If GOLD was a blockchain do you still use network REV to value it ?

Equity type frameworks don't work to value commodities. BTC, ETH, SOL (L1 tokens) are commodities. You can't use equity valuation frameworks to value these L1 tokens. Doesn't work.

On this paper, GOLD is a blockchain. The entire supply is trackable and it drives on a proof-of-staking architecture.

The idea here is to explain why equity valuation frameworks don’t work on commodities. Try to assume that ETH, SOL and other L1’s are extremely overpriced based on multiples, it is exactly the same that GOLD and any other commodity is overpriced based on their multiples. Historically proved it doesn’t work.

I will try to determine what is the Network REV for GOLD, and the current multiples based on that.

(I’m aiming to discuss correct valuation frameworks. And try to disseminate markets misunderstands. Markets are not dumb, they are pricing everything correctly.)

Imagine that a commodity like gold runs entirely on a blockchain, similar to Ethereum, Bitcoin, or Solana. In this scenario, 100% of the gold supply is trackable, transparent, and verifiable on-chain.

We can assume a total supply of approximately 250,000 metric tons currently in circulation. Every year, mining production introduces roughly 3,000 to 3,500 new metric tons into the system.

In blockchain terminology, this yearly production is the “issuance” - the inflation rate where new supply comes live. If we multiply the total supply on the blockchain by the current trading price, we arrive at a market capitalization for gold of roughly $27 trillion. This analogy can apply to any commodity, but gold serves as the perfect proxy for this analysis, because it already proved their value.

Within this GOLD ecosystem, there are specific actors driving the market.

First, you have the investors, who fall into two categories: the fundamentalists and the speculators. The fundamental investors view gold as a reserve asset - a hedge to protect their wealth against the stock market or inflation, holding it for five or ten-year horizons. The speculators, on the other hand, trade in and out based on daily, weekly, or monthly volatility, aiming to profit from short-term demand and supply fluctuations.

Alongside these traders are the producers. In the real world, these are miners who invest in manufacturing plants, labor, and machinery to extract gold. To prevent supply shocks that would crash the price, they must manage how much supply is injected into the market.

If we translate this production layer to a Proof of Stake blockchain, the “miners” are replaced by “stakers.” In a Proof of Stake system, you don’t need physical manufacturing plants; you need the underlying commodity itself. The amount of the commodity you hold (stake) plus some hardware represents your mining power. By locking up this capital to provide security for the network, you earn the right to “mine” new units. These rewards - the issuance - become the revenue for the producers. This creates a closed loop where holding the asset allows you to produce more of it, securing the network in the process.

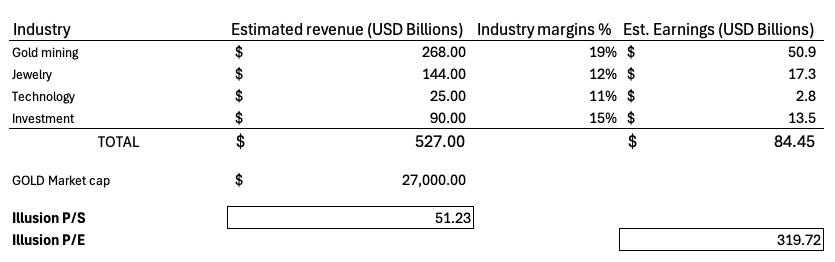

However, the ecosystem relies on a third, crucial group: the businesses that utilize the commodity to create products. In the gold industry, these are jewelers, technology manufacturers, industrial companies and investment companies. They buy gold from the producers and manipulate it to manufacture goods or services, adding marginal value to the raw material to serve consumer needs. Effectively, they are the source of demand, buying and “diluting” the raw supply to create finished products.

If we try to determine the “network value” of gold by looking at these underlying businesses, we run into a major valuation disconnect.

But, let’s do that.

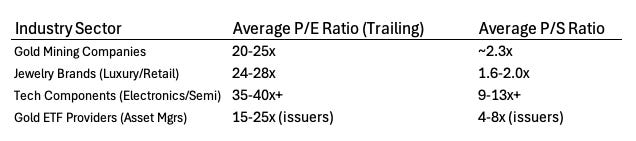

If we aggregate the revenue of all the businesses built “on top” of gold - mining companies, jewelry brands, tech components, and investment firms - we see a total revenue of roughly $527 billion (based on 2024 estimates). If we compare this revenue to gold’s $29 trillion market cap, we get a Price-to-Sales ratio of 51x. If we look at earnings, the Price-to-Earnings ratio would be roughly 320x. These multiples are astronomically high compared to standard equities.

If you tried to value the gold commodity based on the earnings of the businesses using it, you would conclude that gold is massively overvalued, and has being all the time. But that conclusion would be wrong, because the value of a network commodity cannot be measured by the P/E ratios of the businesses built upon it.

This brings us to the core issue with valuing Layer 1 blockchains like Ethereum or Solana. Analysts often try to value these networks by looking at the network revenue generated on the blockchain - revenue generated by the stakers and businesses on top of them. Each Fee or MEV tip that the blockchain “earns” correspond to fee that one application is also earning and/or a fee that is being distributed to stakers (the commodity do not absorb the value).

This is a flawed framework. You cannot use the “network revenue” of the applications to determine the fair market cap of the base layer commodity. The businesses (or dApps) create marginal value and have their own distinct valuations based on their specific earnings.

However, the base layer - the commodity itself - holds a network value premium that far exceeds the aggregate earnings of the companies utilizing it.

While Layer 1 blockchains are arguably more valuable than gold - because the utility is programmable and intrinsic to the digital substrate without the high physical manufacturing costs - the valuation logic remains the same.

You cannot use the same framework to value commodities as you do to value securities.

Attempting to judge the value of Ethereum or Solana based on a Price-to-Sales ratio derived from their dApp ecosystems will result in incorrect numbers, just as it would if you tried to value gold based on the earnings of a jewelry store. The commodity supports the economy, but its value is derived from its role as a reserve and a standard, not merely the cash flow of its users.

The end goal is not to mirror gold to any other L1 blockchain token perfectly. It is that trying to value commodities based on equity valuations is like measuring love with a ruler. Won’t work. You end up calling gold as any other L1 token absurdly expensive or overcooked.

Collapses comes from silence, not spreadsheets - from devs and users ghosting, applications failing, bridges freezing, trust evaporating - not because a ratio screamed bubble.

Ditch the multiples, track stickiness. If tomorrow nobody needs Ethereum/Solana or any other blockchain the way phones need gold wires, it’s dead. No fancy math required.