Looking for forward guidance?

Paper deals signed and vessels are crossing. But we still have conferences to watch.

Writing this letter is part of my duty. But it is also a letter. And letters are meant to begin conversations. I hope this one does. I’ll be seeking out a range of perspectives, and I intend to spotlight some the meaningfully advance the discussion.

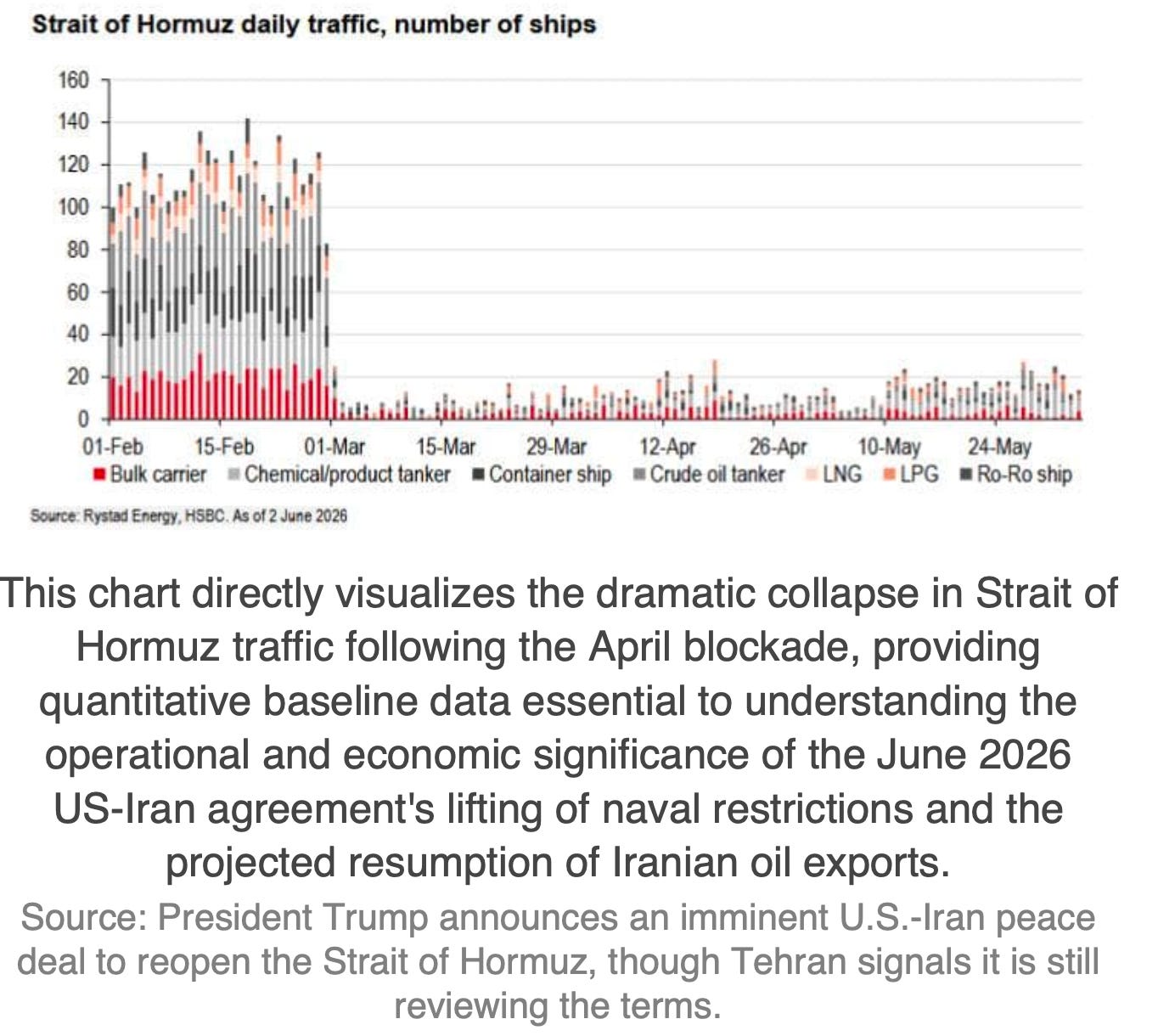

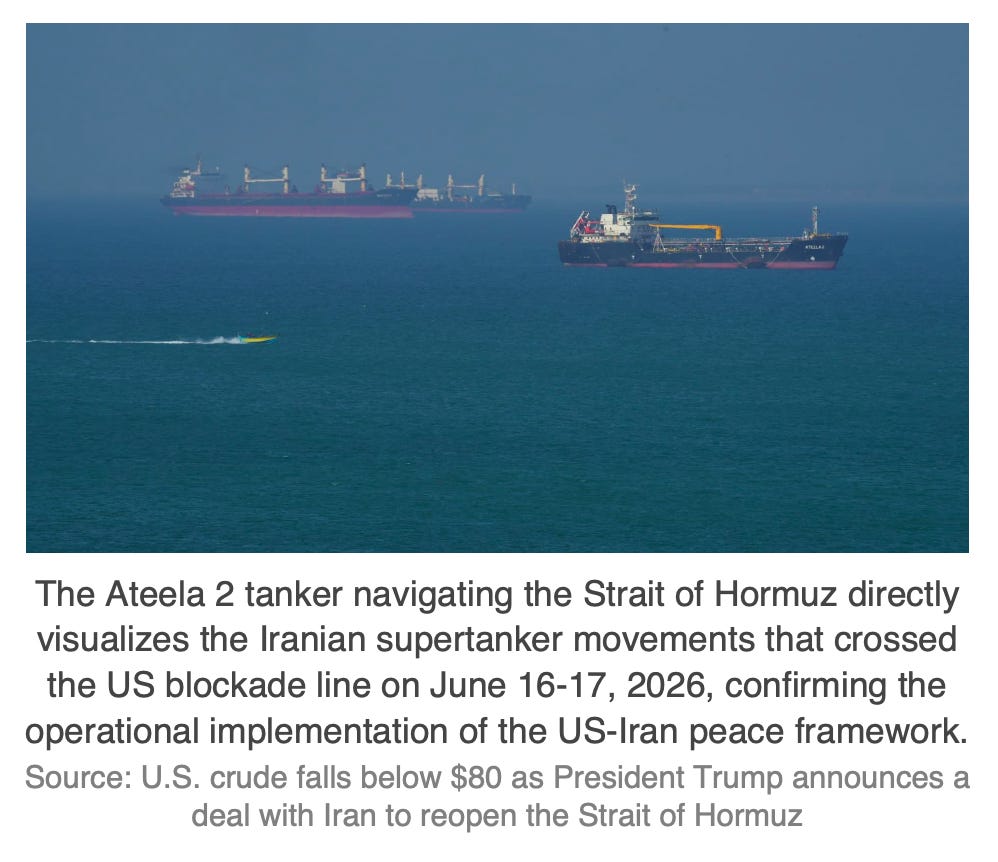

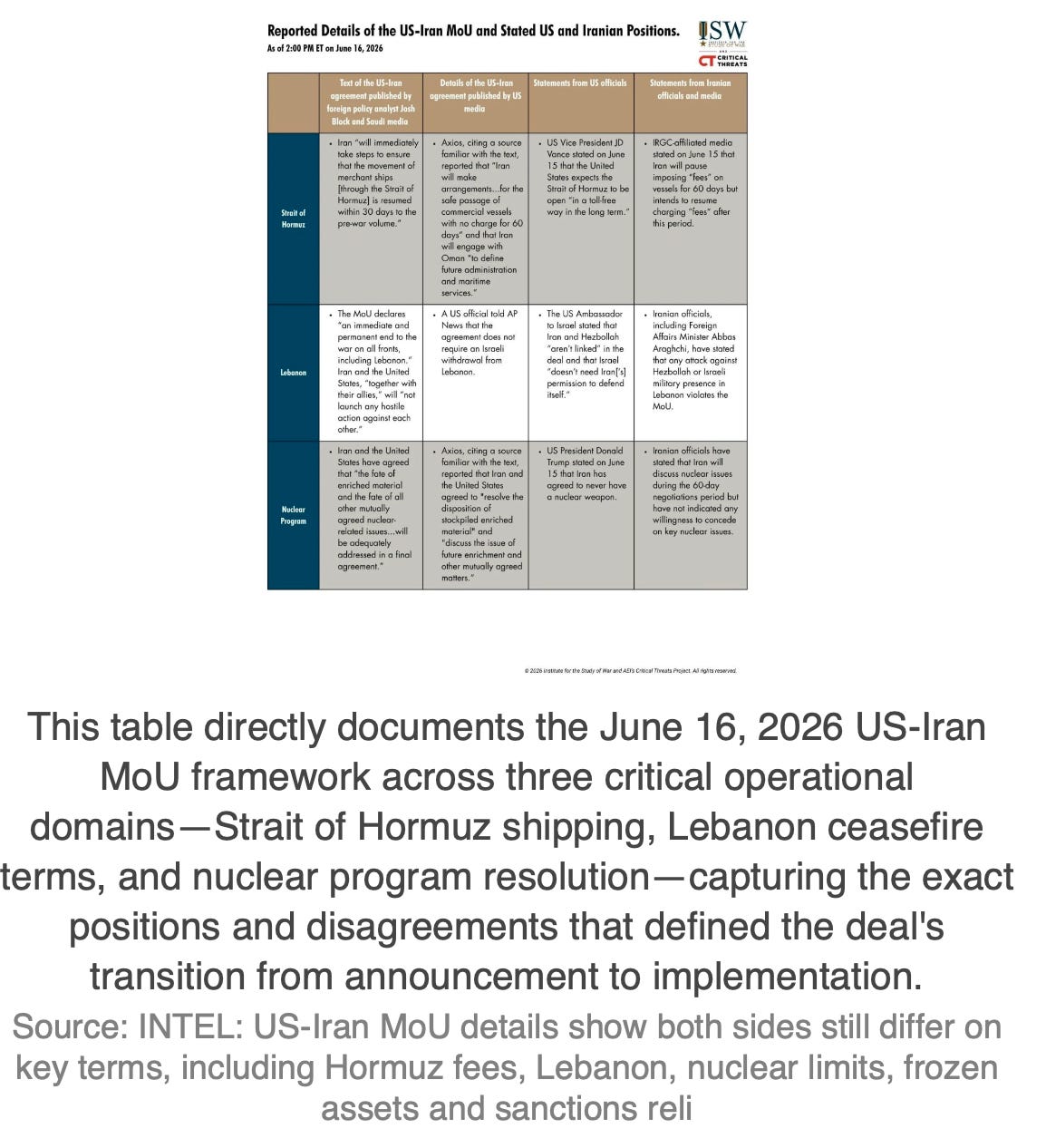

US-Iran peace framework reaches the scope, not only a diplomatic text, paper (digitally sign) but also physical reality of the improvements. Peace framework detailed 14-points co-sign with US and Iranians, and going to formally sign in 19 June – the important Geneva ceremony. The reality is three Iranian thanks pass the US naval blockade, information from Iranian authorities but also confirmed tracked by vessel-tracking technology. These tanks include the sanctioned VLCCs ‘Diona’ and ‘Hero 2’, carrying 3.8m barrels combined, and the third vessel carrying 1m barrels.

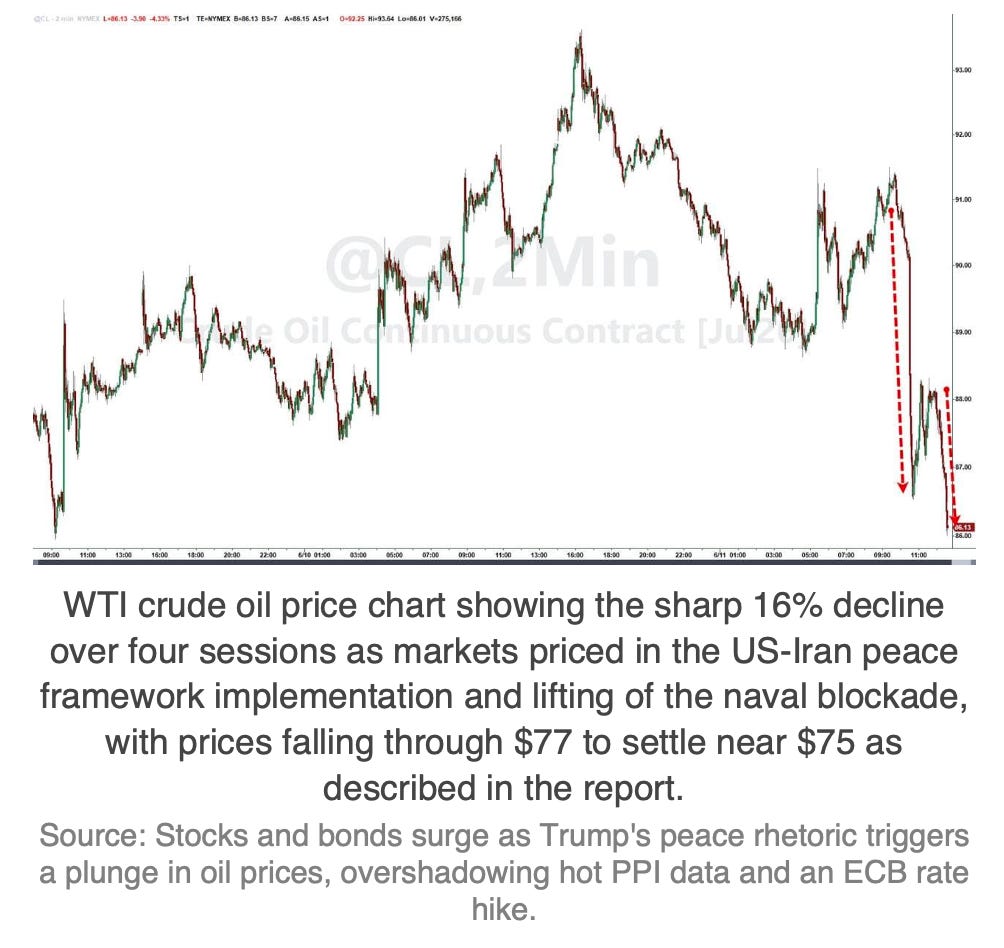

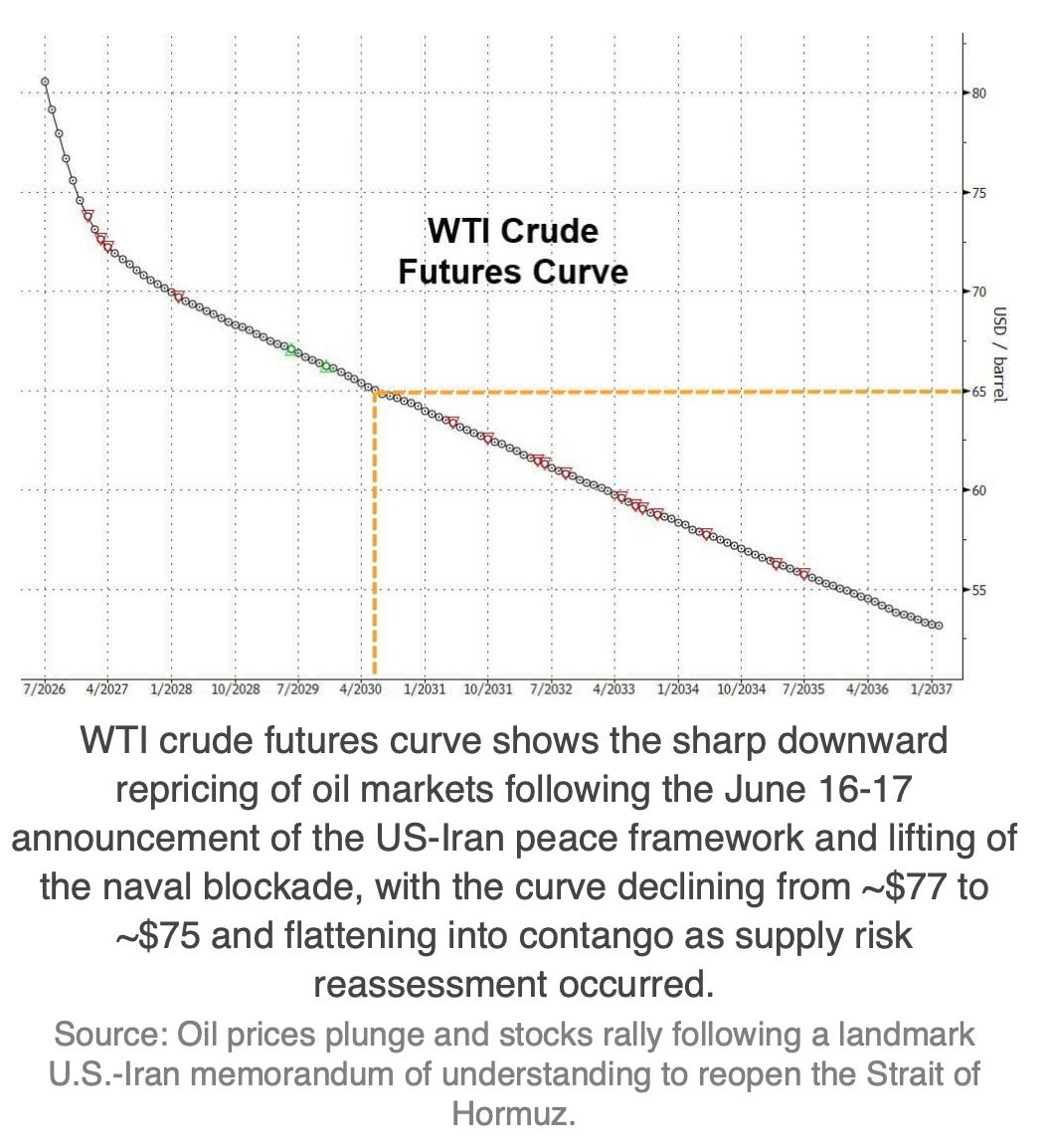

These three vessels crossed US blockade line from Chabahar and the Gulf of Oman with their AIS transponders active (great sign of transparency, the world is seeing). OIL market price reacted sharply, OIL prices down 16% in four sessions, now trading at $74 per Brent.

European countries, G7 nations collectively reaffirmed support for the US-Iran agreement, is it finally European countries and US align or just politics?

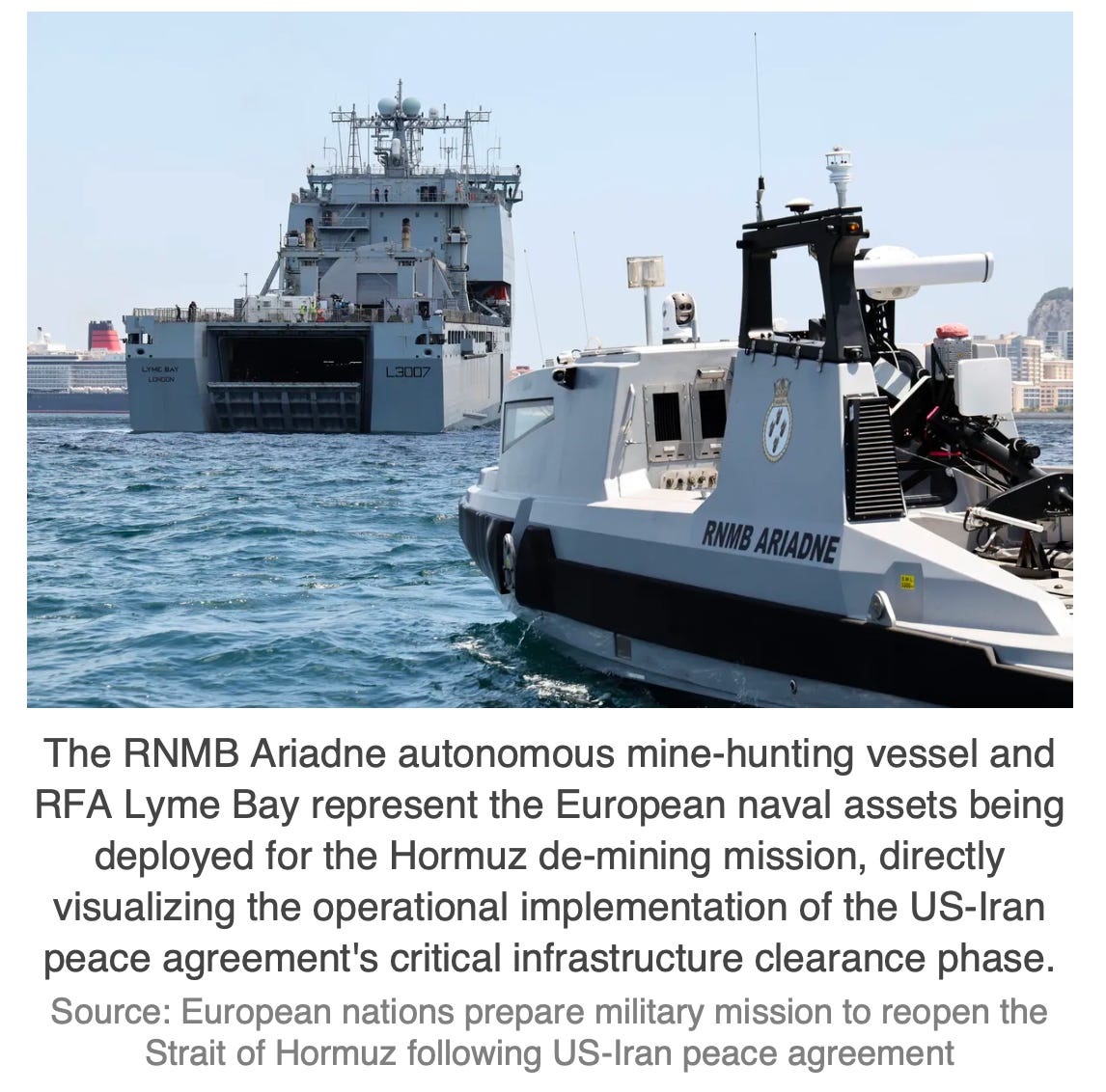

While Trump keeps mention “open by Friday” timeline, there is critical operational constraint: de-mining ships are slow, unarmed, and highly vulnerable. Europe is nations that clear benefit with the rapid opening of the strait - Germany provide support on this mission, France also support personnel and equipment on this mission. But this mission takes time, will not open the strait overnight, it former US Navy officer Ben Cipperley assessed that confidently clearing Iranian mines could require 30 days or more.

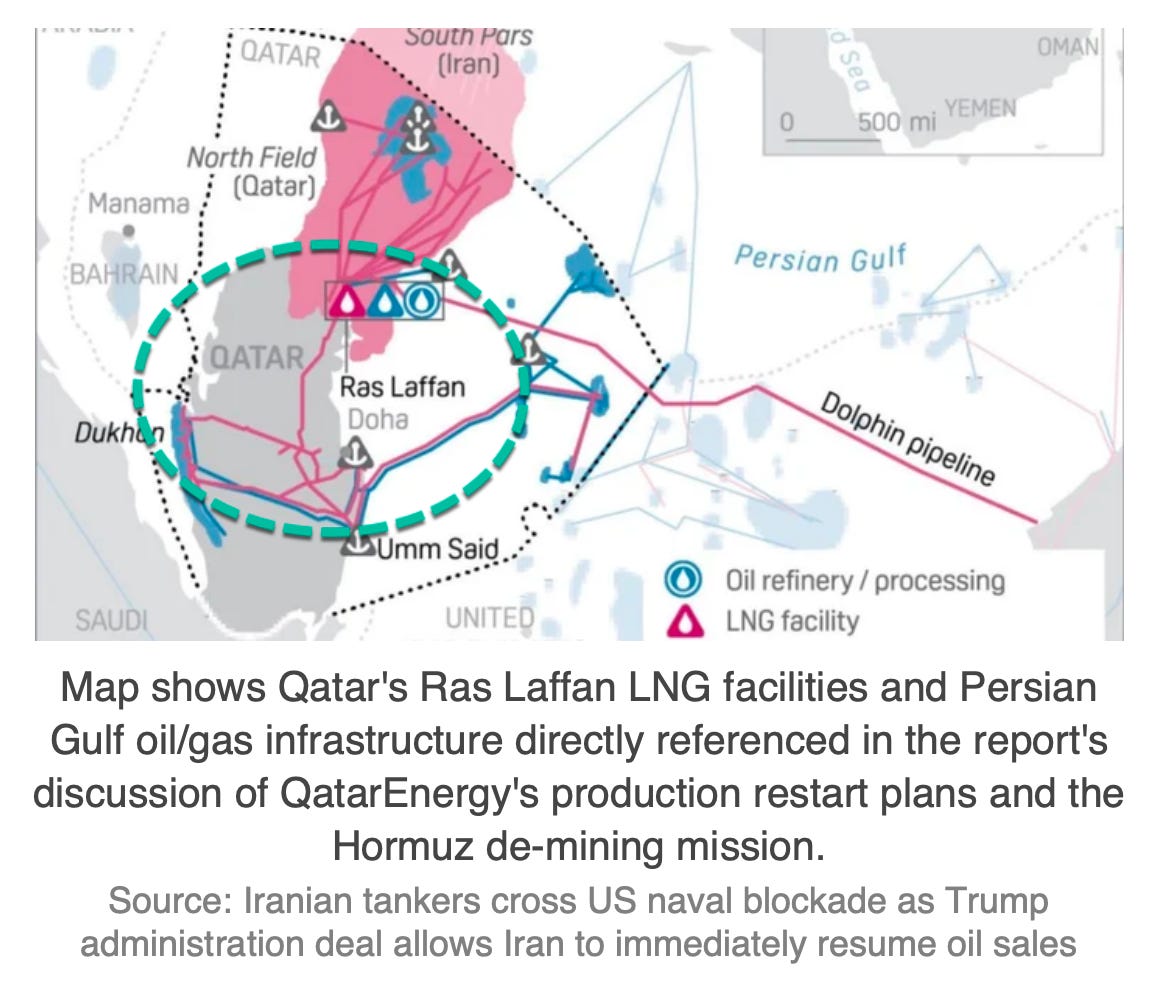

In between QatarEnergy separately confirmed the restore plans, able to restore 50% of Ras Laffan LNG output within one month and 80% with two months. But disclosed the rest have permanently changed by Iranian strikes – requiring 3-to-5 years to replace. This constraint will have clear effect on gas supply in Europe - as European nations are widely dependent in this region, this gas, and have unsustainable reserves to the next winter.

These affects European economic outputs, it’s already bad, and will have a continuously force to get worse, at least to the end of the year, until stagnate through the winter (in a bad spot), waiting to summer to reestablish again the balances. Gas and OIL will trend lower, but will take more time than what politicians are mentioning. Will not be an overnight price convergency to pre-war price equilibrium – and markets don’t agree with that either.

Lebanon is the clear risk, that could disconnect the durability of the deal sign on June 19th. Labanon-Israel front remained in continuously active stress. Iranians warning reiterated, mentioned that Israel is in ceasefire invalidations, that if Israel don’t stop attack Southern Lebanon, Israel should expect a hard response from the Iranian Armed forces. Labanon is one of the four risks that can thread the de-escalation trajectory; the mine clearance timeline is the second; third being the discrepancy between US and Iranian interpretations of frozen asset provisions (it’s unsolved issue); And last but not least the nuclear verification gap – specially uranium sites at Fordow, Isfahan, Natanz, where potentially 441kg of highly enriched uranium and 8,600kg of lower enriched material are held.

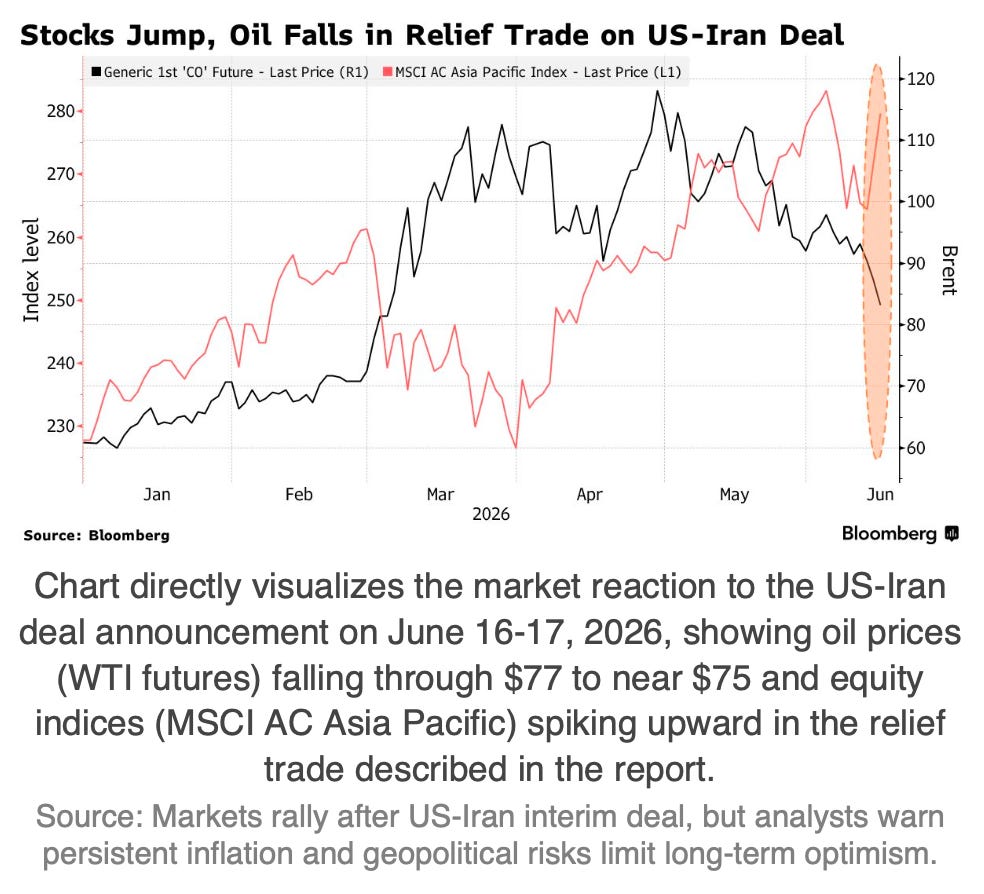

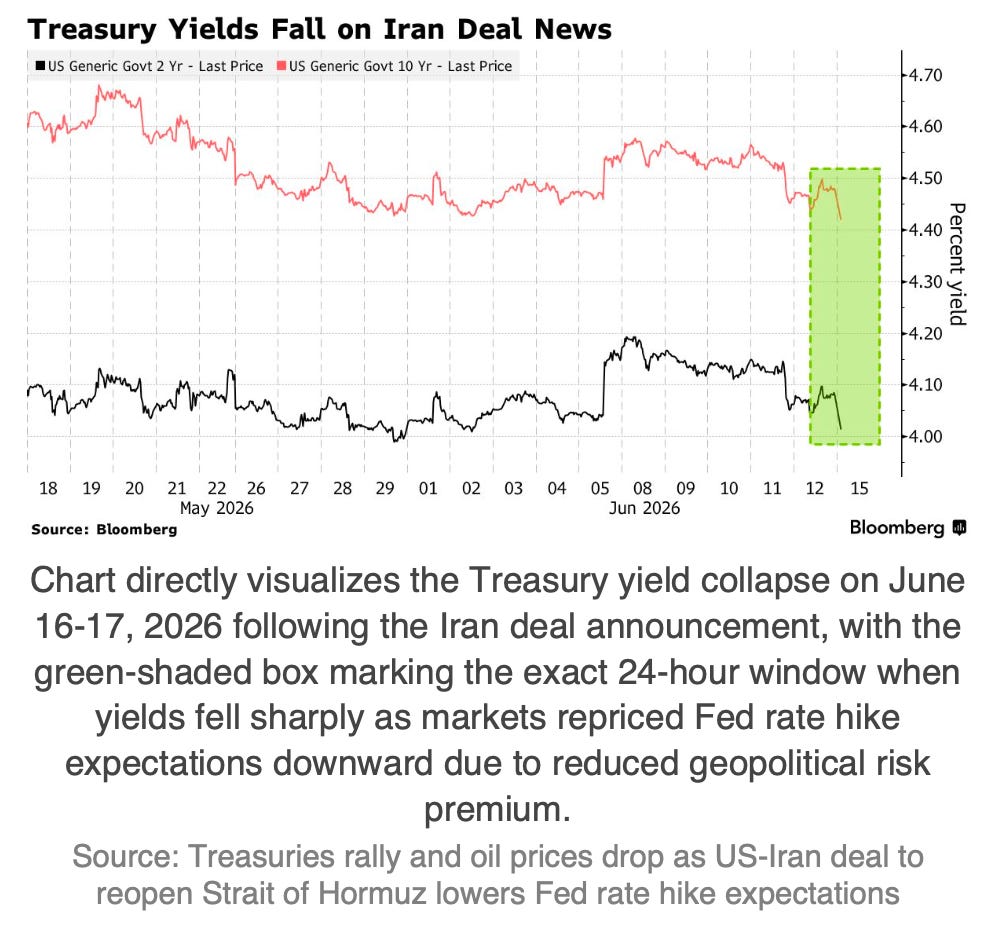

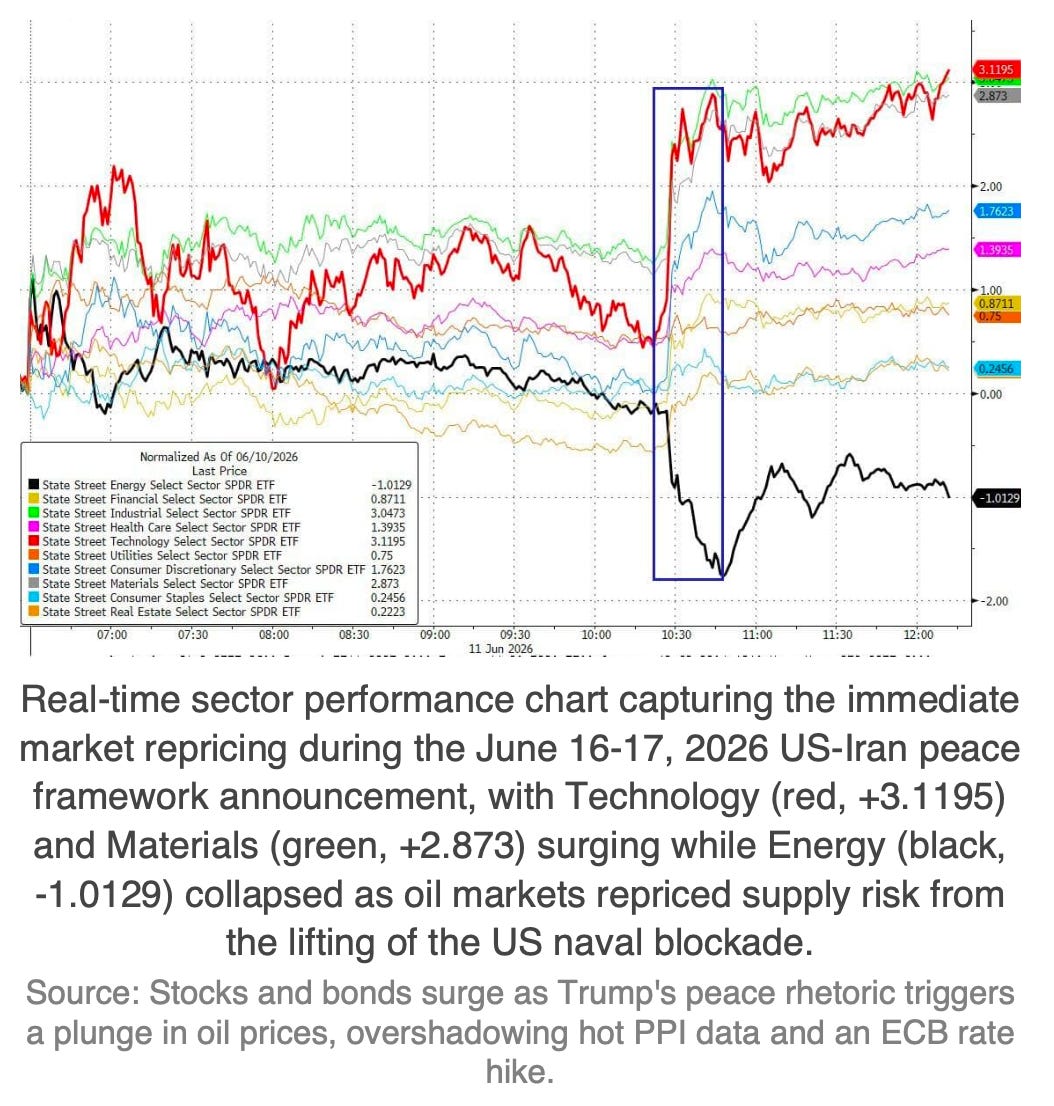

Markets appreciate the relief in Iran-war, there’s direct correlation, as predictable, between the direct decline of OIL, to the jump of the stock market, and the alleviate pressure in the Treasury yields.

Not all sectors benefit equal with lower OIL prices, but technology and industrial sectors clearly benefit with lower prices. OIL. – BRENT or WTI – are directly correlated with their costs, from energy consumption or PPI. Notorious in last PPI reports, the rise of the PPI. By contrast, OIL prices are directly correlated with the revenue size of energy producers – so lower OIL prices affect their revenue, earnings by default, their valuation collapses under lower OIL prices.

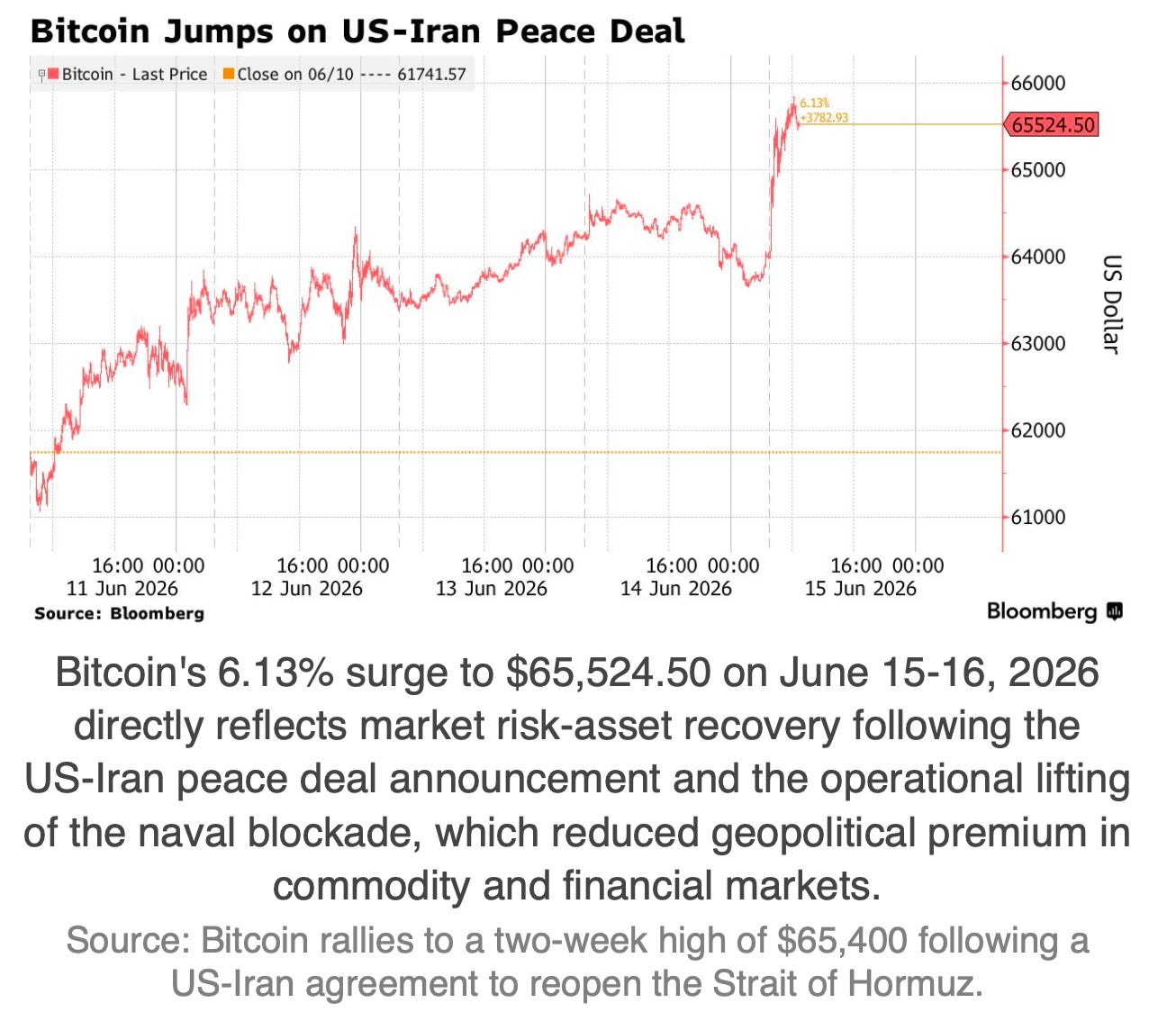

Bitcoin add signal to markets, by agreeing with risk-asset relief, recovering to two-week high on the Iran-deal announcement. This alone means nothing, but it could highlight a move to risk-on, and removal geopolitical premium. Will this sustain overtime, or not, is what markets will determine.

This geopolitical de-escalation – which functioned as a global stagflation shock since late February – reduce the inflation expectations reducing the probability of a December 2026 Fed rate-hike from 80% pre-deal to approximately 65%. With automatic retreated of the two-year yields from 4.15% towards 4.02%-4.05%. Yet inflation data in hands prints May CPI at 4.2% YoY (higher, and well above the benchmark) and May PPI at 6.5% YoY;

May import prices at +6-7% YoY, and forecaster core PCE at approximately 0.35% MoM implying a 4.1% six-month annualized rate. These data doesn’t sound good for easing policies.

Today is highlighted by the first Kevin Warsh FOMC meeting happening, will be first signs of policy aggressivity, policy changed, calculations change or a nothing burger. Today we will have the first signs of how Warsh policies will be.

This meeting is highly anticipated as it marks a major regime shift in FED leadership and communication. Chairman Warsh has signaled plans to overhaul central bank communications, pulling back frequent public speaking and detailed forward guidance to preserve policy flexibility. Markets are expecting a held steady at 3.50%-3.75% but the focus will be on the removal of any remaining easing bias: While CPI and PPI is hot, demand is also hot. And supply side pressures memory cost to surge.

Thanks,

Joao