The Iran-war isn’t over, but is it almost there? My war framework

18 March 26'

[Brief in audio format]

We have all heard Trump and his administration announce that the war is almost done. Yet, we see massive swings in OIL prices, dominated by further headlines and strike threats from both sides.

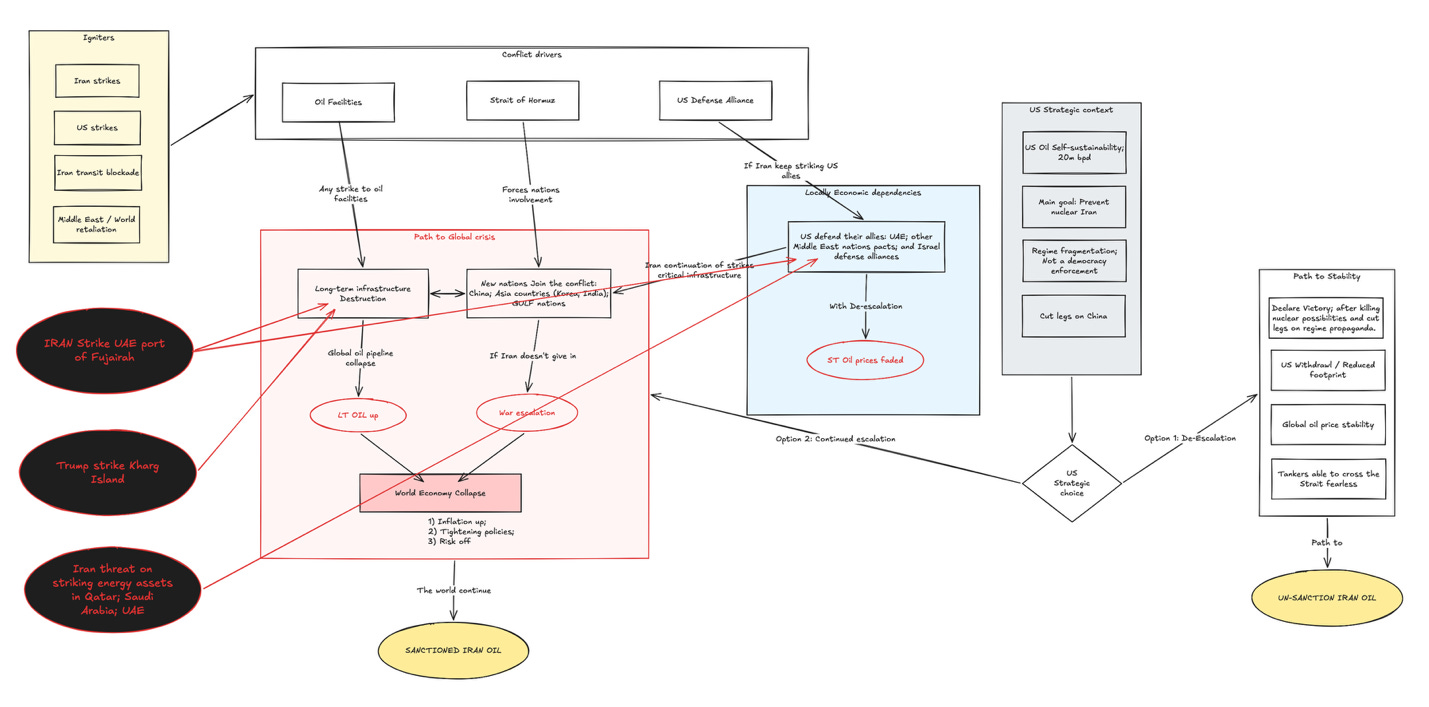

Trump threatened to strike oil infrastructure on Kharg Island—after already striking Iranian military assets there—as a warning signal that if Iran doesn’t open the Strait, the US will strike critical oil. Any destruction of this infrastructure would take years to rebuild, leaving the country deprived of its most critical source of revenue. Kharg Island produces 90% of total Iranian oil, meaning any destruction here will have massive consequences.

Iran, on the other hand, threatens to escalate by attacking Qatar, Saudi Arabia, and UAE energy infrastructure, having already struck the UAE port of Fujairah on Monday. Their justification is always that “US military forces are present and hiding among civilian facilities.” Iran consistently highlights that they aim to attack the US, not their Middle Eastern neighbors. In practice, however, these neighboring nations are the ones under attack. Today, Iran threatened to strike energy assets in Qatar, Saudi Arabia, and the UAE, emphasizing that these are “legitimate targets” following the Israeli strike on the massive South Pars gas field and the assassination of Iranian security chief Ali Larijani.

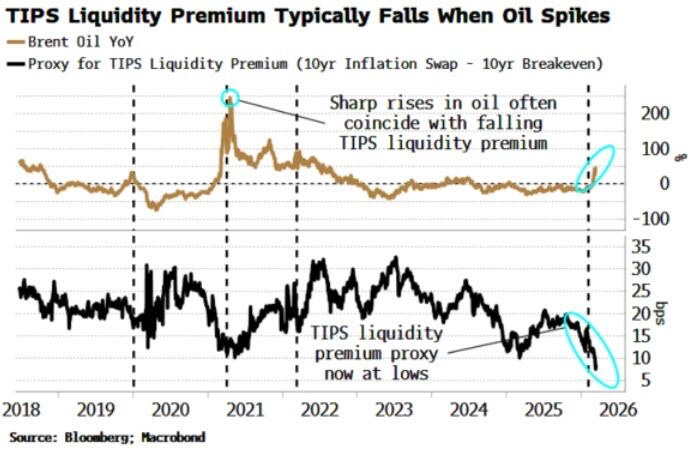

These instabilities pressure oil prices to fluctuate aggressively. Even knowing that the long-term directional trend for OIL price is down, the short-term and near-term direction remains highly uncertain.

We are already seeing the macroeconomic effects of this uncertainty. Today, PPI MoM came in above expectations. While the forecast expected a value below the previous number, it came in well above the prior reading: 0.7% compared to the 0.3% forecast and 0.5% prior. These are the first tangible signs of the impact of rising oil prices.

This aggressive deviation dumped today’s market on the open. The market is in fear, but it is within these pendulum swings that we find the best bargains.

This remains true even when long-term investors are ignoring this war, and despite oil shocks impacting long-term inflation while TIPS premiums sit at historical lows.

It was exactly on this playbook that we traded KOSPI. In previous letters, we correctly picked the bottom on KOSPI; as the war fades over time, KOSPI will aggressively V-shape recover. I still agree with this trade. Even though I am aware tomorrow’s reaction could be volatile (down), any swing will flush out a bunch of leveraged exposure and create aggressive dips—beautiful dips to buy. KOSPI is up +17% from the bottom and only down -6.6% from the highs. It is certainly a great market to watch.

Paired with this market, we have the UAE, which is being penalized by this conflict. In particular, real estate assets are taking a hit. Take EMAAR, the biggest tradable stock that captures the majority of Dubai’s real estate performance. It is down aggressively, even though we all know Dubai has been the most euphoric real estate market of the past five years, with impressive momentum attracting an influx of buyers. EMAAR is currently down -38% from the highs, experiencing its highest drawdown since the COVID shock in 2020.

Despite this drawdown, the sentiment on the ground remains very optimistic. People believe the government is able to protect them. However, those who have a second home are now leaving; flights to or through Dubai are being canceled, and the population has reduced significantly.

For Dubai to actually lose its moat, I believe something much bigger has to happen. People continue blaming the US and Trump for this Iranian escalation, and with the UAE staying out of the war, the sense of protection remains intact. In fact, post-war, with a more stable Middle East and a stable Iran offering better protection, there is a scenario where the region ends up stronger than it was pre-war. This could leave Dubai growing faster and more resilient than ever before. Their land is not being aggressively threatened, and as long as it stays this way, I don’t see a long-term problem. Markets are reacting like a pendulum, and this dip is a massive bargain.

The War Framework

However, my goal in this letter is not simply to talk about previous trades or untrades. It is to provide a clear framework—one that I will later detail in a standalone post—on how to navigate the war. This framework gives us clarity when we receive alerts about Iran headlines, showing us how to manage exposure to predictable black swans and how to read the news efficiently.

Here is the framework I believe in and have been using to judge headlines and their impact on open markets.

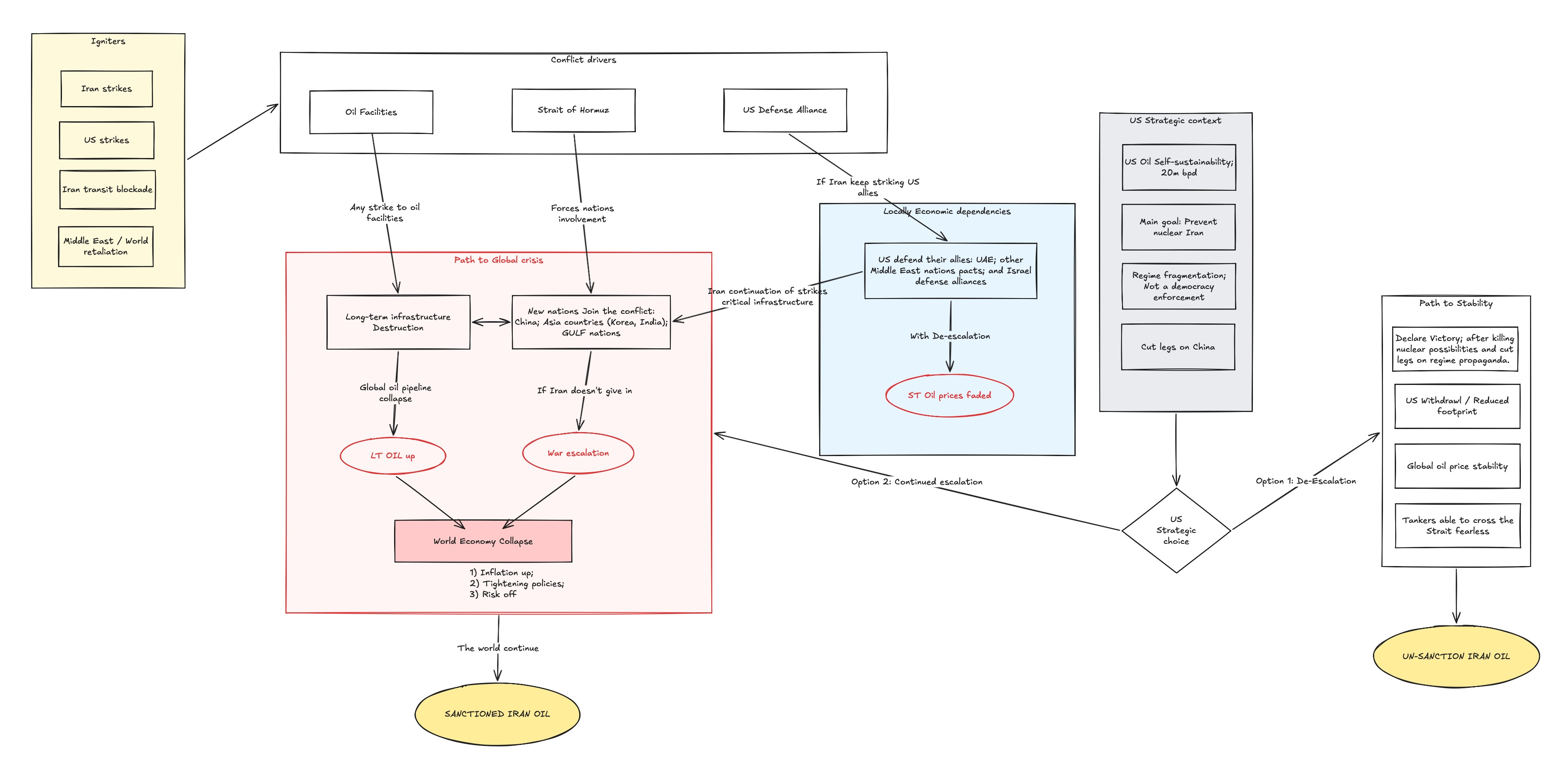

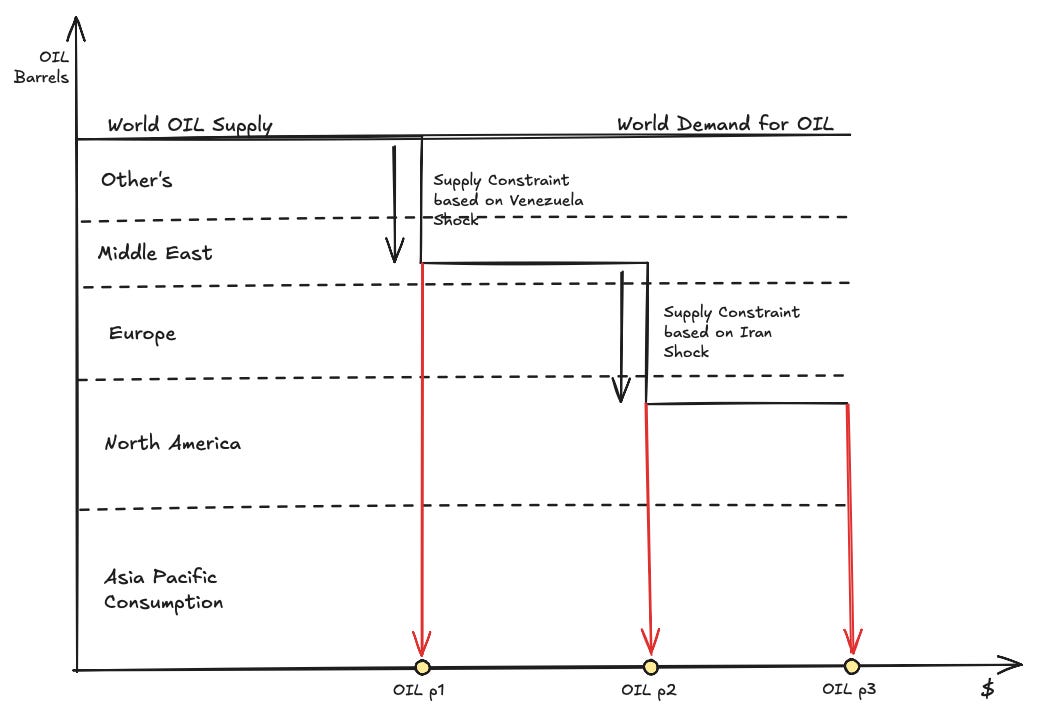

There are three major conflict drivers that sustain this war at the top level. These are the underlying principles for every military action in this conflict: Oil/Energy facilities, the Strait of Hormuz chokepoint, and US defense alliances. Based on these three drivers, each nation acts to escalate or de-escalate the war. Every action eventually ties back to one of these three critical pillars, and each headline is directly related to them as well.

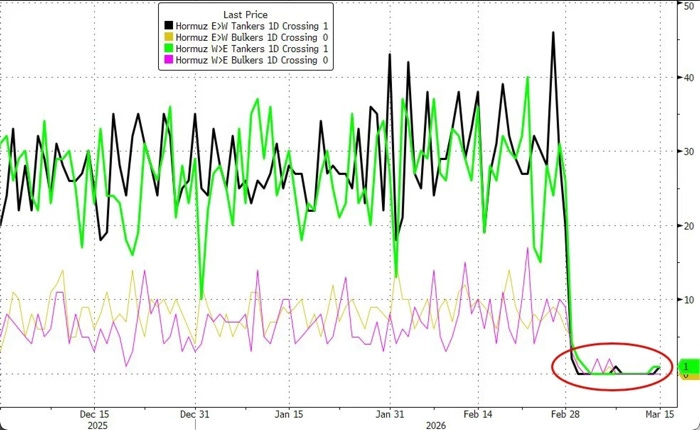

These three major drivers do not carry the same global weight. Some create localized problems where further decisions are required to escalate things, while others have direct, aggressive, and highly robust consequences. The most critical and sensitive areas are related to oil facilities—where any destruction could lead to a long-term supply constraint requiring years to rebuild—and the Strait of Hormuz. The Strait sustains all of the Asia Pacific; without it functioning, all Asian and Gulf nations are smoked and will be forced to get involved, drastically escalating the war.

The less globally destructive, but highly decision-driven escalation path involves US defense alliances. These pacts force the US to defend Gulf nations, Israel, and other allies, dragging them into the conflict even if they don’t want to be. If Iran strikes US allies, the US will show its power by protecting them and fighting back. We live in a US-Empire world, and they have to protect that empire by defending their alliances and projecting strength. However, as Ray Dalio highlights, this is also the fastest way for nations to “go broke.” An increase in military and defense budgets leads to an increase in debt, making nations less financially sustainable and riskier in the credit cycle (this is the core thesis on why BTC and GOLD are strong long-term assets to hold).

By taking a deep look at this framework and applying the latest headlines to it, we can predict further black swans if the escalation continues. Are we walking a tightrope.

Current headlines are impacting critical areas that could, with significant probability, end up damaging oil market dynamics. These threats will consequently add a risk premium to every barrel that has to cross the Strait in the future (HSBC analyst warned), making oil more expensive due to post-war insurance premiums on carriers. The US can actually be a beneficiary here. Their Texas oil (WTI) doesn’t cross the Strait, meaning it will carry a lower risk premium and become even cheaper than BRENT post-war. WTI could trade at a higher discount compared to pre-war levels, and we are already seeing signs of this.

Ultimately, each decision to escalate or de-escalate the war has direct consequences on the supply and demand of OIL. This is the main reason why oil is fluctuating so much, driven by algorithms pricing in these micro-market dynamics.

The latest shocks are fundamentally about the quantity of oil available to be bought. When we talk about sanctioned oil, still affecting global oil price. Europe and North America weren’t buying oil from Iran, but Asia was. If Asian nations are no longer able to buy from Iran, that demand has to go somewhere else. They will pressure the market and compete to buy at higher prices from other providers.

Russia is a clear winner here, Russia wants the war to keep going, that’s why they are helping Iran. Because they have a lot of oil to extract and sell, the world will be forced to buy from them, even though they are a sanctioned nation. We have already the first signs of this possibility, G7 start buying oil that was already on the water, but soon we will be buying oil directly from Russian soil. If we don’t, we will simply push oil prices higher for all, and/or China and other Asian nations will buy it instead.

Two key highlights emerge from this dynamic: the supply and demand for oil are relatively inelastic. You can’t change the amount of oil on the market overnight, even if higher prices create strong incentives to refine and open new markets. Similarly, demand won’t drop overnight, as households, transportation, and industries must continue operating daily. We have to view these events through the lens of world supply and demand, where the majority of ships are currently on the water, trading and changing directions frequently.

In a world where Asian consumption was being absorbed by Iranian oil, the loss of the Strait or the Iranian market represents a massive shock. This consumption is no longer being absorbed, shocking global markets by forcing a massive buyer to aggressively compete for available oil.

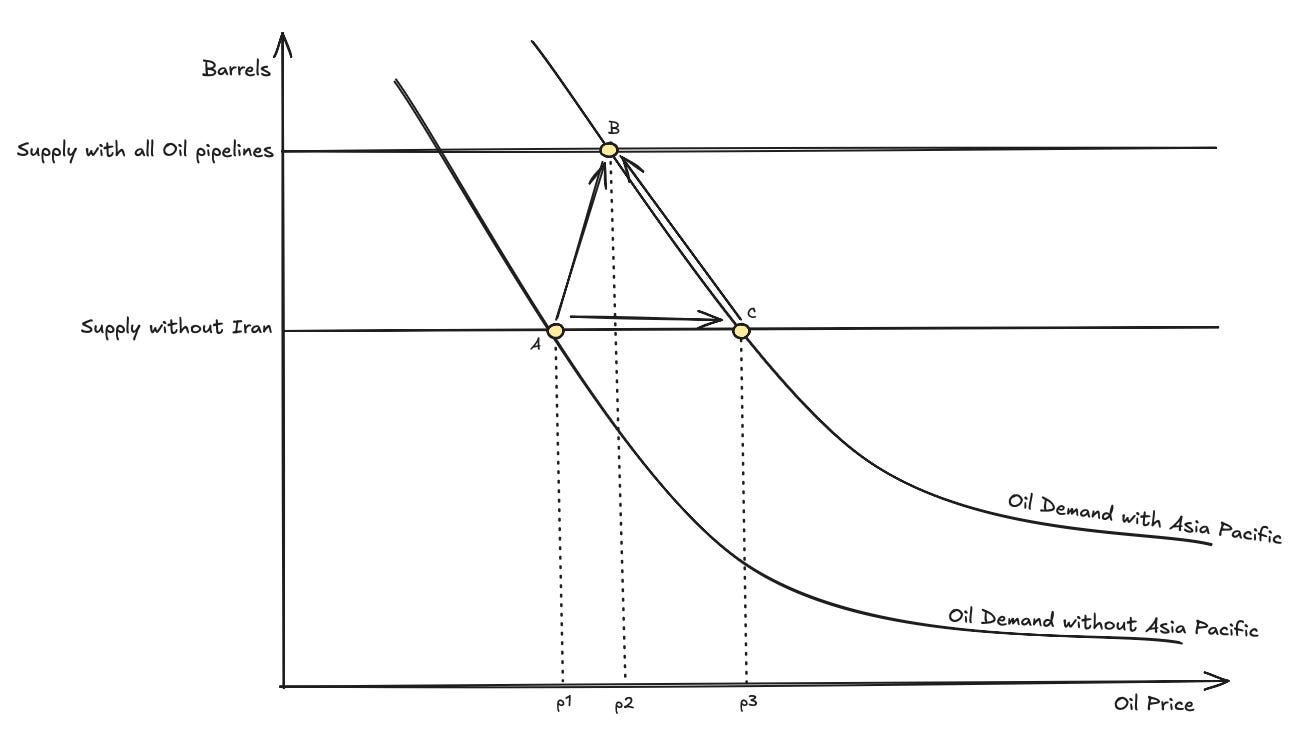

Without Iran, oil prices will increase for a long period until the rest of the world can bring new refineries online. Any strike from US to Iran oil infrastructure will have this massive impact.

The exact slope of the curves here is irrelevant; as long as the marginal consumption from Asia is higher than the marginal supply from Iran, we are directionally right. This being said, in a post-war scenario with clean, unsanctioned Iranian oil, we will probably end up with a higher equilibrium oil price. This dynamic is enforced by pushing Iranian oil supply into the open market, and adding a massive buyer (Asia) that shows its purchasing power. This pushes the price higher for the rest of the world, but especially for Asia, which previously bought sanctioned Iranian oil at huge discounts.

Following this logic, it is predictable that oil prices will spike as we eliminate Iranian supply. But as soon as the situation is resolved and Iranian oil is ‘clean,’ prices will drop from their shock peaks—though they will remain higher than previous baseline levels. As a result, miners in the US, Europe, and Africa will generate more revenue than in pre-war scenarios, based on these elevated prices.

If Iranian oil remains sanctioned post-war, we will likely see marginal upward pressure on prices from Asia as they are forced into buyer diversification. But still settle lower compared to if the entire market opens up and trades freely. For now, Asia will likely keep benefiting from discounted Iranian oil, choosing to deal with any geopolitical blowback later on.

Building on this recent volatility, there will be intense pressure to increase global strategic stockpiling. Nations will be forced to hold greater quantities of OIL to buffer against any future supply shocks. Consequently, this preemptive hoarding will likely increase baseline demand for OIL, driving the natural equilibrium price higher.

This creates a very compelling thesis to watch oil miners carefully. As soon as the market starts pricing them down when oil prices begin to collapse, opportunities will arise. I expect that when oil prices start coming down, traders will short or sell their holdings in miners. However, higher demand for oil, and higher long-term oil price, and subsequent above expectation earnings results will create positive shocks and unlock the real value of holding these stocks. So far, they have performed quite well under these Iran-war scenarios.

This is intended to be a thought exercise, and not financial advice. Reach out in open conversations, DM me or comment anytime.

I’m aiming to provide clarity about the world day-by-day, and I hope you get smarter and more financial intelligent every day. Each day we increase our chances of winning.

Thanks, Joao