Meteora (MET) TGE playbook

TGE trading strategy

(NFA)

Meteora is set for its TGE on October 23. To evaluate how to trade the MET token during this event, we should analyze how similar projects are performing, the overall DEX market conditions, and the potential demand and pricing for MET. Meteora operates as a Solana-based DEX, so comparing it with other DEXs is the right approach.

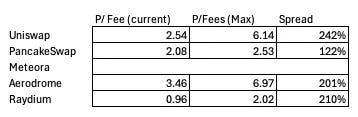

The DEX industry currently trades at a Market Cap to Fee ratio between 1 and 3. Aerodrome shows the highest multiple, while Raydium holds the lowest. Over the past three months, most DEXs have seen their maximum ratios 200% above current levels, except for PancakeSwap, which showed weaker growth ratios.

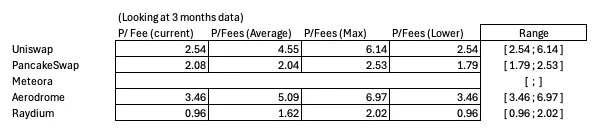

Meteora is likely to trade within the range of PancakeSwap to Raydium multiples. To understand why, let’s look deeper into the data.

The market tends to value projects with a higher revenue share relative to fees, as this directly affects the token’s value. Aerodrome, which distributes 100% of its fees as revenue, trades between 3.46 and 6.97 times its fees. Raydium, converting only 16% of fees into direct revenue, trades between 0.96 and 2.02 times.

Meteora captures about half of Raydium’s revenue share. If the relationship were linear, MET would trade at around half of Raydium’s ratio, or approximately 0.5 Price/Fee. However, that seems too low and not justified.

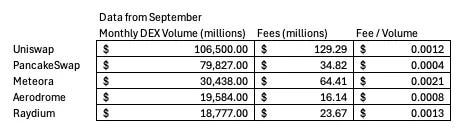

Meteora generates more fees from the same trading volume - almost three times Raydium’s annualized fees — which suggests it operates more efficiently. This efficiency likely comes from Meteora’s mechanisms to capture higher fees during initial token launches and its involvement in the ICM model, which are related to the token issuance.

For every dollar traded, Meteora generates $0.0021 in fees, compared to Uniswap’s $0.0012, a 75% higher fee yield per dollar traded. Against Raydium, Meteora produces 1.6 times more fees for the same trading volume.

It’s also true that the market is pricing each dollar generated in fees on Solana less than in other ecosystems: roughly 80% of BSC’s value, 35% of Ethereum’s, and 30% of Base’s. Base currently provides the highest valuation per fee dollar. These comparisons are based on major DEXs per L1 as benchmarks.

MET’s FDV will likely be capped by Uniswap’s. The market will not support Meteora trading above Uniswap’s FDV. If it does, heavy selling pressure should emerge. Still, based on P/Fee ratios, Meteora could reach similar valuation levels in an optimistic scenario. Meteora’s annualized fees, around $1.3 billion, are close to Uniswap’s, though Uniswap likely maintains higher costs, justifying its stronger multiple.

Meteora should trade above 0.5 in Price/Fee terms. A fair range would be between 0.5 and 2, considering its numbers. It generates significantly higher fees than Raydium, Aerodrome, and PancakeSwap but similar revenue to Raydium, despite capturing 1.6 times more fees per traded dollar. Meteora also has the lowest revenue share among its peers. Uniswap’s revenue share is unclear, and likely near zero, so comparisons should be made cautiously.

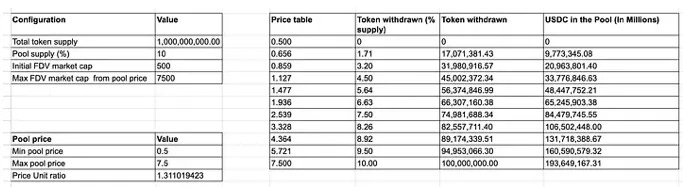

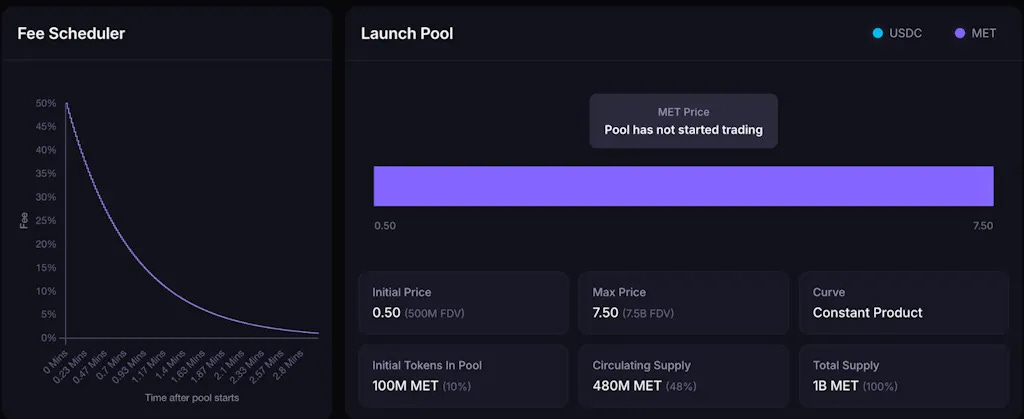

Meteora plans to release 10% of its total supply to bootstrap initial liquidity for MET, with prices starting at $0.5 and going up to $7.5.

Early liquidity will be single-sided, using Meteora’s dynamic AMM model, which applies higher fees at launch and gradually reduces them as trading matures.

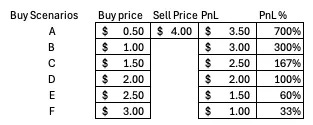

MET could be a strong buy for those able to purchase at or below a 0.5 ratio — roughly in the $1.5 to $2 price range at TGE. It’s reasonable a good hold between $2 and $3 and sell above $4. There’s little justification for a Price/Fee ratio above 2 when peers remain in lower ranges, though market euphoria could push prices higher temporarily.

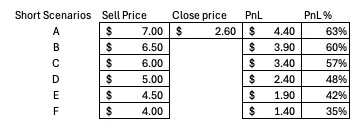

Since MET will have a high float and significant value in airdrop at launch, demand may appear strong at first but could quickly lead to heavy selling. Prices above $5 to $6 would present a strong shorting opportunity, targeting an average price near $2.6 or lower. Liquidity for buying above $2 is likely to fade quickly.

If the market reacts strongly, as seen with Plasma, the price could spike and then drop sharply to around $1.5 or even $1.3. If fee generation weakens post-launch, fundamentals will decline, possibly pushing the price below $1 — giving Meteora a lower FDV than Raydium.

Overall, I’m optimistic about the TGE. With liquidity starting from $0.5, early buyers have a high probability of strong returns. Even after paying the maximum 50% trading fee, early entries could remain highly profitable. Bots will likely act fast, so timing will be critical to capture the opportunity.

Thanks,

Joao

I was factually wrong about MET. The market ultimately priced it between $0.45 and $0.55.

My biggest mistake was focusing on fees. It is now clear that the market does not care about fees. The market only cares about revenue.

MET's revenue was significantly low, which is what brought its P/S multiple down to the sector's average range.