SpaceX dumped Korean market.

23 June opinions.

The headline today is SpaceX dumped the Korean market. SPCX fell -16% from yesterday in a heavy sell and deleveraging event, dropping from the $176 area to the $150s. That directional pressure, in a large liquidation event, pushed the derivative to its lowest price since the perp was created on Hyperliquid. The SpaceX IPO is a major signal for how the stock market performs at the current stage we are in, and the first pump-to-dump below the IPO price could point to a renewed fear environment. That is not a positive sign for the next major IPOs coming to market, Anthropic and OpenAI in particular, and not a positive read for sentiment, at least in the short term, with SpaceX the worst individual performer on my watchlist here. It signals a rotation to fear: every Asian space company dumped following SPCX’s last three days, and not only space names, the KOSPI index is down almost 10% on the day.

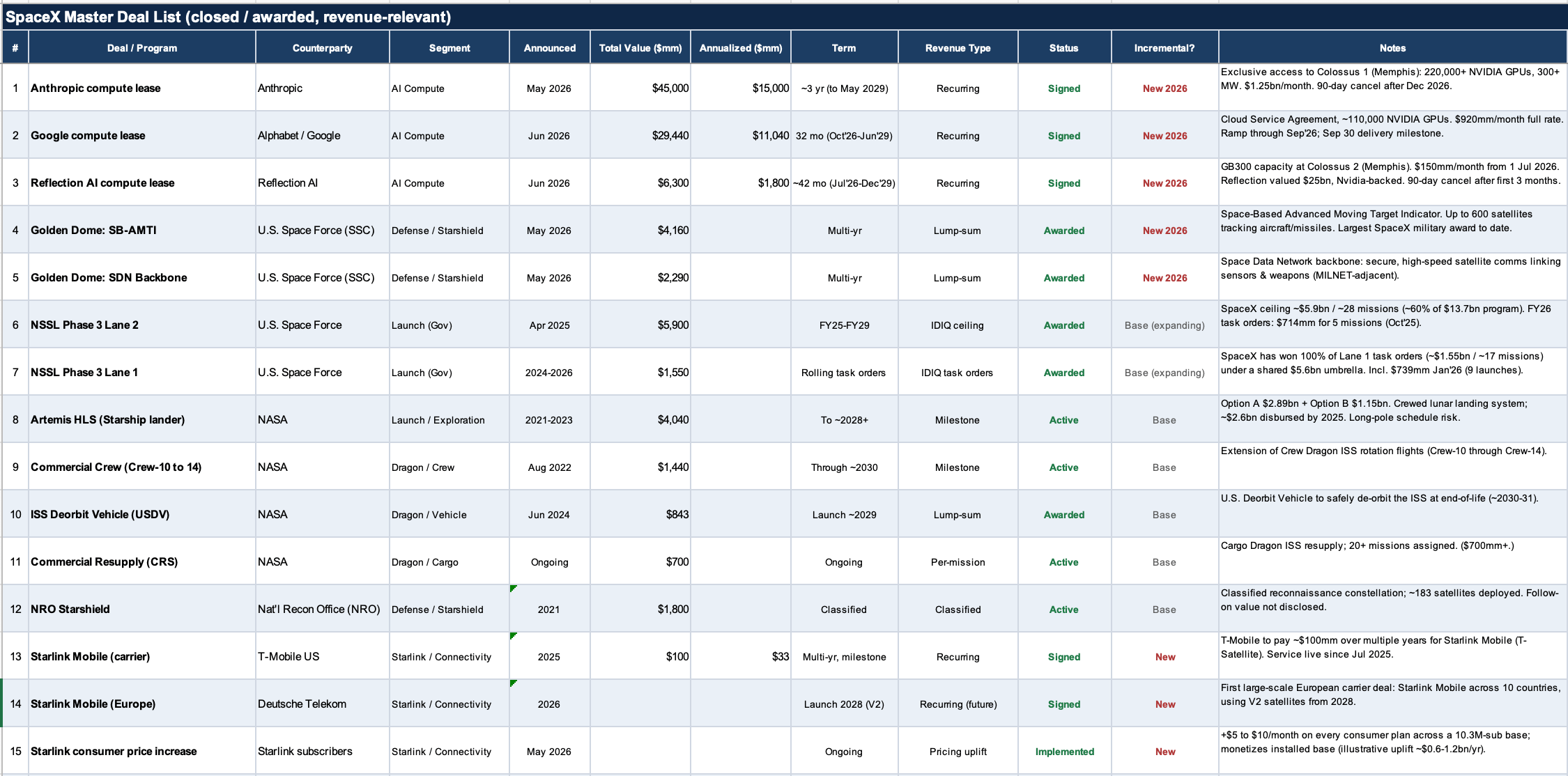

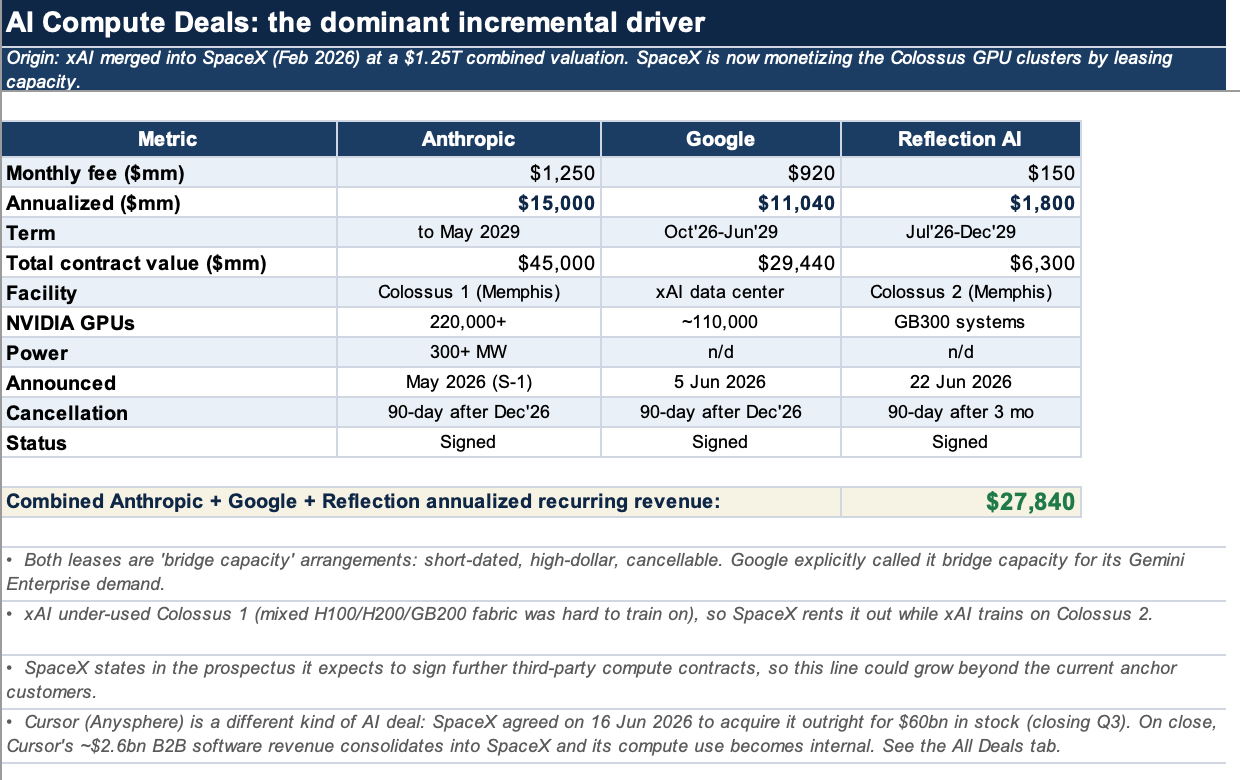

SpaceX is dumping on technicals, not on fundamentals. They closed another $6.3b in compute capacity for Reflection AI from the Colossus 2 cluster, a $150m monthly deal starting in July 2026, and deal after deal keeps closing on compute. Before Reflection AI, SpaceX closed a compute deal with Anthropic worth over $45b, bringing $15b in annualized revenue, and a compute-leasing deal with Google of almost $30b, bringing $11b annualized. SpaceX also acquired Cursor for $60b (after a $10b deal), so that one is irrelevant here. We are counting almost $30b in annualized revenue from compute deals alone, and after the IPO numbers these points toward a potential of over $100b in revenue by year-end. At a $2T market cap that is a forward P/S of 20, well below the hundreds P/S SPCX carried on its IPO date. SPCX took pressure from deleveraging de facto, but also from the debt opened on that date, with projected cash burn of over $400b through 2031. A lot more revenue must be created to reach the point where they can fund an eventual $100b in annualized cash burn and build the ambitious products they are projecting. Here I have only counted the almost $30b from providing compute to partners, but there are more revenue streams: Starlink telecom products, plus rocket launch and space exploration, sovereign award deals and NASA partnerships, which I expect to accelerate from here, with the number of SpaceX rockets sent to explore particular areas in space, the Moon especially, rising rapidly from 2026 to 2027 at higher pace.

Technology reads

On one side we have SpaceX vaporizing over $600b in market value in a day, with SpaceX and the hyperscalers absorbing severe selling pressure, while memory and energy is performing. Micron closed an Anthropic deal: a multi-year HBM, DRAM and SSD supply pact, a joint chip co-design agreement, a Series H equity investment, and an internal Claude deployment, all rolled into one announcement. These moves are about grabbing as much memory as possible. Anthropic is reaching a level of partnership that lets it scale and operate in a supply-constrained market.

There is memory, and there is power: two important gaps that the consumer-facing AI platforms like Anthropic need to fill. Microsoft signed a 20-year, 2.67GW natural-gas power purchase agreement with Chevron for “Project Kilby” in West Texas.

There is a natural force in high equity markets for companies to issue debt against equity: when equity prices are high enough, their credit rates stay very safe. Nvidia is raising $25b in debt against $85b in demand (3.4x oversubscribed). SpaceX opened a $20b inaugural investment-grade bond sale (BBB-rated by S&P, Moody’s and Fitch), right before the -16% single-day stock decline. That bond disclosed cash burn projected through 2029 and $400b in projected net debt by 2031. This rush for debt is what can hurt capital markets and could pressure an equity rebalancing. That is the one concern I have about the bull run continuing in a straight line up: the rebalancing of debt. Debt is tied to the Fed rate level, so as hiking pressure rises it directly pressures every high-debt company and forces a debt rebalancing across many players. These companies become less attractive when interest costs rise and they lag as revenue producers.

There is another area drawing more eyes, as it reaches a level of maturity that could eventually create a positive impact on the markets: the first generation of quantum innovation driving a new computational revolution, led by security and infrastructure security. In a World War III scenario, this is probably about decrypting the encrypted messages of other nations, so the rush to the new “atomic bomb” is generationally important for the few players working on government-led projects, security projects, or financial and blockchain areas. Creating quantum-risk-free security is a new level for financial infrastructure. The Trump presidency knows this, and the people around him are capable enough to have the government sign two executive orders on quantum computing: a 2028 deadline for a research-relevant quantum computer, a 2030/31 federal post-quantum cryptography migration mandate, and $2b in funding for named quantum firms. Government pressure pushing federal agencies to migrate is an important move and will propagate into enterprise security spending cycles. In security, quantum-risk-free companies will provide a catalyst over the next 12 to 18 months: a revenue increase from signed enterprise deals, especially for financial institutions, where the real quantum threat sits.