Current debate about the L1 tokens valuation frameworks

"If you spend 13 minutes a year using equity frameworks to value commodities, you have wasted 13 minutes" - Joao

I feel compelled to write because I see my peers fighting for purposeless causes. They take the wrong approach and choose the wrong battle.

Before addressing the core purpose of my message, I want to recall famous quotes from my teachers.

I’ve always said if you spend 13 minutes a year on economics, you’ve wasted 10 minutes. - Peter Lynch

We will continue to ignore political and economic forecasts, which are an expensive distraction for many investors and businessmen. - Warren Buffett

These quotes highlight the high cost for equity buyers who spend time on macro. If you focus on macro, you waste time by not researching and improving companies.

Being an expert on stocks means you are likely not an expert on macro.

The current debate is an illusion and serves only as entertainment. Both sides are pro-tech, pro-crypto, and pro-innovation. They both have skin in the game on the bull side of the crypto market. Therefore, this is not a question about technology. It is a question of valuation frameworks. It is an attempt to determine how far we have drifted from intrinsic value and an attempt to select models do work and which do not.

However, they started with the wrong approach.

Stocks ≠ Commodities

They are not comparing potatoes to potatoes. They are comparing potatoes to oranges. These products have different characteristics and serve different purposes. They satisfy different necessities.

This analogy explains why it is wrong to use equity models and stock multiples to value commodities. They have different characteristics, purposes and necessities just like potatoes or oranges.

Models and multiples rely on the characteristics of the underlying asset. In those cases, for equity models the asset is required to be a stock representing a business. Using the same models to value commodities and stocks ends in illusion.

This sounds ridiculous, but it is exactly what is happening.

They compare AMZN to ETH. They use the same multiples to compare ETH and SOL to AMZN over time.

Yet, the Commodity Exchange Act (CEA) of 1936 classifies BTC, SOL, and ETH as commodities. By using equity models to value ETH and SOL, you fight against the CFTC classification we all fight for.

Commodities valuation frameworks usually rely on:

Demand-supply forces

Futures and forward pricing based on contracts for future delivery

Production costs and extraction estimates

(…)

When equity value, we rely on:

Sales, revenue and profit numbers and growth

Margins of the business

Users growth and the value of each user

Multiples of any kind

(…)

These are completely different frameworks currently being used in the debate

Because ETH and SOL are commodities, it should be valued by the supply-demand law, production costs, and contracts for future delivery. This leads us to value these commodities by understanding their demand. Applications must spend tokens for security, and users must spend tokens to transact. We must also understand supply in terms of new tokens created by incentives or staking rewards.

Simultaneously, our layer 1 blockchains are increasing throughput. Tech evolution unlimits gas spending. We must understand that while we increase throughput, the inverse is also true. An eventual blockchain could reduce the total gas able to spent.

Comparing these commodities to Amazon or any other stock is completely irrelevant. I do not see it as productive. It is only useful for entertainment, which explains why I see so much content on this topic.

To see the absurdity, imagine using equity models, like sales, revenue, and profits to value or predict oil prices. The conflict arises because critics claim you need a company to extract the oil. Here is where the fallacy goes bust. Historically, you needed a company to extract the commodity. This is not true currently. We have decentralized organizations and Foundations. Together, they fight to improve commodity supply and demand forces. They backed tokens in proof-of-staking mechanism, and they mine new tokens, as they are commanded by code not manufacturing, land power.

Shift the framework, let’s value businesses - “Invert always invert”

When we say ETH is valued at $400b, we are not looking at the valuation of each foundation as if it were a centralized force. We are consider the total supply time the current market price, to get the market cap of the commodity - that’s it. If you want to use equity models, you must isolate the foundation as if it were a private company. Staking earnings are like revenue for that company. This revenue depends highly on the price of the commodity, but their earnings do not influence the value of the commodity.

This is exactly what happens with oil, gold, or any commodity business. These companies do not hold the same valuation as the commodity market itself.

Consider the oil example. You have an oil market valued at over $6T a year, growing to a predictable $8.7T in 2034. To value this market, you need the correct models to account for almost 50% growth over the next 10 years. You cannot use equity models because they do not work there.

Consider that fees on L1 are distributed to the stakers. Stakers are managed by foundations or private organizations. Take Lido as an example. It shows how different the valuation multiples and the discussion can be if you use the correct models within the correct frameworks to value different type of assets.

Lido secures almost $25b worth of ETH, yet it has a market value of $500m. This means the market value of the organization that “produces” the commodity is valued at 1/50th of the commodity they hold.

Unlike other commodity production companies, crypto proof-of-stake mechanisms force the producers to hold the underlying asset to produce more of it. This is positive correlation force between the commodity price and the producer revenue.

Let us continue with our analogy. Lido is valued at 1/50th of its holdings and trades at approx. 6 P/S (Price-to-Sales), using the TTM Revenue: $88m . We can say that Lido, the producer of the ETH commodity, is not being valued very expensively.

This contradicts the high multiples seen in current discussions.

If we assume the commodity utility will grow over the next 10 years, the P/S should reflect that. The revenue is directly correlated to the price of the commodity. This is exactly the same as oil or gold producers.

We must isolate the stocks from the commodities. We have a 1/50th multiple of the commodity holding relative to the market value of the producer. Ethereum revenue is not concentrated in the Ethereum commodity itself; it goes to the staker. The staker is the producer supporting this market.

The debate often cites a 300 P/S for Ethereum. If we divide this by 50, we arrive at a fair P/S for the producers, the companies. We get a normalized P/S of 6. This is exactly the multiple Lido has. This provides an unprecedented fair comparison.

Ethereum overall producers are being fairly priced at 6 P/S relative to the total commodity value of $400b. Therefore, Ethereum foundations that stake and secure ETH should be valued at 6 P/S. Their sales are represented by the staking revenue they receive.

This is exactly what happens in any other commodity business. Oil and gold producers control the supply of the underlying commodity. If prices are high, they produce more. If prices are low, they stop producing. Production increases supply, which is eventually used or burned to produce new products. Their revenue inflates the commodity supply, so they must manage it appropriately. Similar to the question about staking is revenue or not for stakers - It is revenue.

This is why I believe we are in a cycle of expanding throughput. However, as we go toward the infinite, our producers will eventually produce less revenue, go or not go out of market is a question of demand-supply. Unlike centralized traditional producers, this is decentralized, code-driven manufacturing. The inverse of increased throughput is a decrease in gas spending limits. In the future, we may need to increase gas costs to incentivize stakers who provide network security - this is a possible scenario. Traditional commodity businesses are very similar to current L1 businesses. We just have to use the proper valuation framework in the right corners.

Using equity multiples to value commodities is ridiculous. Similarly, it is ridiculous to value stocks as if they were commodities. I use Lido as a good proxy for the producer because they are, in fact, a producer of ETH. When we price it properly, we see that current valuations are not the 300 P/S everyone is trying to sell. They are actually at 6 P/S and valued properly.

Let me rephrase the quote from my teachers.

If you spend 13 minutes a year using equity frameworks to value commodities, you have wasted 13 minutes. - Joao Baptista

The entire approach is wrong.

On CoinGecko, we can track the market value of ETH and SOL commodities. It is accurate because we track the supply transparently on the blockchain. This gives us $400b and $80b valuations, not the equity value of the businesses.

Let’s assume we know the transparent gold supply. Multiplying supply by price gives the market value, currently $24T.

When we use fees or revenue generated on the Ethereum blockchain, you go one step deeper. You take data from producers and applications, that use the commodity. This data does not belong to the commodity anymore.

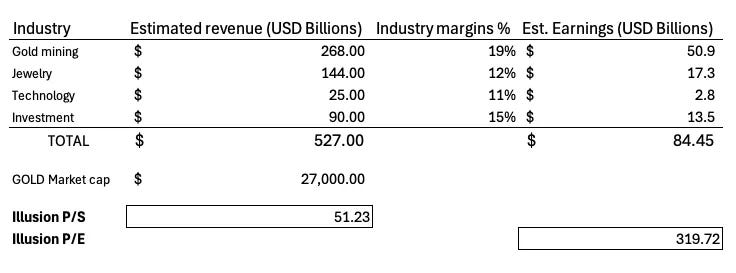

Similarly, to get the fees and value generated on the gold network, you must go deeper into producer revenue and applications, such as jewelry. Using this revenue to apply multiples to the current gold market value is ridiculous, but let us try.

(Note: These estimations are judged by Grok; questioning the numbers is not the purpose.)

Total Gold market cap is $24T.

Total revenue from gold-derived markets is $527b.

Total earnings is $84b .

We could argue that gold has a P/S above 50 and a P/E above 300. It is hugely overvalue commodity.

Looking at this data, gold, oil, and any other commodity appear overvalued and expensive. This is because we use equity values, aggregate everything, and distribute that to the commodity value. We miss the critical component. The value of the commodity is not the value of the businesses that use the commodity to live.

ETH and SOL are being priced exactly like other commodities when we take the right approach. A commodity is a function of total supply outstanding times the current price. This is simply a function of demand and production.

I never thought I would need to write this paper. Apparently, my economist eyes see things clearer than the top leaders I followed my entire career. Many of them are the reason I spent the last five years in crypto.

Thanks,

Joao