Technology shifts disrupt employment

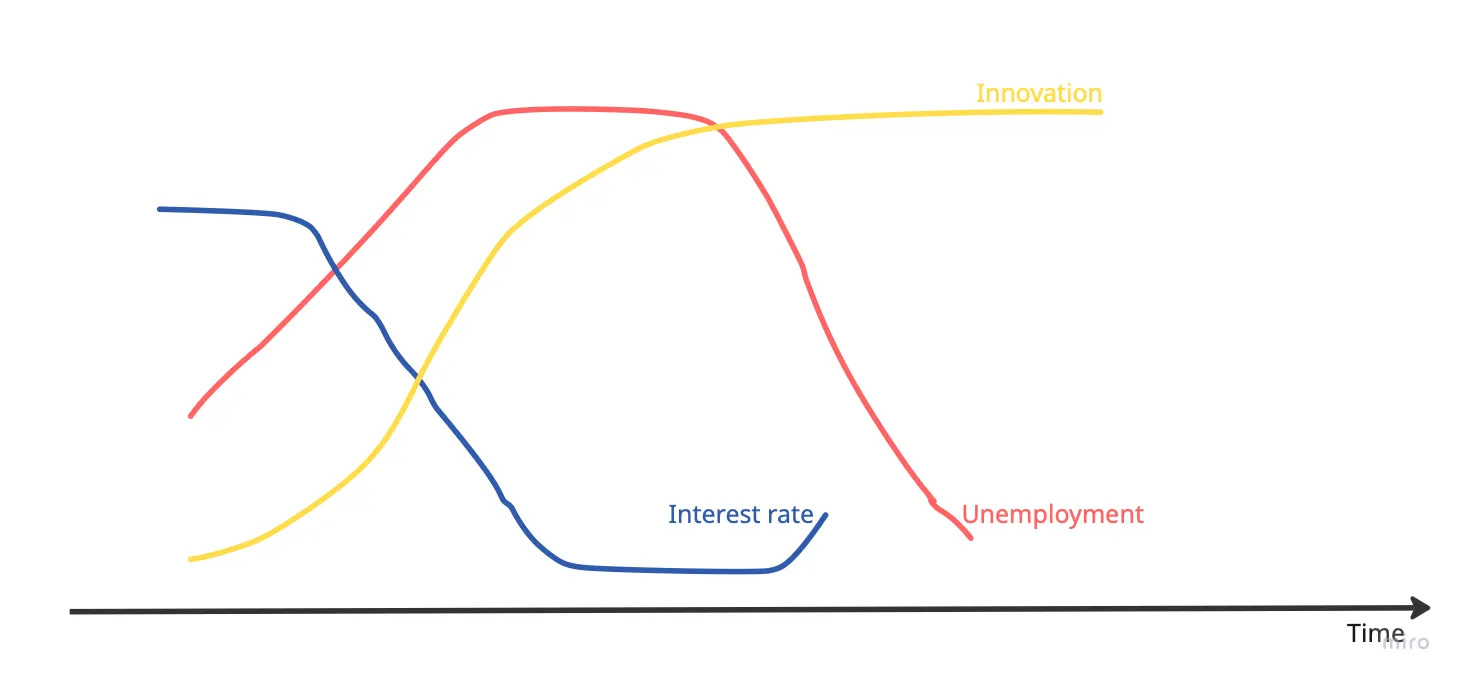

Shaping a flat circle in Innovation cycle

Thank you for dedicating your time to read this article. In a busy world, your attention is valuable. For any useful or thought-provoking conversations, I’m your guy!

When a mature technology cycle is disrupted, a new innovation takes its place. This event changes both the tech stack and the labor market.

Many observers note that new innovations create new, often better, jobs. This pushes employees to shift roles. It happened during industrialization and the technology boom. Humans moved from farms to city factories, and later to office chairs connected by the internet. This pattern is factually true, but the transition is not immediate. It takes time. Employers must first build expertise and the infrastructure required to train others on the new technology. It also takes time for employers to feel the need to expand their teams. Meanwhile, the innovators themselves are still discovering the technology’s full potential.

Eventually, a big shift occurs. New, innovative companies emerge. They fight for market share by doing the same or better work with far fewer resources. This forces established companies to replace their existing workforce. We saw this in the 1920 industrial revolution and the 1990 technology boom. We are seeing it again in the 2025 AI boom, as new companies achieve more with less. Technology consistently helps companies increase their margins.

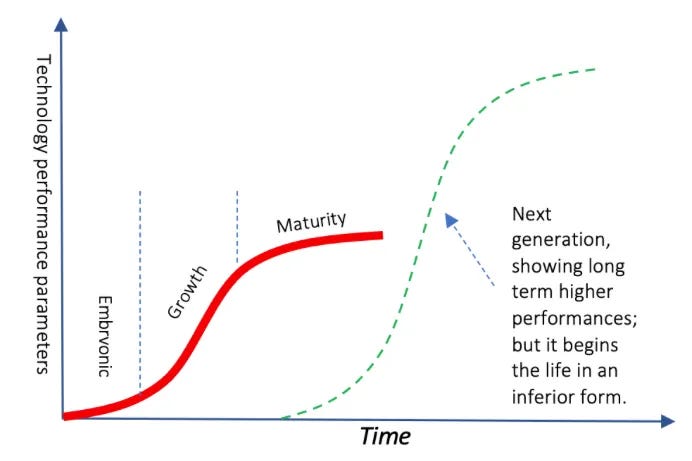

Each innovation cycle changes the established tech order. A new wave of companies forms. The internet, for example, has now reached maturity. It has lost the exponential growth curve it held for 35 years.

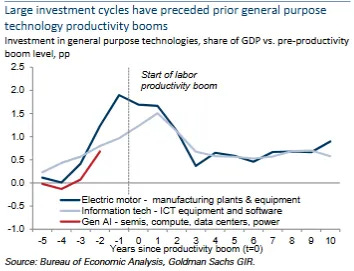

This maturity creates the necessary conditions for the next innovation to emerge. A new technological innovation is emerging. It could be robotics, generative AI, blockchain, or something else entirely. The goal of this analysis is not to predict the next specific innovation. Instead, it is to evaluate what happens to the labor market during such a cyclical shift.

We will study two important periods: the 1920s industrial revolution and the 1990s internet boom. These two eras reveal historical patterns that highlight what will likely happen next in the labor market.

Humans tend to overestimate the short term and underestimate the long term. We often think the innovation is already here, that insiders are ready to teach, and that newcomers are ready to learn. In reality, it takes longer than people expect for the population to adapt. It also takes time for companies to feel the productivity boost that builds confidence and leads to more hiring.

The end of an old innovation cycle is often marked by a final positive market phase. This phase onboards the last possible adopters. Sentiment then shifts from technological optimism to pessimism. This peak usually coincides with an easy-money environment and fast hiring. Soon after, the growth of job openings drops, and unemployment eventually follows. During this transition period, employment suffers. This lasts until the productivity from the new wave of innovation reaches scale. Initially, new technologies employ only technical experts and early adopters. These individuals are valuable, limited, and expensive to hire.

The 1990 period

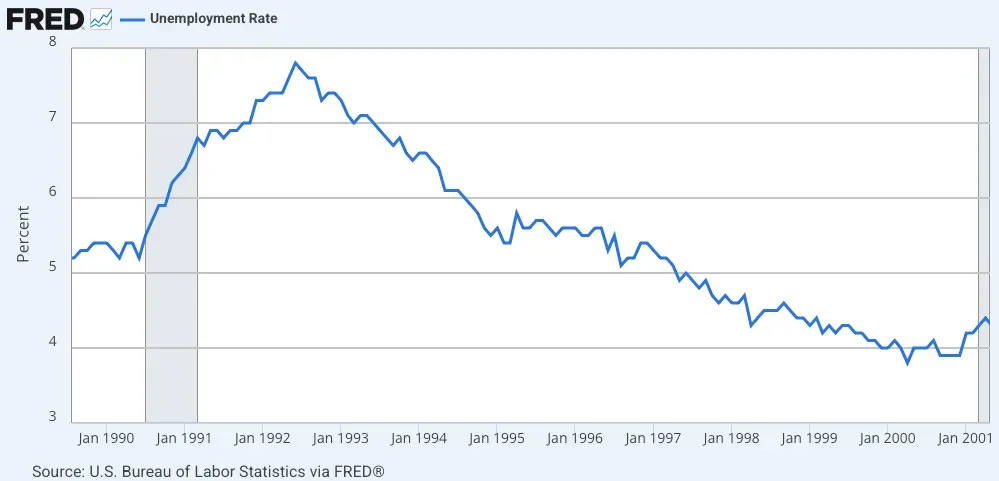

Looking back to 1990, only a small group of early adopters-the “nerds”-built the new internet technology. It took years for it to reach the general public and force traditional industries to adapt. During that time, the economy experienced bubbles, unemployment spikes, and gaps between tech hubs and low-tech regions. Unemployment rose from 5.4% in 1990 to 7.8% in 1992, before falling to 4% by 2000.

The Federal Reserve (Fed), mandated to protect the labor market and inflation, is forced to react to rising unemployment. It typically cuts rates aggressively. This gives employers easier access to capital and increases hiring speed. The Fed effectively signals a green light to the system, turning sentiment and increasing the money supply. From 1990 to 1993, the Fed cut interest rates from 9% to 3%. This facilitated the new innovation’s rapid growth.

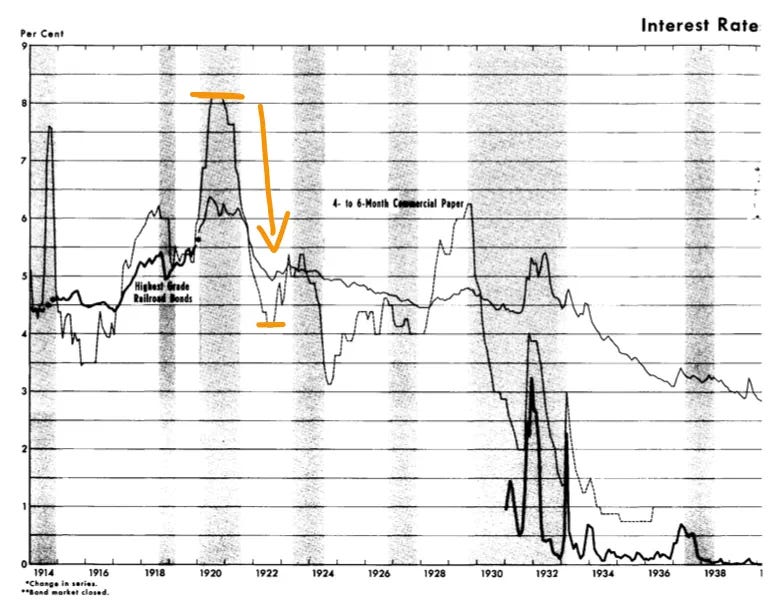

The 1920 period

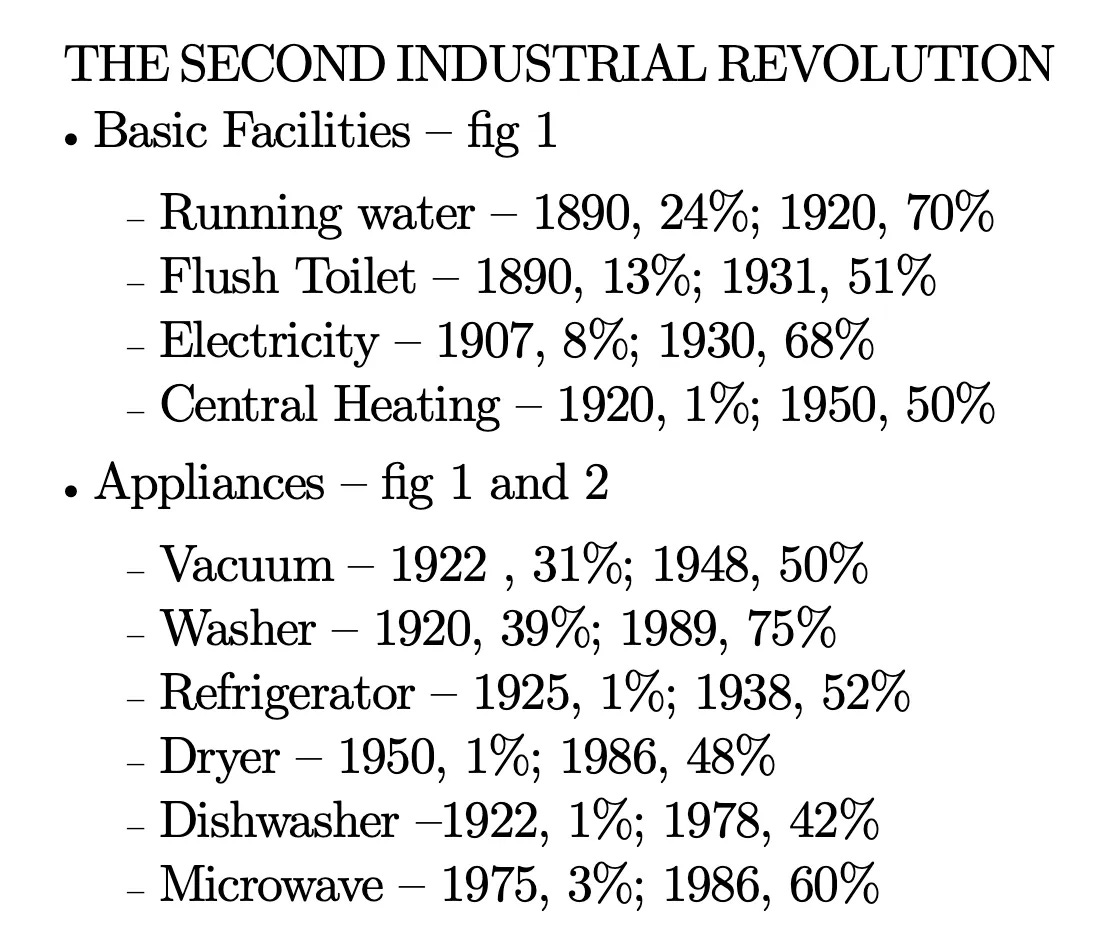

A similar playbook unfolded in 1920. After World War I, a transformative new cycle began: the industrial revolution. This period transformed modern history with many new innovations. However, the labor market first suffered a decline driven by this economic shift. This pain occurred before the innovations had a positive effect on jobs-before Henry Ford employed thousands and before refrigerators, washing machines, and vacuum cleaners were produced at scale and widely adopted by the population.

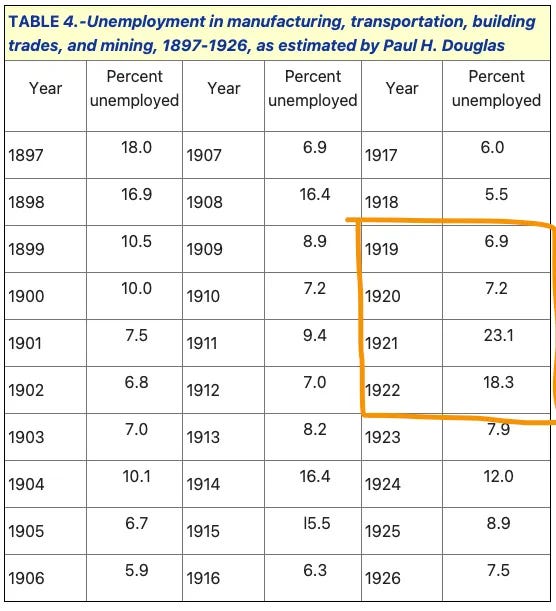

Unemployment grew sharply from 6.9% to 23.1% in 1921, a clear sign of the innovation shift. It eventually declined to 7.5% by 1926.

This growth in unemployment forced interest rates down. Rates dropped from 8.13% in 1920 to 4.13% in 1922 to support the labor market.

The 2025 period

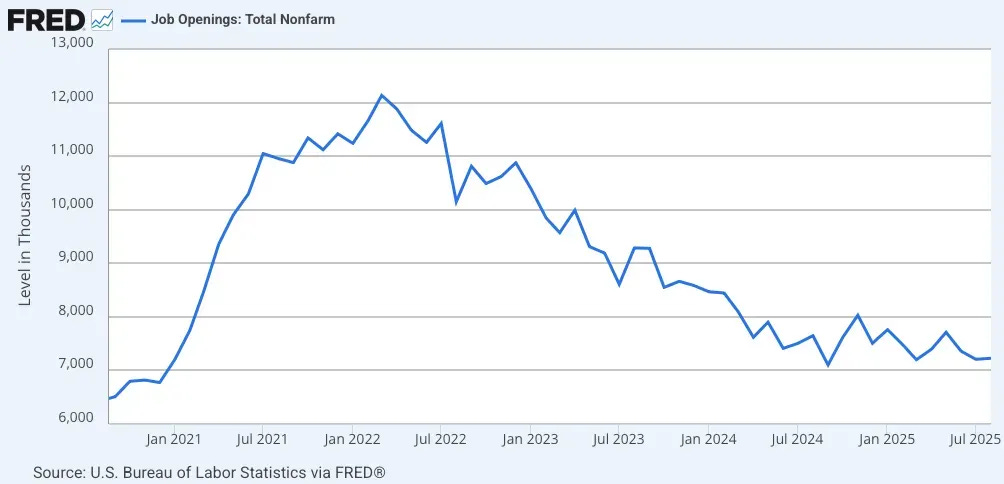

A similar pattern occurred in both the 1920 and 1990 innovation shifts. Today, we have more data to track these cycles. As Ray Dalio famously says “Hiring is one of the last things to turn down at the end of the expansion, but the rate of job openings is one of the first things to decline.” Ignoring the massive capital injection from 2020 to 2022 following the COVID pandemic, job openings began to fall after 2022. Employers grew cautious and slowed hiring. As Dalio noted, job openings are a leading negative indicator.

That decline in openings has since appeared in rising unemployment, which has been climbing since 2023. Unemployment rose from 3.6% in 2023 to 4.3% today, and it is trending higher. We are in an innovation cycle shift, and the labor market is already showing signs of stress. It will likely suffer more. Recent news points to significant layoffs from large companies. Meta plans to fire 600 people in its AI unit, and Amazon aims to replace 600,000 workers with humanoids. This is just the small peak of a much larger unemployment iceberg.

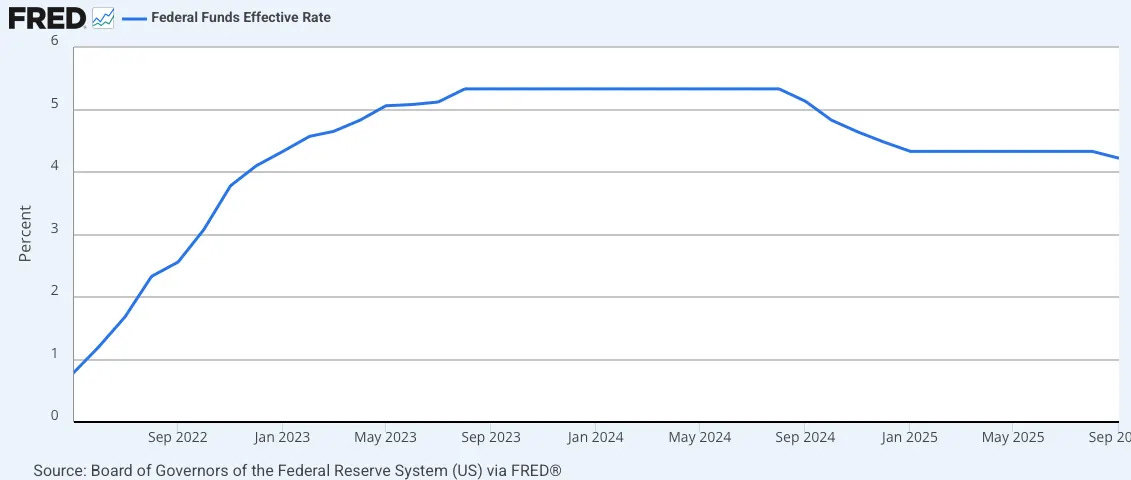

Fed Chair Jerome Powell has already shifted his policy focus, moving from inflation to the labor market. Despite unemployment remaining relatively low, the Fed has already taken action by lowering interest rates. It will be forced to cut further as the labor market weakens. In September, the committee stated, “Job gains have slowed, and the unemployment rate has edged up but remains low... The committee judges that downside risks to employment have risen.” This points directly to higher labor market risks. The Fed has already dropped the effective rate from 5.33% in 2024 to 4.22% today. Further cuts will come to solve the labor market issue.

This article shows a consistent pattern during innovation cycle shifts: unemployment increases early, before the new productivity boost takes effect. This is followed by a reaction-lower interest rates-to improve economic conditions.

We are living in a flat circle, and it is happening again.

Thanks,

Joao