Hyperliquid.

40-Pages report pricing HYPE progress.

The View in One Page

Hyperliquid no longer trades as a crypto-only story. In just 9 months, HIP-3 - builder-deployed perpetuals on stocks, indices, ETFs, commodities, FX and pre-IPO companies - has come to carry a third of all volume on hyperliquid, and it is now the platform’s biggest volume driver. That changes what we are valuing: HYPE trades the all-exchange narrative now, not only a decentralized crypto perp venue.

Strip HIP-3 out and the stakes get obvious. Volumes would fall by more than 50%, the venue would basically be BTC-trading only, and HYPE - $70 in early July 2026 - would sit at $10 to $20.

But the pillar has a crack in it. HIP-3 is, in practice, one company: tradeXYZ runs basically 100% of the market, a clear monopoly whose founder stays anonymous. So the regulatory threat that matters is second-order - enforcement against the deployer, not against the platform - and if TradeXYZ goes, Hyperliquid’s biggest market goes with it. No risk to Hyperliquid is more structural than this one.

The scenario work prices it. Across the Down, Stable, Up and UpUp grid, expected value comes out at $17.4b MCap against a $15.3b market cap - the market has, in a way, already paid for the base case, and there is not much upside left at the current price. Near a $10b valuation, the long could get super interesting.

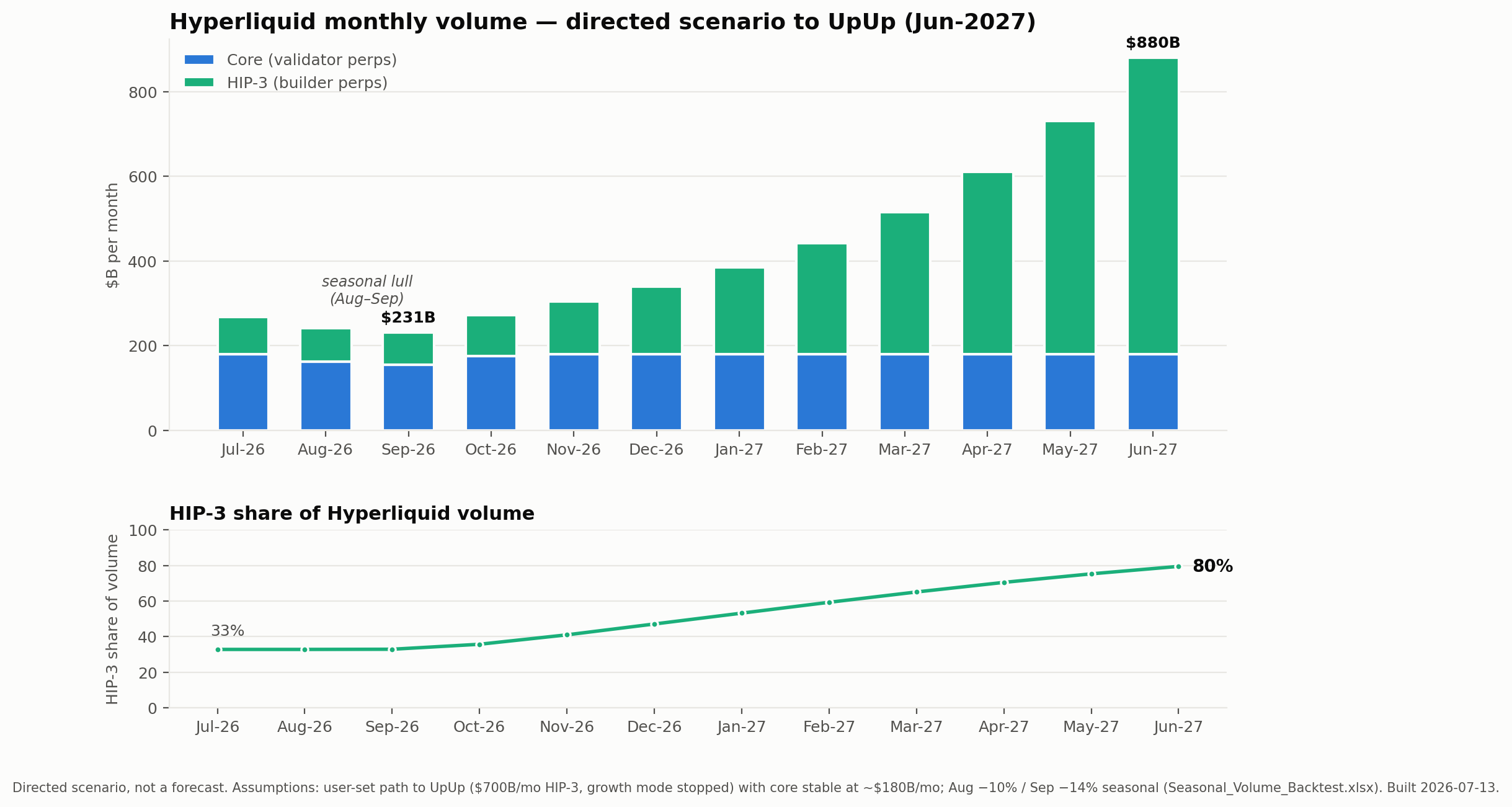

The re-rating case is conditional, not priced. Take “growth mode” off 50% of the market with TradeXYZ still the monopoly deployer, and direct HYPE-holder economics clear $100m a month - multiple math that points to $30b, +100% from here. And timing beats pricing: this is HIP-3’s first summer, and I could see August and September being its worst months for volume; under these conditions we should buy (no matter what) in mid to late September.

(Gmail: joao@atiscapital.net ; Tg: jbbaptista)

Phase One: A Crypto Exchange on the Crypto Cycle

Hyperliquid has been alive with trading data since 2024. Hyperliquid was a phenomenon early on: in just a few months it reached over $100b in monthly perp volume. The clear inflection point came in 2025 - entering 2025 with over $100b in monthly perp volume, then reaching peak volume of almost $400b in August 2025, 9 months later, a net win of +166% from the beginning of 2025 to the August peak.

I divide the Hyperliquid story into two phases, and it is with this two-phase approach that we are going to analyze Hyperliquid: the first phase, before 2025; and after 2025. Being explicit: pre-HIP-3 and post-HIP-3. HIP-3 changed Hyperliquid’s entire position, fundamentally changing where they sit on the everything-exchange route. It changed the ability to monetize, and to grow in every possible world environment. In the pre-HIP-3 era, Hyperliquid was dominated by crypto token volume - it was naturally built for that - particularly with the growth of ETH trading, which peaked at +58% more volume compared to BTC. ETH reached approximately 45% of the total market share of all Hyperliquid perp volume and peaked at almost $180b of perp volume in the single month of August.

In this period, ETH performed well: 3-month performance over +76% (June to end of August), and +141% in 6-month performance (the 6 months to end-August). The volumes were justified by this aggressive token performance. We can’t claim causation, but we can see a high correlation between volumes and the price increase. ETH traded from a low of $1,484 to a high of $4,837, while monthly volumes grew from $40 to $176b over the same period.

We see a high correlation between price and volumes - they are widely correlated. Reflexivity: when prices come down, volumes reflect the same trend. After the August peak, ETH went down, and we expected Hyperliquid perp volumes to go down with it, in correlation - which proved true.

Since August and particularly until 2026, all volumes came from crypto tokens. ETH dominated the entire market, owning at peak a 45% market share and crossing BTC volumes in July.

But it held for only a short period of time. In August, and particularly on October 10, the market rotated bearish, suppressing prices and volumes across the majority of crypto-related tokens. The ETH price is down more than 60% since the August peak, reflecting unsurprising pressure on Hyperliquid’s perp structure. We are going to talk about this more deeply further ahead.

A quick note: with all the rest of the tokens suppressing volumes, BTC volumes remain stable. By comparison, ETH previously traded $176b in a single month and is now trading only $30b in June - down 83% from the August volumes.

But in 2026, something changed fundamentally in the Hyperliquid venue. We see a big red wave capturing volumes on Hyperliquid. Underlying this new era is the rising expression of an entirely new market: the HIP-3 market, allowed since late 2025 but best represented by the growth of tradeXYZ. HIP-3 is now the biggest volume driver for Hyperliquid, fundamentally changing how we value Hyperliquid.

The mix tells the story. In the first era of Hyperliquid, the sustainability and health of the business were directly affected by crypto market performance - 100% of volumes came from crypto token trading. Now, having multi-funnel trading instruments is a much healthier and more sustainable position, less impacted by the crypto industry. The market share of crypto volumes is dropping from 100% to 68%. This trend tends to keep moving down; I expect crypto trading to represent as low as 25% of the overall trading inside Hyperliquid. We can’t deny that crypto trading still has a huge impact on Hyperliquid economics, but the trend is moving toward less and less relevancy, after the launch of HIP-3 and eventually the growth of HIP-4.

Without HIP-3, Hyperliquid Would Be a BTC-Only Venue

Let’s just imagine what the current numbers would be without HIP-3. Volumes would be at $180b, dominated 50% by BTC trading (June with $90b of BTC volume) - volumes dominated by BTC and the rest, with ETH at $30b of monthly volume.

Volumes would be down more than 50%, with a BTC concentration at 50%. Hyperliquid would be a super-concentrated trading venue - basically a BTC-trading venue only. It would carry a tremendous amount of risk attached to the bitcoin price, and not much forward upside without diversification of its economics. $180b of monthly volume against the real number of $266b (June 2026) represents a gap of less than $80b of volume and a decrease of over 30% compared with the real, with-HIP-3 economic data.

Consider where HYPE is currently trading: $69b FDV (July 3, 2026), with a monthly trading volume of $266b - annualized, just for expression, $3.2T - printing a price to annualized volume of $0.02. Revenue sits at $60m for the month of June - annualizing, just for expression, $720m of annualized revenue - for a PS of 95 considering FDV, a 21.5 PS considering the $15.5b market cap, and a 54 PS considering the $39b of outstanding token value.

The point here is that high multiples are being assigned to the instrument that best represents Hyperliquid - HYPE - based on the promise that new revenue funnels can be generated, and that Hyperliquid keeps buying back the HYPE token with those revenues. To increase the burning velocity, Hyperliquid must generate higher revenue - meaning more volume funnels and higher data numbers.

At the end of the day, Hyperliquid economics comes down to volume numbers and the ability to monetize those volumes. With 30% less volume without HIP-3, the real volume number is 30% lower - and on top of that, the expected future volume number would be much lower by reflection. The market would price HYPE at a much lower multiple - probably half, or even less - as a consequence of lower expected volumes, which would also show up in lower revenues, pressuring the HYPE token even more. Without HIP-3, and taking a huge assumption, we could see a PS on market cap of 5 to 10 - a 50 to 75% decrease - and revenue 10 to 25% lower than we have now. Meaning we would see HYPE prices at $10 to $20, and not at $70 as we are seeing in early July 2026. Even worse if you run this calculation actualizing the future cashflow value of Hyperliquid with or without HIP-3, lowering future multiples.

But HIP-3 exists, and it gives the market confidence that Jeff, the prodigy, has the ability to generate new trading venues, new volume sources - the ability to drive different waves as the market grows, creating an all-weather platform in which all civilians can participate, from traders to enterprises to issuers. Today Hyperliquid has two structural waves flowing: crypto trading, and HIP-3 trading creating powerful economics going forward. The third wave will be HIP-4 - already launched in June 2026 - predicting a new wave flowing in parallel to HIP-3.

The Hyperliquid management team’s ability to pursue new markets with perfect timing - creating the ability to generate new volume funnels - is what gives HYPE its high multiples and its deserved market value. Where in the first phase volumes came from crypto trading, the second phase is now being pushed by tradFi trading - commodities, stocks and even currencies. It underwrites the management team’s ability to pursue new ways of monetization, with high efficiency. HIP-3 and HIP-4 are both already launched, pursuing a high expected value.

HIP-3 produces positive fundamentals for the value of Hyperliquid: it lowers the correlation and concentration to the crypto industry; it creates a multi-funnel revenue stream; it creates an all-weather revenue situation; and it smooths the volatility of the revenue. Hyperliquid volumes are much stronger with HIP-3, and they will be even stronger when HIP-4 reaches its velocity. HYPE is now trading the all-exchange narrative, not only as a decentralized crypto perp venue.

HIP-3 Volumes Are Ripping

Even with the innovations, August volumes have not been reached yet. The forward probability of reaching those numbers is high, but in reality we are already 6 months past the peak and have not yet reached new highs in terms of volumes, in a situation of hot stock market. I see a high probability of reaching new highs by year-end, just with the consolidation of crypto markets and the growth of HIP-3, but still a future reality, not a present reality.

HIP-3 volumes are ripping - growing +37% last month, reaching above $85b in monthly volume, and probably achieving the $100b monthly volume benchmark in a few months. HIP-3 is an impressive product: in just 6 months, HIP-3 grew from less than $10b of volume a month to over $80b - growing 8x in 6 months.

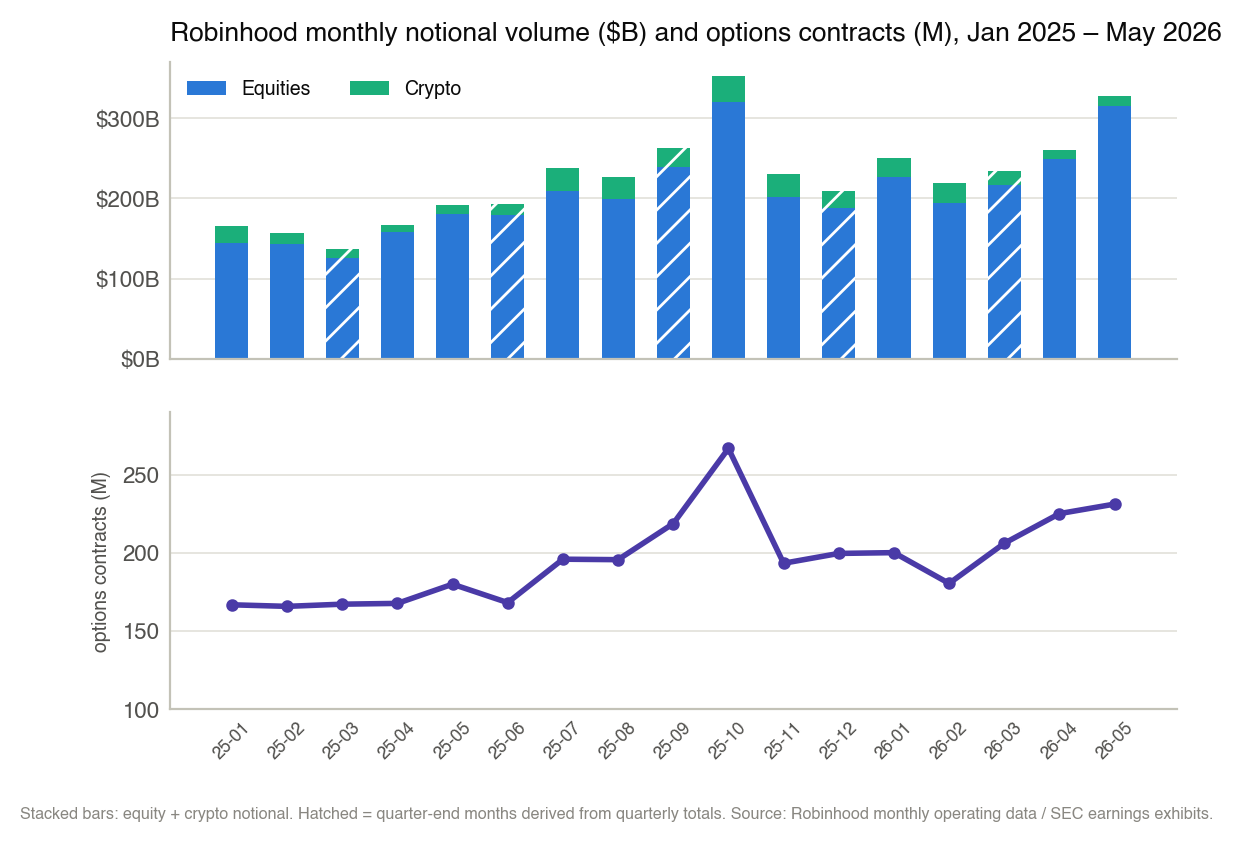

The TAM to grow this market is not the real problem. Robinhood traded over $300b of equity notional in spot volumes, and perp volumes usually run 10x higher than spot volumes, judging by Binance and Bybit relative volumes. Robinhood, at above $300b of notional equity monthly volume, is trading 25x more than crypto notional. It signals extreme upside. For comparison, HIP-3 volumes remain 0.47x the crypto trading volume; if this reverts (as the current trend is supporting), converging toward the Robinhood data, we can see trillions in monthly volume in the near future - just by pushing HIP-3 volume above crypto volume.

The volume profile has already changed a lot, and the trend is strong for a continuation. 1/3 of the volumes are now dominated by BTC trading, 1/3 of the volume comes from HIP-3, and the other 1/3 goes to other crypto tokens. The volume dominance now sits in BTC trading and the HIP-3 markets - bitcoin still being the single most tradable asset on Hyperliquid.

What HIP-3 Actually Is

HIP-3 represents a third of the entire exchange in just 9 months. To understand the new Hyperliquid era, we must have a sense of what HIP is.

HIP stands for Hyperliquid improvement proposals. HIP-1 is the native token standard - the launch of native tokens with onchain spot orderbooks. HIP-2 was the hyperliquidity proposal - the operator-less market-making strategy built into the chain itself, for all HIP-1 tokens: the launch of HLP. HIP-3 is builder-deployed perpetuals: it unlocks the ability for anyone who stakes 500k HYPE to deploy and operate their own perp exchange on Hyperliquid’s infrastructure - including stocks, indices, ETFs, commodities, FX and pre-IPO companies. HIP-4 is the outcome markets: it allows fully collateralized contracts that settle within a bounded range, the primitive for prediction markets and binary options. These are, so far, the 4 proposals that unlock what Hyperliquid is today.

HIP-3 is not directly attached to stocks and commodities, and it was not directly forced by the Hyperliquid core team. Hyperliquid created the rails so that anyone who stakes 500k HYPE could deploy their own perpetual-futures exchange running on Hyperliquid orderbooks, matching engine, margin system and liquidation infrastructure. The deployer chooses what to list, defines the contract, and operates the oracle pricing - and deployers set out to list TradFi assets because that market is a lot bigger, and crypto was already dominated by Hyperliquid. Hyperliquid provides the exchange machinery - the infrastructure - and the deployer provides the markets. It is a super-connected ecosystem of Hyperliquid and deployers that independently manage their own markets, benefiting from Hyperliquid rails and assuring that their clients will be able to trade with efficiency, relying on Hyperliquid infrastructure to do so. With this proposal, Hyperliquid moves away from being the originator of new markets, creating the rails for independent deployers to own their own markets.

Discipline is managed by the Hyperliquid validators, with voting power to slash a deployer’s stake if there is degradation, downtime, or invalid state transitions; deployers can be slashed by 20%, 50% or even 100%. Slashed HYPE is burned, not paid to victims. So far, no slash has occurred, but it is a way to manage deployer efficiency and build trust between the parties.

HIP-3 had a bunch of partners, and Hyperliquid wins by having multiple deployers - each one stakes 500k HYPE. But so far, only one deployer really grew and was able to drive under HIP-3: TradeXYZ.

TradeXYZ Is HIP-3

TradeXYZ today controls basically 100% of the entire HIP-3 market share alone. It is a clear monopoly in HIP-3 contracts, launching commodities, index, equities, ETFs, and pre-IPO instruments. TradeXYZ owns almost a third of the entire Hyperliquid volume, and it is now the most relevant partner for Hyperliquid core.

TradeXYZ’s execution has been perfect, absorbing the entire HIP-3 market. To analyze HIP-3 is to see a reflection of TradeXYZ. TradeXYZ proved the ability to grow - growing by single-instrument volume and by adding more instruments live. It grew the monthly volume first, particularly during the Iran war, allowing traders to trade OIL-perp instruments 24/7, with liquidity - publicly used on the New York Stock Exchange floor. TradeXYZ rapidly won the commodities category, then expanded into all the other categories, now dominated by equities and index trading volumes, reaching above $80b in monthly volume last month, June 2026. The origination of volumes changed with time, but the ability to dominate every market is, for lack of better words: euphoric.

In 8 months, TradeXYZ grew from $0 to $80b in trading volume, with 95 different instruments. It launched 14 new instruments last month, June 2026. At this level of scale, by the end of the year they will double the number of instruments tradable inside their own HIP-3 platform.

Execution and growth have been flawless: the ability to scale monthly volumes and push new assets live, growing in multiple directions - a higher quantity of instruments live, and higher volumes per instrument. By July 3, the single asset with the highest notional is CL, the WTI crude OIL instrument, with a notional of $31b - a total of 19% of all TradeXYZ (HIP-3) notional. Other commodities like SILVER, and then the XYZ100 index, hold second and third place, with $26.8b and $26.7b respectively.

TradeXYZ is in complete rocket mode. It is trading $2.4b of notional volume on peak days, and its growth is sustainable WoW, MoM. With the incremental addition of new instruments - dominating all markets and unlocking new assets for Hyperliquid - now that the machine is built, the scaling laws just allow more and more instruments to be traded on Hyperliquid, acquiring every possible market to unlock the everything-exchange promise.

And the mode is exponential - growing more categories and the overall cumulative volume.

A market whose growth was once dominated by commodity trading is now growing through new hyper-growth categories - equities, index, pre-IPO - trading more notional volume than commodities. Equities are trading $2.7b in weekly notional volume, and commodities are at $0.9b in weekly notional volume. Mark that even within the HIP-3 segment, the rotation across multiple instruments and multiple categories holds true. TradeXYZ’s ability to pursue more instruments generates sustainability in their volumes, which reflects into Hyperliquid’s volumes as well.

Risk One: Nobody Knows Who Runs TradeXYZ

TradeXYZ’s execution is solid and their economic data is solid - but what is tradeXYZ, and who are they? What do we know about the management? Can we underwrite their ability to continue at this growth level? By underwriting tradeXYZ we are underwriting HIP-3 sustainability, which reflects across all of Hyperliquid’s health. The deployer controls the oracle for each instrument - one of the most important and vulnerable bricks. Let’s explore.

TradeXYZ is a perp DEX that deploys on Hyperliquid core. The founder remains anonymous: we don’t know who he is or where he is. But the origin is tied directly to Jeff (Hyperliquid’s founder) - the tradeXYZ founder’s decision to build tradeXYZ is attributed to meeting Yan and to conviction in Hyperliquid. The founder is anonymous, but at least he has personal connections with Jeff. Even knowing that Hyperliquid is, in a way, directly tied to tradeXYZ - and surely trusts the founder - the public markets have no information on who he is. $80b of monthly notional volume is trusting a company whose founder prefers to stay anonymous (we live in 2026, in AI era). This is only possible because they are deploying on Hyperliquid, their execution is impressive, and they partner with S&P Dow Jones Indices for their S&P 500 perpetual contract.

Not a single source discloses the founder’s real identity, nor any city, country, or jurisdiction of operation. There is one named executive, disclosed because of S&P Dow Jones Indices licensing the S&P 500 to the venue: Collins Belton is quoted and identified as COO and general counsel of TradeXYZ. But other than Collins Belton, we know nothing about the management team behind tradeXYZ. This is the single most important structural risk for Hyperliquid: this one deployer owns “all” of the HIP-3 market - owning 1/3 of the entire Hyperliquid total volume - and it is growing at an extreme level of scale, eating the entire Hyperliquid volume and eating market share from all competitors.

Risk Two: The Oracle and the Corporate-Actions Gap

The HIP-3 operating stack is composed of three layers: 1. HyperCore, managed by Hyperliquid, runs matching, order types, funding settlement, liquidations and auto-deleveraging - onchain execution, with decisions by the validators; 2. The XYZ protocol defines market listings, oracle sources, leverage limits, margin modes, and open-interest caps - decisions by the deployer; 3. The TradeXYZ operator runs the off-chain relayer fleet that prices every market and pushes updates onchain.

The TradeXYZ management team controls two layers, owning the relayer work: computing oracle, mark and external prices for each asset and broadcasting updates to HyperCore every 3 seconds. The operational risk is here - there are many areas that could fail. They partnered with Pyth and Blue Ocean ATS to provide a public pricing-reference source for the majority of instruments and for the US overnight equity session, respectively. There are many mechanics that allow tradeXYZ to trade, 24/7, instruments that are open only a few hours per workday, shifting oracles from external to internal pricing driven by their own orderbooks. Anti-manipulation systems and trader-protection systems must also be deployed, to guarantee there is no possible vector of attack.

But the risk is there: oracle failures, and single-stock corporate actions - splits, spin-offs, delistings, and so on - for which there is no adjustment policy published in any document. Operationally, there is a gap to note. The earlier SPCX precedent determined contracts on a price-based, no-rebase settlement: the default across all XYZ markets is to track the quoted per-share price through the event rather than adjust positions - inferred from the SPCX event, not from documented policy. That brings real operational risk to trading stocks through probable single-stock corporate actions. In a stock split, an apparent conflict between prices and the split could happen, and the resolution is unsettled.

TradeXYZ accumulates two sets of risks: 1. Founding/Management structure; 2. Operational. But there’s more.

Risk Three: Regulation, on the Binance Timeline

Both Hyperliquid and TradeXYZ sit in a very good spot in terms of economics, but in a devil of a position in terms of regulation. Neither is licensed or clearly legal in any country of the world - so countries like the US and Canada are banned, and the others sit in a gray-area position.

The numbers are becoming impossible to ignore. Hyperliquid and their deployers are rotating into a more compliant and regulated market (from crypto to tradFi assets), where the world enforces more licenses and higher controls. The two are interconnected in terms of regulation, but they have different regulatory structures.

Hyperliquid is decentralized at its core. It runs on independent validators - even if they are concentrated, they run a decentralized organization - and Hyperliquid creates the rails for new independent deployers to provide access to new instruments, creating perps for all assets. They don’t sit to control, operate, or own the equity, commodity, index, or any instrument for their clients; by providing access to these instruments, they create the rails for others to provide that service. TradeXYZ is the deployer allowing that access to perpetual contracts on all those types of instruments - and in a well-regulated market, with rules that block any unlicensed deployer from creating derivatives contracts on any instrument, tradeXYZ sits in a position attackable by the regulators. Making $100b plus in monthly volume on tradFi perp contracts without any license, or a public founder - it’s a three-legged chair.

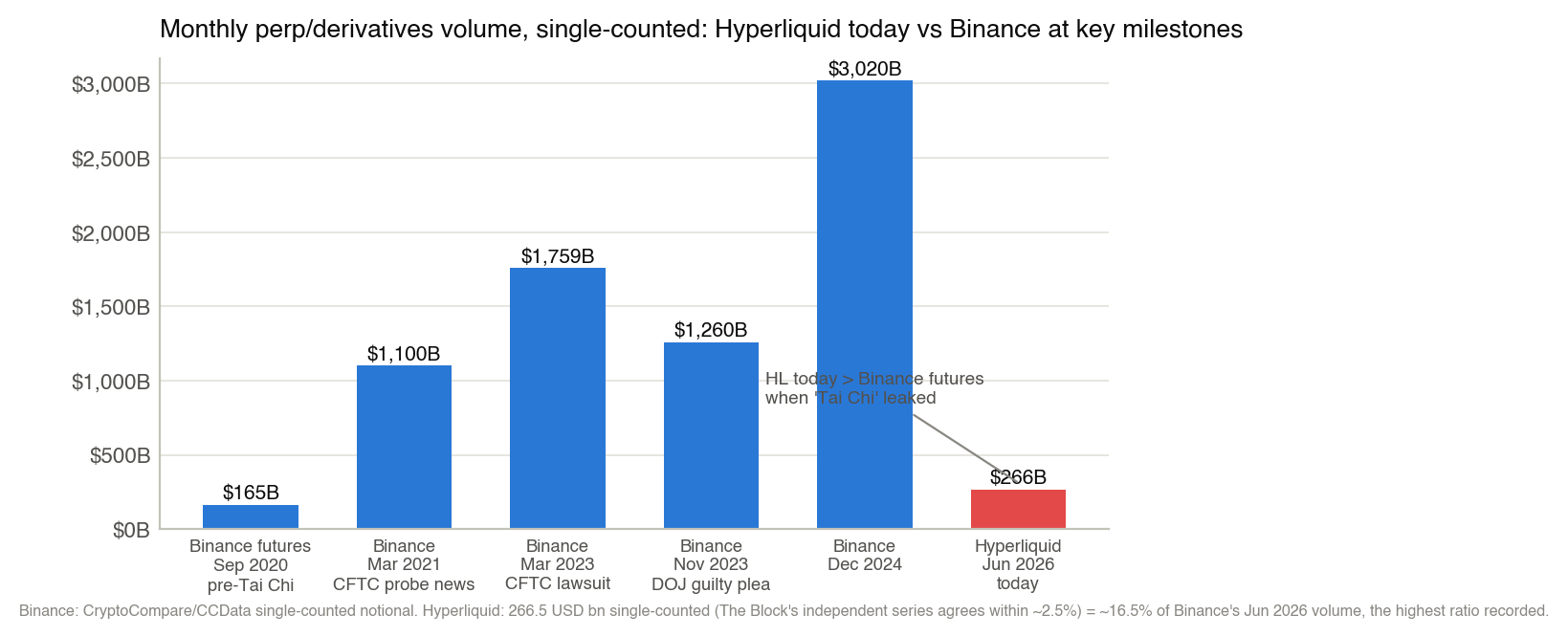

Binance and Hyperliquid are completely different in many aspects: Hyperliquid is a wallet-based, non-custodial, decentralized perpetual exchange; Binance was an email-account-based custodial exchange. But in many ways they were (back in 2017 to 2022) very similar - serving derivatives contracts without licenses, KYC, or an AML program, and serving worldwide customers, including banned and probably sanctioned nations. On Hyperliquid, the incentive for sanctioned nations is very limited: the major product is synthetic, and either way it has been trackable by Bloomberg and ZachXBT. For Binance, that was a major IEEPA/OFAC issue.

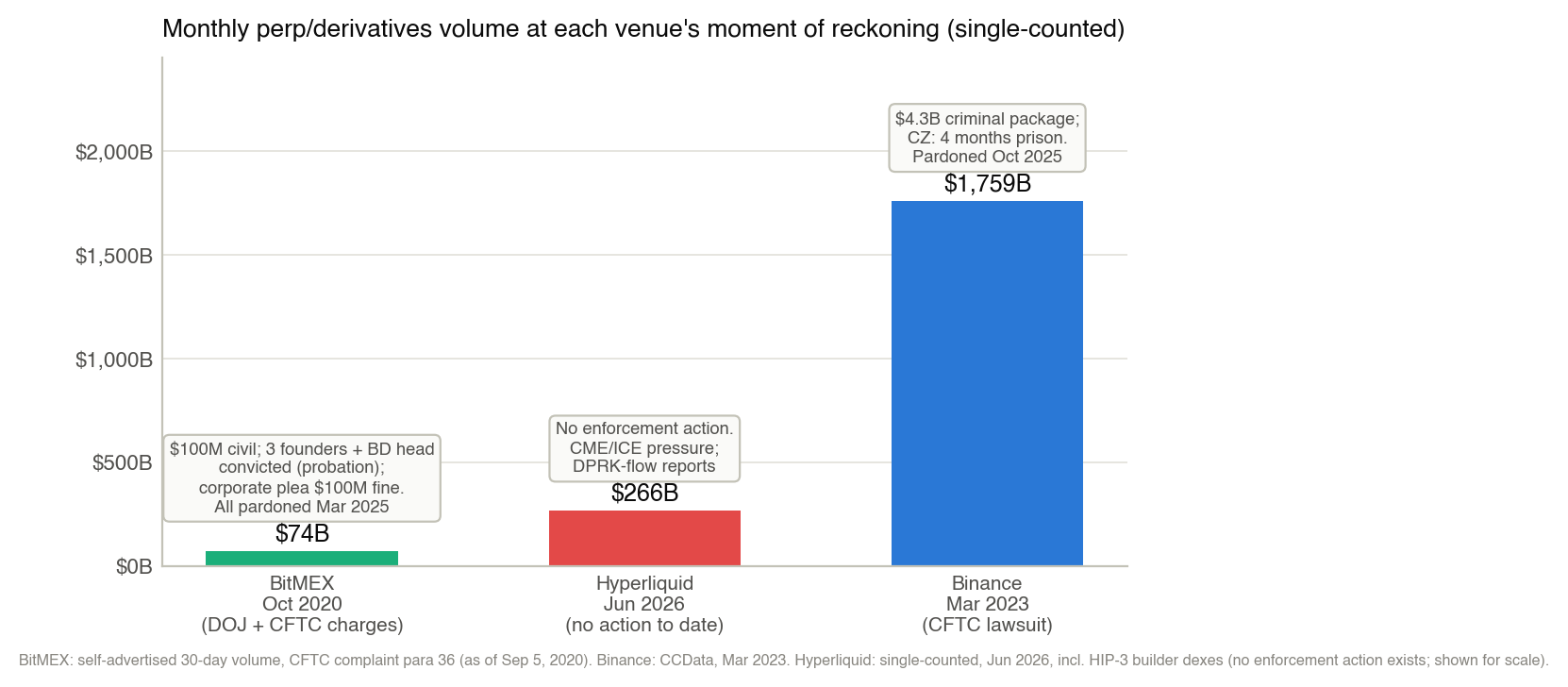

Binance had three major phases. Phase 1: the growth phase, from 2017 to 2019. Phase 2: scale explodes, and the warnings. Phase 3: enforcement. In growth mode, Binance did everything possible to acquire and grow its user numbers and volume data. The first regulator to act was Japan’s FSA in March 2018, and in 2019 the administration mentioned that US users dominated 20 to 30% of their traffic. In the leaked “Tai Chi” document, Binance was doing $165-$450b a month in futures volume. That eventually led to the CFTC investigation in March 2021 to identify whether US residents were trading on binance(.)com - concluded in May 2021 - and a DOJ and IRS criminal-side probe; US VIPs alone were 63% of Binance(.)com VIP volume. The UK FCA banned Binance, and Japan’s FSA issued its second warning. Binance kept growing both its market share and its total monthly volume. Eventually, in March and June 2023, Binance and its founder were penalized - for serving US customers with no KYC or AML policies, for operating an unregistered futures commission merchant, for serving sanctioned countries, and with 13 more charges directly on Zhao, Binance’s founder.

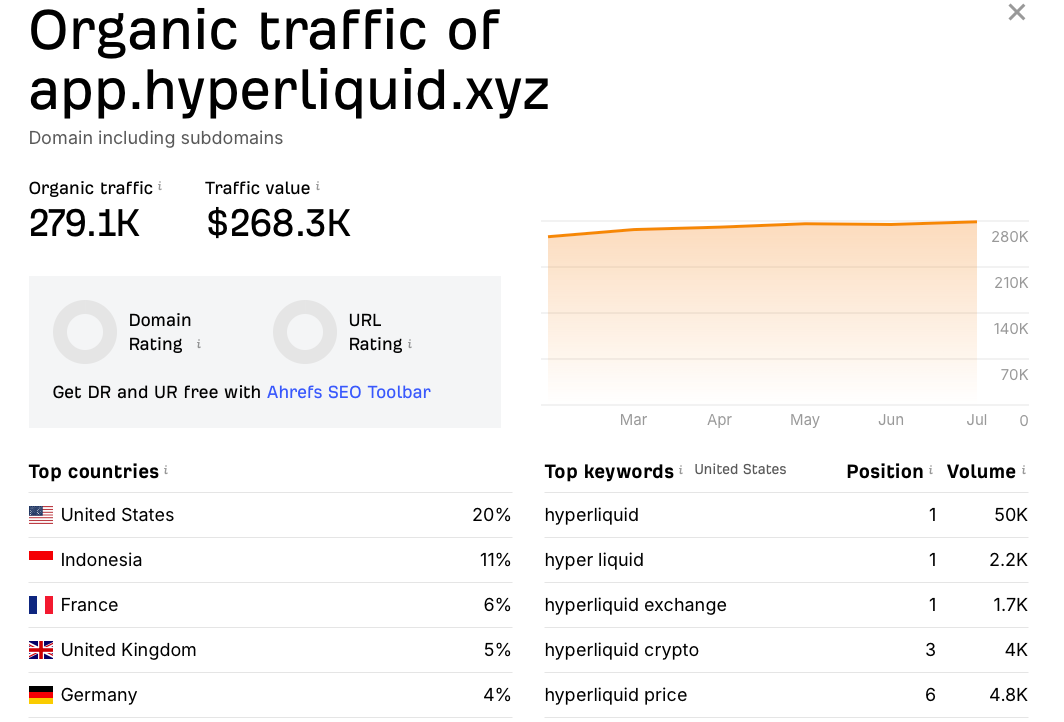

Binance and Bitmex were clear examples of the enforcement - showing that regulators will force any rules onto unregistered commission merchants serving banned US clients. Even though Hyperliquid apparently “enforced” a ban on US customers, simply by tracking the traffic of their webapp URL we can identify the US as the top country in search results, owning 20% of the total traffic value. Many use VPNs, APIs and other offshore ways to get access to Hyperliquid. But the high number of searches for Hyperliquid’s direct webapp URL is publicly visible.

Hyperliquid today is trading $266b in monthly perp volume (without double counting), with $2.9T for the 2025 full year alone. Moving from crypto-only to an all-asset exchange increases the risk of regulatory pressure. So far, no regulator has acted against Hyperliquid, and the parties behind the administration are super important for measuring these risks - the Trump administration is pro-crypto and pro-tech, has taken no enforcement actions, and provided pardons to both the Binance founder and the Bitmex founder. This provides relief on regulatory pressure, but it still doesn’t solve it. They will open the gates or close them by enforcing any sort of rules and steps. There are no direct regulator attacks, but CME Group and ICE formally urged US regulators to scrutinize Hyperliquid over manipulation risks - the first warning signs from competitors that are being threatened by the growth of Hyperliquid. That happened in May 2026.

The risk grows as the monthly perp volume grows, and as they scale into serving tradFi instruments. We are at higher levels than the pre-Tai Chi leak, but a lot lower than the levels of the March 2021 Binance action.

The risks run along three main vectors: CFTC, BSA, and IEEPA/OFAC.

The CFTC vector covers the offering of leveraged derivatives to US persons without FCM/DCM/SEF registration and with no CIP/KYC. Hyperliquid’s HIP-3 equity and pre-IPO perps (SPCX as an example) sharpen the exposure: they resemble security-based swaps, where retail offering restrictions are stricter still and the SEC/CFTC boundaries are unresolved.

BSA - the Bank Secrecy Act - covers DOJ criminal charges for operating as an unregistered money-transmitting/financial institution serving US persons without an AML program. Hyperliquid’s legitimacy here rests on its non-custodial architecture: whether a validator-governed L1 with a bridge contract “transmits money” is untested. Clear DeFi rules must be published; the Clarity Act will provide guides on this.

The IEEPA/OFAC sanctions vector covers the openness to sanctioned-jurisdiction trades. Hyperliquid’s open access cannot exclude sanctioned users, and DPRK-linked trading (Lazarus-attributed wallets) is already publicly documented. OFAC has sanctioned smart-contract addresses in the past - Tornado Cash in 2022. Vulnerable.

Even with all these risks, Hyperliquid sits above all this pressure, and the climate under the Trump administration and the worldwide posture on crypto technology have changed 180 degrees. Meaning: the support that worldwide politicians are giving to crypto markets is much more aligned than it was 2/3 years ago.

TradeXYZ, the biggest deployer on HIP-3, adds a second, sharper legal layer on top, because of what it trades. Hyperliquid is a core contributor; it doesn’t operate. TradeXYZ is an operator - and an operator that touches securities and commodities. Perps referencing single stocks or narrow indices sit at the security-based-swap boundary, where US law requires SEC-registered venues and effectively bars retail participation. The May 2026 CME/ICE letters urging CFTC scrutiny of Hyperliquid specifically cited the synthetic stocks and oil markets - basically tradeXYZ products. This pushes tradeXYZ into a corner: even if Hyperliquid core is not being charged with any illegal action, tradeXYZ at scale could eventually be charged for operating these unregulated synthetic instruments, offered without KYC or AML to a worldwide user base. And this is the major regulatory risk hanging over Hyperliquid - the threat from regulation lands not on the Hyperliquid platform but as a second-order effect, on tradeXYZ being charged. And they alone control the entire HIP-3 market. If TradeXYZ is forced out of the market, Hyperliquid loses its biggest market in one stroke.

The Economics: What HIP-3 Pays HYPE Holders

HIP-3 is THE pillar of Hyperliquid’s growth. It is the reason HYPE is valued as it is. And it is the reason investors stack capital by owning the instruments that best represent the growth of Hyperliquid - HYPE.

HIP-3 is super relevant in the growth numbers, measured by huge market penetration - owning 1/3 of the total perp volume - with a clear uptrend. It is almost certain that HIP-3 volumes will flip crypto volumes; it is not far from achieving it.

The risk in regulation is real. The further question is to understand whether this HIP-3 growth represents a direct economic value transfer to Hyperliquid. How are synergies created between Hyperliquid and their deployers? What is the economic sharing program that allows both companies to grow together in complete synergy, with positive EV for both, sustainable long-term?

The deployer sits in a position to keep 50% of trading fees as a base: all trading fees generated are divided 50/50 between deployers and Hyperliquid, as a fair distribution. On top of that, there is a “fee scale” mechanism allowing the deployer to add a further 0-300% of fee growth, with one particularity: above 100%, the protocol’s own fee rises to match, ending up splitting all trading fees generated 50/50. This economic design allows the synergies to happen at all times, in all possible situations. The deployers get to decide the fee number, and deployers can compete over fees.

Hyperliquid wants to push HIP-3, as it is a much bigger market than the crypto market alone. To do so, they launched “Growth mode” in November 2025, cutting protocol fees, rebates and volume contributions by 90% to help new markets bootstrap liquidity.

“Growth mode” has worked. There is a clear trend through year-end for HIP-3 volumes to flip the non-HIP-3 volumes, as more and more instruments trade on HIP-3 through TradeXYZ and new participants aim to capture a portion of tradeXYZ’s HIP-3 market share by competing; more volume, in the aggregate, will compound. The non-HIP-3 and HIP-3 volumes are converging.

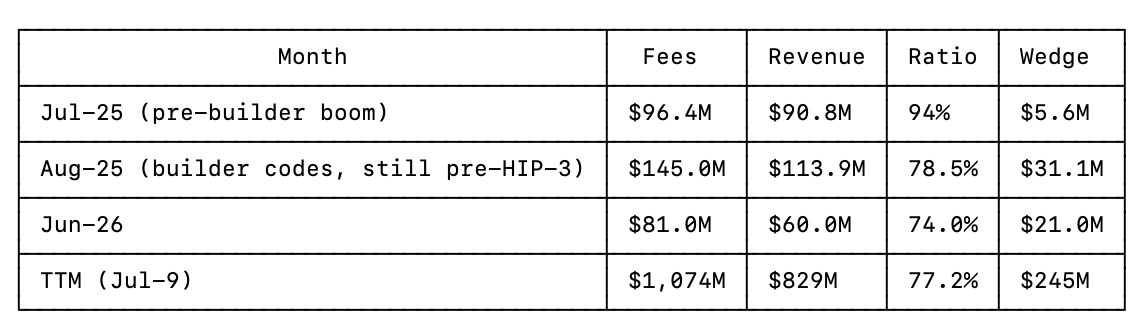

But in terms of fees generated through each HIP, they are far from matched. The core reason is the “growth mode” program, developed to bootstrap the initial growth of HIP-3. HIP-3, with $85b of perp volume in June, printed only $8.7m in monthly fees - an economic value of $0.0001 per volume traded.

Most of the fees are, to this day, still generated on the non-HIP-3 instruments - meaning the crypto-trading venues. Non-HIP-3 alone printed $58m in June, reaching new YTD highs in economic value created and representing almost 90% of total fees generated. Together they reached $67m in June monthly fees, growing +40% YTD in fees generated.

Not all fees are directly revenue, but a big portion is. For non-HIP-3 markets, each fee generated is distributed to builder-code apps, referrers, and HLP’s 1% distribution. In pre-HIP-3-launch data, approximately 78% of the value of fees shows up as revenue: in August 2025, pre-HIP-3 launch, Hyperliquid generated $145m in fees and $113m of revenue - a $31m wedge, distributed to referrers and builder codes.

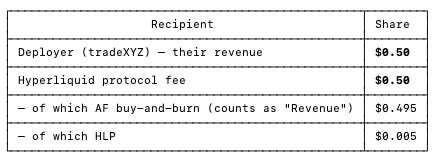

For HIP-3 markets, all fees carry the conditions previously explained. TradeXYZ divides the fees 50/50 with the Hyperliquid protocol. 1% of the total fees still goes to HLP, and the rest goes to the AF - the Assistance Fund - to buy back the HYPE token. In real numbers, 49.5% of total TradeXYZ HIP-3 fees represent direct revenue to HYPE holders.

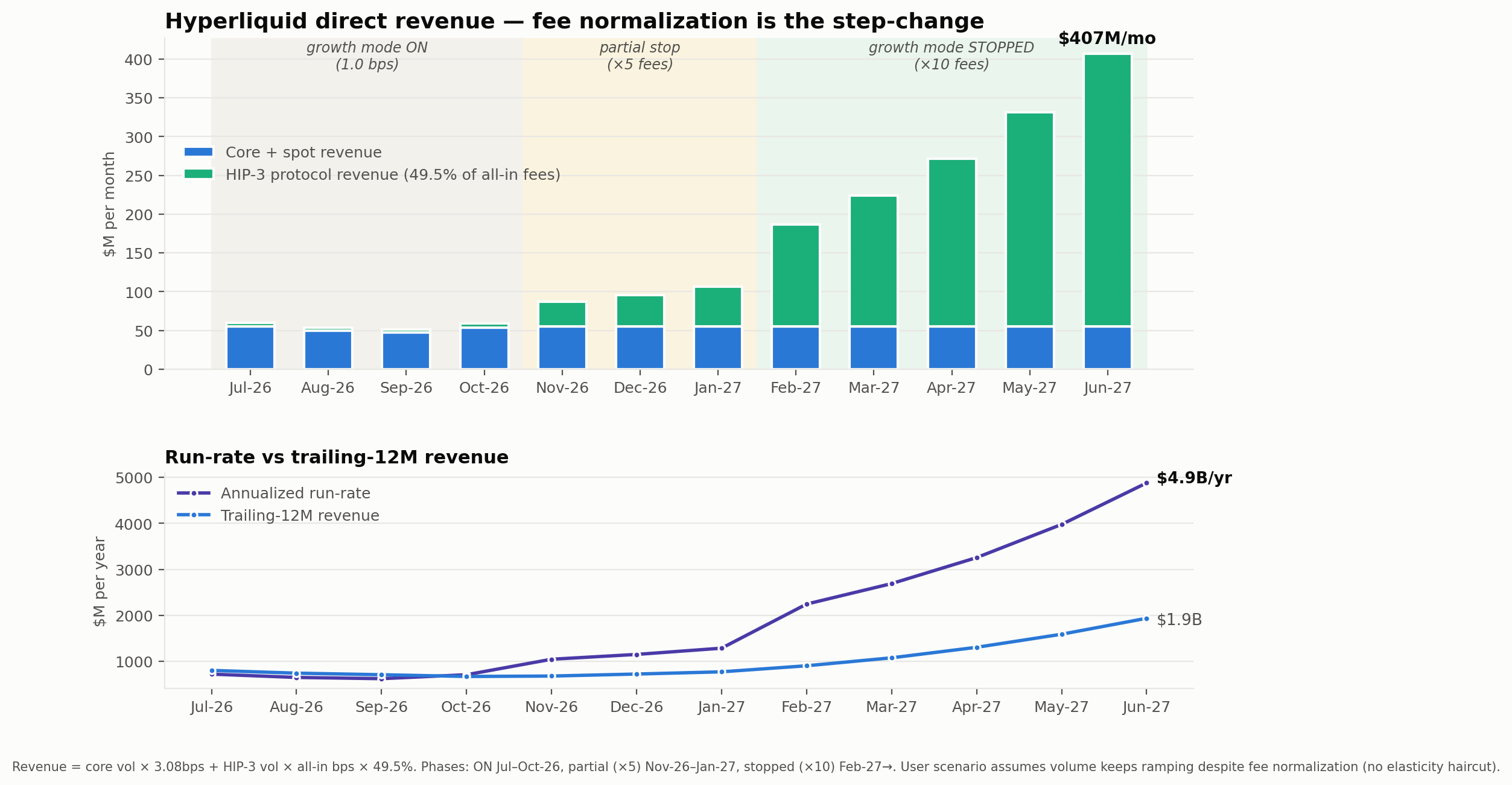

TradeXYZ doubled the protocol base (tiers can be increased by staking-HYPE, that discount base fees) to a 0.048%/0.09% base. In growth mode, for the majority of instruments, this base fee is pushed down -90%. Even with these massive discounts, Hyperliquid overall printed $8.7m in fees last month, with +502% YTD growth, on $85b in perp volumes. It is set to more than double by the end of the year, growing on average +15% MoM and reaching $20m in monthly fees for HIP-3 - with huge assumptions: that TradeXYZ keeps dominating the market, and without the catalyst of more and more tokens being pushed out of “Growth mode”. So far, we have only 4 instruments not in “growth mode” - GOLD, MSTR, PURRDAT and STRC - tokenized equities directly tied to crypto and gold.

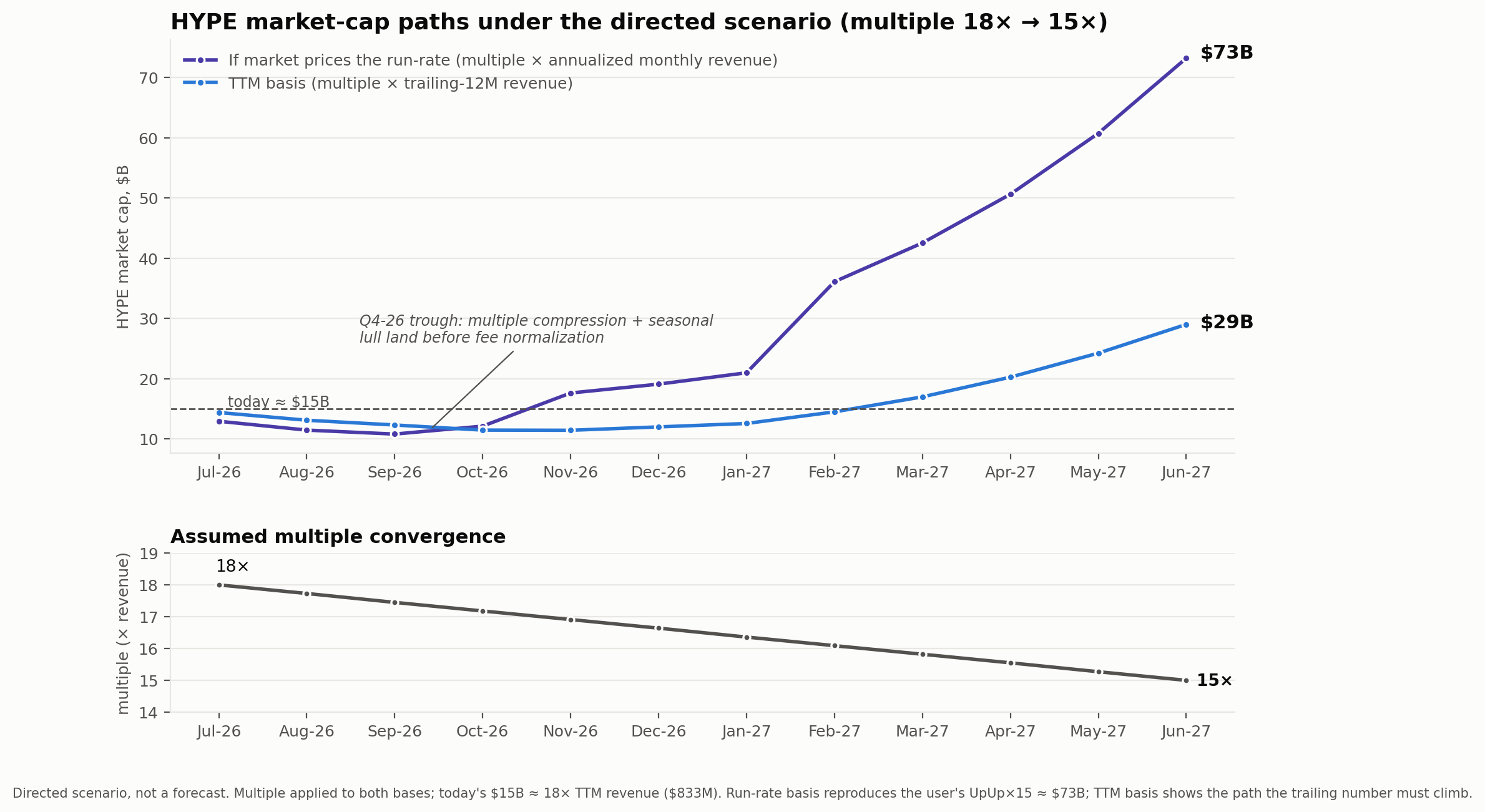

Take a small assumption: that 50% of the entire market comes out of growth mode. We could reach $100m plus in monthly fees from HIP-3 alone, and TradeXYZ alone is able to reach a TTM fee number above $1b - meaning over $500m distributed directly to Hyperliquid. Keeping the same MCap/Fees ratio we are currently trading at, 17.9x Price to Fees, we reach a HYPE valuation, from HIP-3 alone, of above $9b.

Add the numbers from crypto, even predicting that crypto markets remain stable, without the “comeback” we are all waiting for. Hyperliquid is printing $58m in monthly fees from crypto trading; taking off the 1% HLP fee, we have more than $57m of monthly economic value being distributed to HYPE holders. Together, the non-HIP-3 and HIP-3 monthly economic value directly distributed to HYPE holders will be above $100m a month - taking the assumption that perp volume keeps growing once growth mode is off for half of the instruments, and that TradeXYZ remains the monopoly deployer. Competition will push volumes even higher but eventually fees lower, so one will balance the other; I am not taking a big net view on fees generation as the number of deployers increases through competition.

Put together, we are predicting over $100m a month of direct HYPE-holder economic value - meaning above $1.2b of annualized revenue - which at PE ratio of 25 (using the last TTM values for comparison) puts HYPE’s MCap valuation at $30b: +100% above the current market value of $15b MCap.

It also signals a rotation in dominance from the crypto markets toward the HIP-3 markets, where HIP-3 penetrates the dominant crypto market. HIP-3 penetration will not only dominate perp volume - it will also dominate the entire HYPE-holder economy, completely decoupling HYPE from BTC trading. Eventually, through year-end (with all the further catalysts), it dominates over 50% of all fees generated inside the Hyperliquid ecosystem.

Four Scenarios, One Expected Value: $17.4b

Let’s run a specific scenario analysis, taking some assumptions, to further understand the upside against the downside on the underlying instrument. There are four types of scenarios: Down, Stable, Up and UpUp.

The Down scenario is one where HIP-3 is completely hit by regulation: TradeXYZ gets penalized, charged, and made illegal in all countries for providing unregistered futures, plus all sorts of charges for illegal conduct that could happen. (It is a non-zero probability, but a lot smaller under the current Trump administration.) In this scenario, HIP-3 volumes go almost to 0%; other competitors probably emerge, but realistically volumes go down 90%. In this scenario I also predict new volume lows for the non-HIP-3 markets, everything affected.

In the Stable scenario, I expect the non-HIP-3 and HIP-3 values to remain stable - nothing changes, but June monthly volumes become annualized volumes by repeating the last month every month. (We could see a relatively high probability of this through year-end: as TradeXYZ consolidates the market, “growth mode” tends to end - it would probably end if volumes consolidated, but we did not assume that here).

In the Up scenario, it is both a positive +15% MoM increase for HIP-3 - doubling monthly volume - and crypto volumes growth in portion to last month growth. Here we are also predicting that growth mode is off for at least 50% of the instruments: as TradeXYZ consolidates and increases the number of instruments, it will remove growth mode as many more instruments consolidate.

In the final scenario - an extreme bull market - all assets’ volumes rise: non-HIP-3 volumes reach the previous August 2025 highs, and HIP-3 volumes double the non-HIP-3, with “growth mode” stopped completely. HIP-3 is now the dominant market for Hyperliquid, no growth mode is required, HIP-3 turns on the printing machine - and it becomes the major HYPE-buying force.

In these scenarios we are representing the spectrum of possible future outcomes. The base case is a combination of continued HIP-3 growth (Up scenario), a reduced number of instruments under “growth mode” (at least 50% of the current instruments off), and the crypto market remaining stable at last-month values (Stable scenario).

By assigning different scenario probabilities across core states and HIP-3 scenarios, we reach an EV of $17.4b MCap, on $1.1b of EV annual revenue and a compression of the multiple from 17x to 15.7x. The most probable scenario is the Stable core-state paired with the Up HIP-3 scenario, at a joint probability of 21.1%. The probability of doubling the market cap sits at 12%, and there is a 40% probability of trading below the current market cap, $15.3b, under these conditional (subjective, in my own opinion) scenarios.

At Current Prices, the Upside Is Limited

In a way, the price already reflects HIP-3 growth and a stable crypto market - so at current prices, the upside for HYPE is limited. If any data point suggests a change in these probabilities, it of course suggests a market valuation adjustment - but so far, at $15b, HYPE is pricing in all progress under my rational conditions. Around a $10b market valuation, it could offer an upside that would be super interesting for taking long exposure. I see huge upside across all market valuations for Hyperliquid, and for really long-term bets we could raise the probabilities of certain scenarios. For that, we should measure how big the market is. If Hyperliquid is aiming for bigger plays, how big is that market - how big is the TAM - is the only question that deserves an answer from me. And what is the reachable market for Hyperliquid, as a decentralized, networked, perp-led platform?

The Blue Sky: Sizing the Everything-Exchange

HIP-3 traded $86b in Jun-2026; if we annualize it, that reaches $1.03T in annual trading volume, in US notional. It is a non-zero value, but in comparison to other markets it is a very small number. FX spot trades $750T in annual notional; cash equities $360T in annual notional; equity index futures $335T in annual notional; commodity futures $134T. That makes the total TAM $1,639T, the retail-leverage SAM $420T, and the reachable-market-adjusted SAM $250T. $1.03T is a pickle on these massive burgers.

Annualizing the current HIP-3 market values, we reach less than 0.3% market share of the first layer - “L1 – Retail-Leverage SAM” - and 0.4% market share of the second layer - “L2 – PERIMETER-ADJUSTED SAM (de facto reachable)”. There is upside in capturing share of a market that already exists, and Hyperliquid can compete by providing innovation, openness and frictionlessness. Even a move to 1% triples the metrics - meaning we reach our UpUp scenario.

The blue sky for Hyperliquid is the initiation of the perp-equities era on the Hyperliquid platform.

It is a new, innovative product that did not exist before: it started with crypto tokens, and it is now being pushed to tokenized RWA. The perp/spot ratio in curated venues for BTC is 4-6x (with spikes above 20x). Consider the same perp/spot ratios for cash equities volumes as BTC has: on above $360T of annual volumes, that could represent $1,440T - $2,160T of annual volume for equity-perps - the reachable market. Even if perpetual contracts become standard in all platforms and Hyperliquid reaches a 1% dominance share, that should represent $21.6T in annual volumes - 21.6x the last month annualized, and 9x above the UpUp scenario: an extreme upside surprise. And we are not even considering the perpification of index ETFs, commodities, FX and others. CFDs represent a kind of similar product to perpetual futures, at least from the view of retail and leveraged trades; but, perps are a clear substitute for them, with a much better and more efficient derivative product.

TAM and future catalysts provide huge upside for Hyperliquid, the HyperCore network, and HYPE holders. But this is still a less predictable scenario: a lot has to be true for these outcomes to become possible. And it is not the case that the long term increases the probability of it happening, because of the regulatory unclarity.

The long term increases the probability of these extreme positive outcomes happening - if regulatory pressure is not considered. If it is taken into consideration, then the longer the time horizon, the more it also increases the risk of regulatory pressure. We can’t expect a decentralized protocol to control 10% of the world’s perpetual derivative volumes without clear and enforceable action from some major government. We are also not saying that Hyperliquid management lacks the ability to navigate those regulatory waves and create their own regulatory moats. But it is a super wide spectrum.

Time the Buys, Don’t Price the Buys

We always try to price the asset, but we could also try to time the buy, as Philip Fisher under the chapter “Five more don’ts for investors”, rule title “Don’t fail to consider time as well as price in the buying of a true growth stock”.

So, let’s try to analyze Hyperliquid’s fundamental value as we live through the summer. It is the time of the year when financial people go spend their bonuses on boats on the Mediterranean, open bottles at private clubs on the beach, and spend their 2-week unlimited-budget vacations. Market activity and high-value decisions are patiently put to the side, to be decided when all the analysts and seniors are back in the office - back to normal life, as the hot weather turns cold in New York City.

Let’s try to measure the seasonal impact of summer on Hyperliquid’s fundamental value numbers, through HIP-3 volume performance. Backtesting the historical performance of the S&P 500 shows that August and September are the worst months for S&P 500 performance - these two months, since 1950, have a negative monthly average return.

It is not only asset performance that declines in summer. Trading volumes (predictably) decline 12.5% on average (a midpoint of 10% to 15%), and CME volume declines roughly 9%.

Even if Hyperliquid’s history doesn’t show the same type of pattern, this is the first summer that HIP-3 is live and running. Until now, Hyperliquid’s volume numbers tracked the crypto industry. Now that Hyperliquid is deviating from it, this could be the best year for it: through HIP-3, volumes could be impacted by the “Sell in May and go away” mentality that has clear expression in tradFi assets.

It is still an open question whether seasonality is real for tokenized RWA perpetuals. This year will provide some signs of that, but I could see a high probability of it being the case - with August and September being the worst volume months for HIP-3 compared to all the months ahead, until July-2027 comes around again.

If this is true, we should attempt to time the buys, not price the buys. We should buy (no matter what) mid to late September, under these conditions, as we predict clear, highly probable future upside starting after September.

Big Note: HIP-4 Is Excluded on Purpose

In this research I am excluding all data for HIP-4, on purpose. HIP-4 could also be a huge driver of HYPE value - from prediction markets, but mostly by allowing the creation of options contracts. That is a market that trades $605T in SPX annual options notional. HIP-4, if well executed, could be the third driver of HYPE upside, with a force that could double the HYPE upside, and it could collide with the bullish season - but more data must signal that upside before I consider it a non-delusional, probable scenario.

Thanks,

Joao