Is AI going to fire 72 million Americans? Who pays their credit loans and mortgages?

[Brief in Audio version]

I’m trying to connect the dots here. While I’m reading a lot of different opinions, the discourse seems to range from apocalyptic to utopian in both directions. While everyone else is trying to answer the critical question of whether AI is “good or bad,” I’m looking for a clear answer to a more specific concern: Is AI good or bad for my bags? Right now, there is no clear answer; that is my first conclusion, and that is why I’m nibbling on this topic.

For this research, I will use my own knowledge and three specific sources: Arthur Hayes’ latest article; Michael S. Burr’s recent speech; and my notes from the latest All-In Podcast. All three are deeply connected, touching on different but interconnected dots. To start, Michael S. Burr mentioned three possible scenarios for AI in relation to the labor market:

Normal: A scenario of gradual adoption.

AI Bull: A scenario of rapid growth in AI capabilities and adoption.

AI Bear: A scenario of stalled growth in AI capabilities and adoption.

In the gradual adoption scenario, AI integration occurs slowly enough that widespread joblessness is avoided. Unemployment might rise in the short term due to skill mismatches, but education and training adjust over time, allowing workers to successfully retrain or find new roles.

In the AI Bull scenario, capabilities grow exponentially. Adoption is so rapid that it ushers in a “jobless boom.” AI agents replace a vast range of professional and service occupations. AI-centric startups with radically new business models displace firms unable to adapt, and layoffs soar. This leads to widespread unemployment and a decline in labor force participation, as a large share of the population becomes essentially unemployable.

In the AI Bear scenario, growth stalls. This might occur due to the exhaustion of training data, a shortage of electricity to satisfy data centers, or a lack of capital required to build new infrastructure. An AI “bust” occurs, abruptly ending investment; interestingly, this would hurt the financial sector more than the labor market.

The distinction between these three scenarios allows us to organize a model to understand which is most probable. However, Michael doesn’t explicitly relate the impact on unemployment to debt defaults—and how that could impact the banking sector, which is a critical component of the Hayes paper. When we connect these dots, we see that the relation between AI-driven unemployment and debt defaults could result in massive losses for the banking sector.

This technological revolution—which we all call AI—is a force that, in an “AI Bull” scenario, targets white-collar jobs first. Blue-collar jobs remain safe for a bit longer, only being threatened when the second wave happens: a physical AI revolution. This would involve autonomous manufacturing, vehicles, and humanoid robots substituting the entire workforce required for manufacturing or housekeeping.

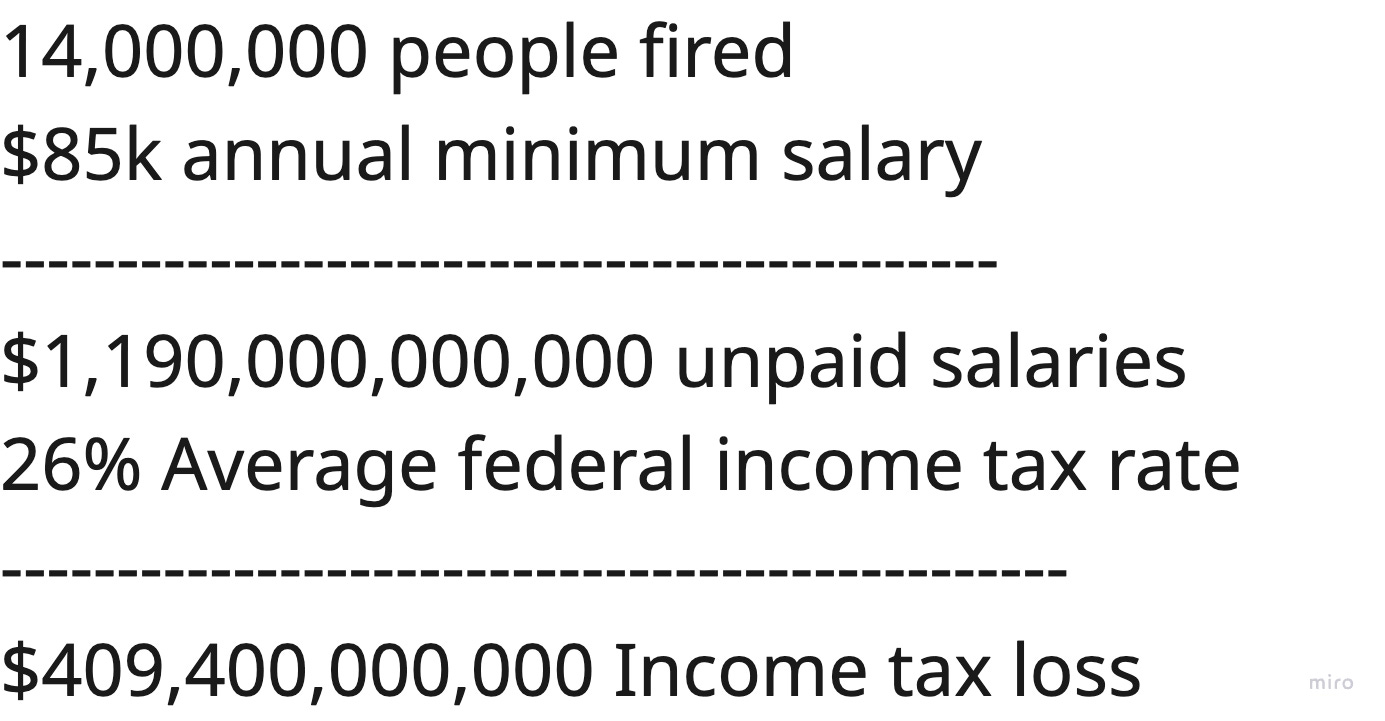

It is clear that Arthur Hayes assumes the “AI Bull” scenario. He sees white-collar knowledge workers being replaced by AI tools like Claude. White-collar jobs represent roughly 43% of the US workforce—72 million workers who earn above-average salaries and power the empire’s consumer-led economy. In this social class, 74% own a home, and 42% of those homeowners have a mortgage with an average balance of $250k. Doing the math, there is roughly $5.6T in mortgage loans tied to this group.

Underwriting these loans is easy for this “$85k plus” annual salary class; they are viewed as low-risk borrowers. But in an “AI Bull” scenario, corporations will quickly fire a sizable chunk of these workers if AI tools are 10 to 100 times faster than a human. A complete eradication of most knowledge work would kill these mortgages. If we consider only a 20% mortgage default rate, it represents $1.1T in mortgage losses and $227B in direct banking losses, according to Arthur’s numbers. If you include consumer credit of $3.7T, you add another $330B in losses for the banking community.

In short, a 20% job loss in the white-collar sector could lead to a banking equity drawdown of 13%—almost half of what it was during the 2008 Great Depression. This creates a much worse scenario for thousands of consumer banks that will suffer even bigger losses because by trying to compete with “Too Big To Fail” (TBTF) institutions, they end up with higher leverage and higher exposure to defaults.

Arthur doesn’t discuss the impact this 20% white-collar firing would have on government revenue. Assuming an $85k salary for 14.4 million fired people, that is $1.2T in lost salaries. At an average federal tax rate of 26%, this represents over $300B in lost income tax for the government. Even worse, that $1.2T will no longer flood the economy in the form of spending. This reinforces the theory of massive future money-printing by Western civilizations; I am simply adding an extra layer to the Hayes theory.

In this “AI Bull” scenario, the assumption is that AI will be so disruptive and infinitely scalable that it destroys white-collar work rapidly. Market participants will assume unemployed workers cannot meet their payments, directly harming banks that won’t even know if the wealthiest workers can earn a living in the age of AI. Without credit, demand for real goods collapses. The economy fails, commercial banks go bankrupt, and only TBTF banks survive.

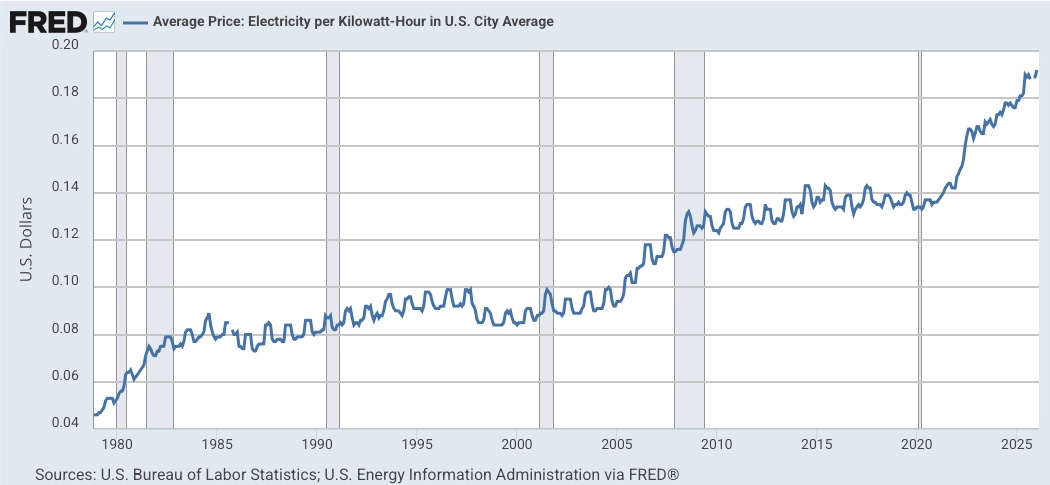

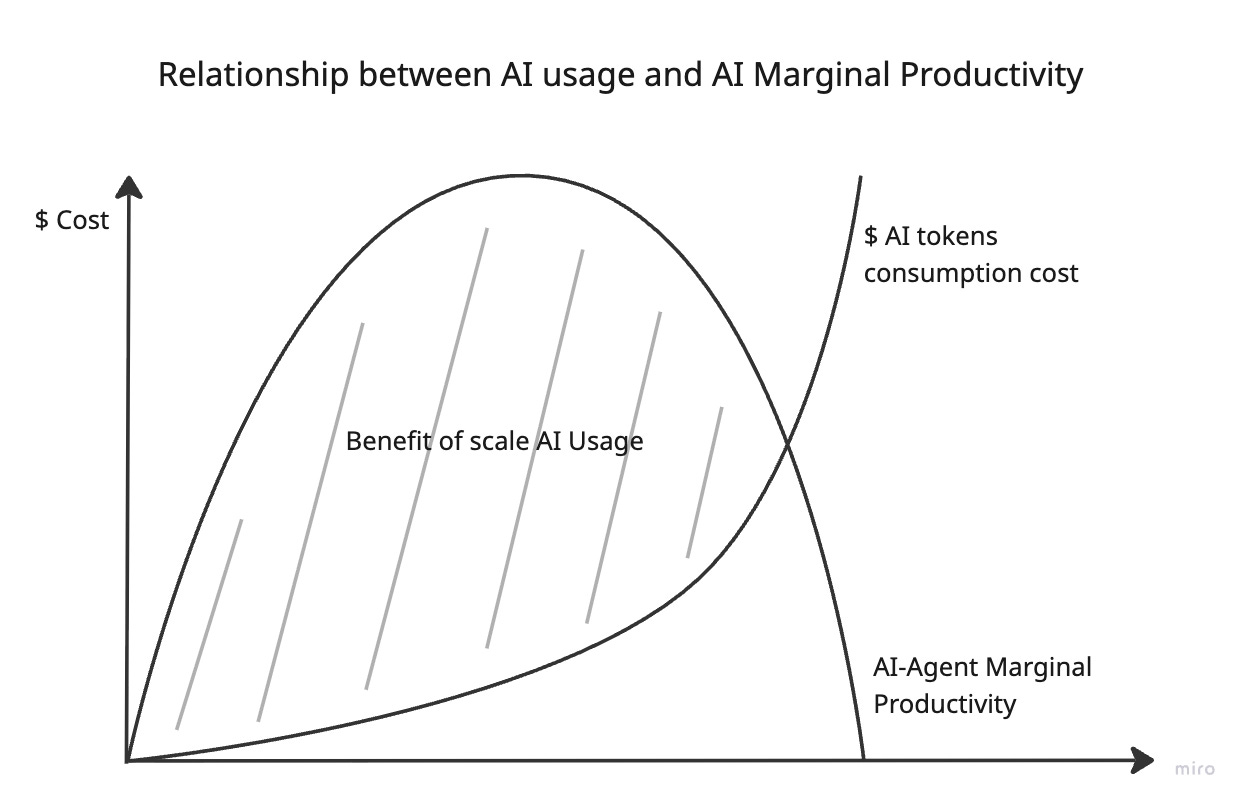

However, there is a major friction point: The Cost of AI. AI cost is a function of CAPEX depreciation + operational costs (Total Power x PUE x Electricity Cost) + Labor/Facility overhead. The cost per token is derived from these variables. It is a fact that CAPEX spending is increasing because technology is evolving so fast; substituting old GPUs is constantly required, which increases the depreciation rate. In a world of limited electricity supply, like the US and Europe, energy prices will skyrocket in an “AI Bull” scenario.

Electricity has a unique characteristic: it is very hard to export and store. It must be produced and consumed nearby. Expanding capacity is slow; solar plants take 2 to 5 years, and nuclear plants can take two decades. Because electricity pricing functions on marginal costs, a supply shortage will cause the cost of AI products to skyrocket. This creates a distinct divergence between the US and China. While the US faces a “supply shock,” China is bringing massive energy capacity online—potentially 3 to 5 times greater than current US capabilities. Because China can physically power the infrastructure, their AI ecosystem may scale while the US stagnates under energy ceilings.

In the US and Europe, the government will have to intervene. Since 37% of electricity consumption is residential, data centers “stealing” power will increase household costs and reduce spending power. Governments will force data centers to subsidize the electricity cost increase, ultimately pushing the cost of AI tokens even higher.

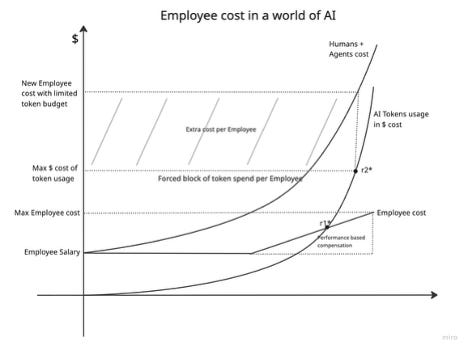

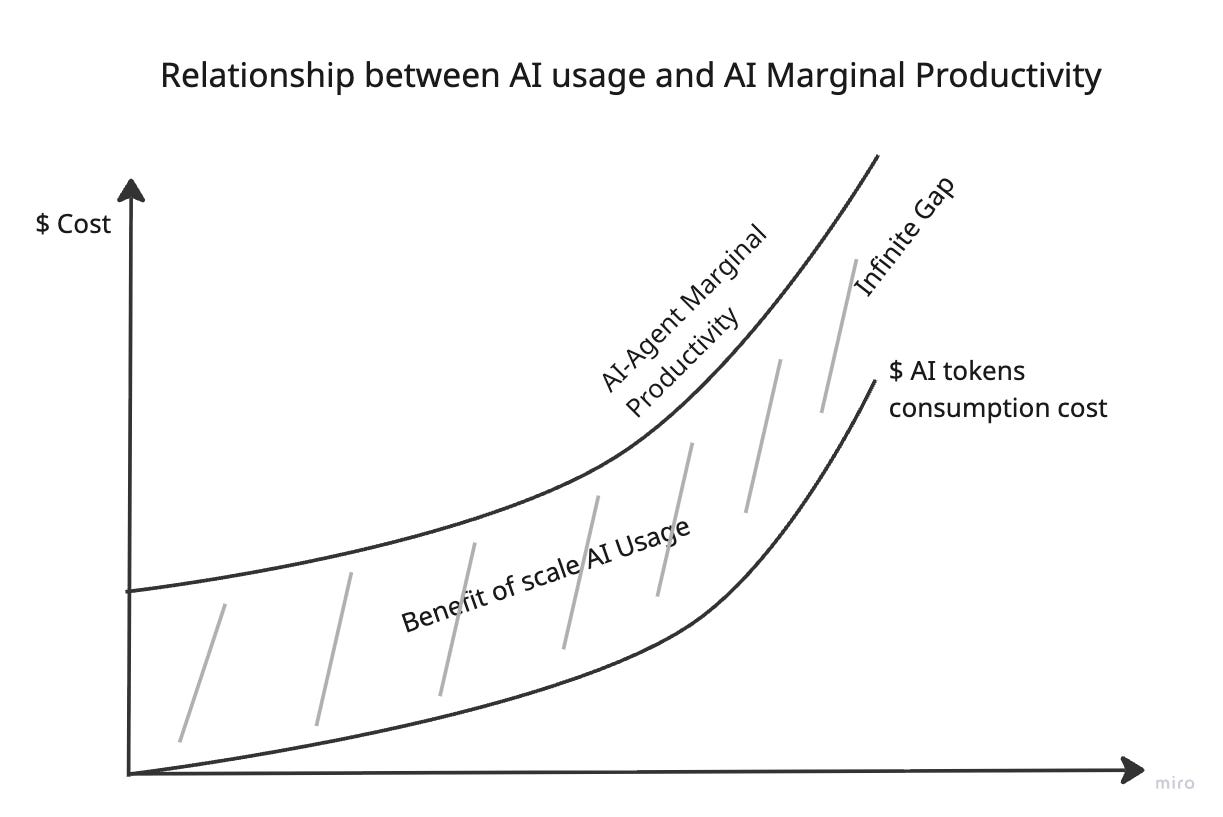

This challenges the “AI Bull” assumption that the marginal benefits of using AI are infinite. That scenario assumes your return is always a positive function of how many tokens you spend.

But the latest All-In Podcast serves as an “oracle of truth” here, providing real-life facts on implementing AI. Jason Calacanis noted that using agents can instantly hit $300/day per agent—roughly $100k/year. This proves that AI costs can scale infinitely and dangerously. In a world of agents, token limitations are not an optional feature; they are a requirement to avoid bankruptcy.

Chamath Palihapitiya added that he now has to set “token budgets” for his best devs. They must be twice as productive, or he will run out of money. This proves that the theory of infinite consumption producing infinite returns is empirically “in the toilet.” Infinite marginal productivity is not true. Success will instead be a combination of cost efficiency and achieving “max profitability” per token without vaporizing net returns.

This reality forces executives to place “hard stops” on token spending. In an ultimate comparison, an organization will only replace a human with an agent if the agent alone is more profitable than the human + AI combo. Noting this, we tend to disagree with the “AI Bull” scenario and incline toward the “Normal” scenario—a less apocalyptic outcome. This is the scenario Michael Burr defends as gradual adoption.

The adoption will be delayed by energy shortages in the West. Some joblessness will follow, but employees who become more efficient will also become more expensive and valuable. I’m not expecting a massive displacement that destroys the banking sector completely. I expect a predictable adjustment in equities as the “expectation gap” between AI hype and real-world cash flows closes. A probable “Normal” scenario is expected, because it will have a weight of both scenarios “AI bull” and “AI bear”, where energy shortage and higher costs delayed maximum development; and AI-first startups and employees substitute analog people. On aggregate should be neutral or slightly positive – “Neutral” scenario.

The only remaining wild cards are China and Military needs. China doesn’t have the energy problem; they are positioned to go “all-in” on the “AI Bull” scenario. With massive bailouts and job displacement, they may print above-average returns, leaving the West behind. This is when the world order changes. As Asian markets print higher returns, US capital will rotate, harming US wealth. This would require another “liquidity bazooka” from the US government to absorb the shock. Gold and Bitcoin are positioned for this event, but the internal tensions in China—as their population suffers through this rapid displacement—will be massive.

Ultimately, all roads lead to the “printing machine.” Whether it’s to subsidize energy, bail out banks, or compete with China, massive printing is inevitable.

Finally, we must consider World War III. This will be a war of agents, cyber attacks, and robot swarms. Because of this, I predict an executive order will eventually redirect a significant portion of the electricity supply to the Defense Department to feed AI manufacturing and military compute. This will limit the quantity of AI tokens available for consumers and companies even further.

Absorbing AI technology is crucial for any person or organization.

The next phase will be blue-collar displacement, and for that, I see a single-scenario outcome: total disruption. If you are a blue-collar worker, don’t sleep. Protect yourself now. Buy stocks on market busts and learn how to communicate with AI agents. If they understand you, you will be safe. If they can’t, you are in trouble.

Time to read again. Time to refine your English and/or Chinese skills.

Official sources:

Arthur paper called “This is fine”

My notes on the paper:

Thanks, Joao