The Worst day in Korea markets. Even worst than the day after 9/11

04 March 26'

[Brief in podcast format]

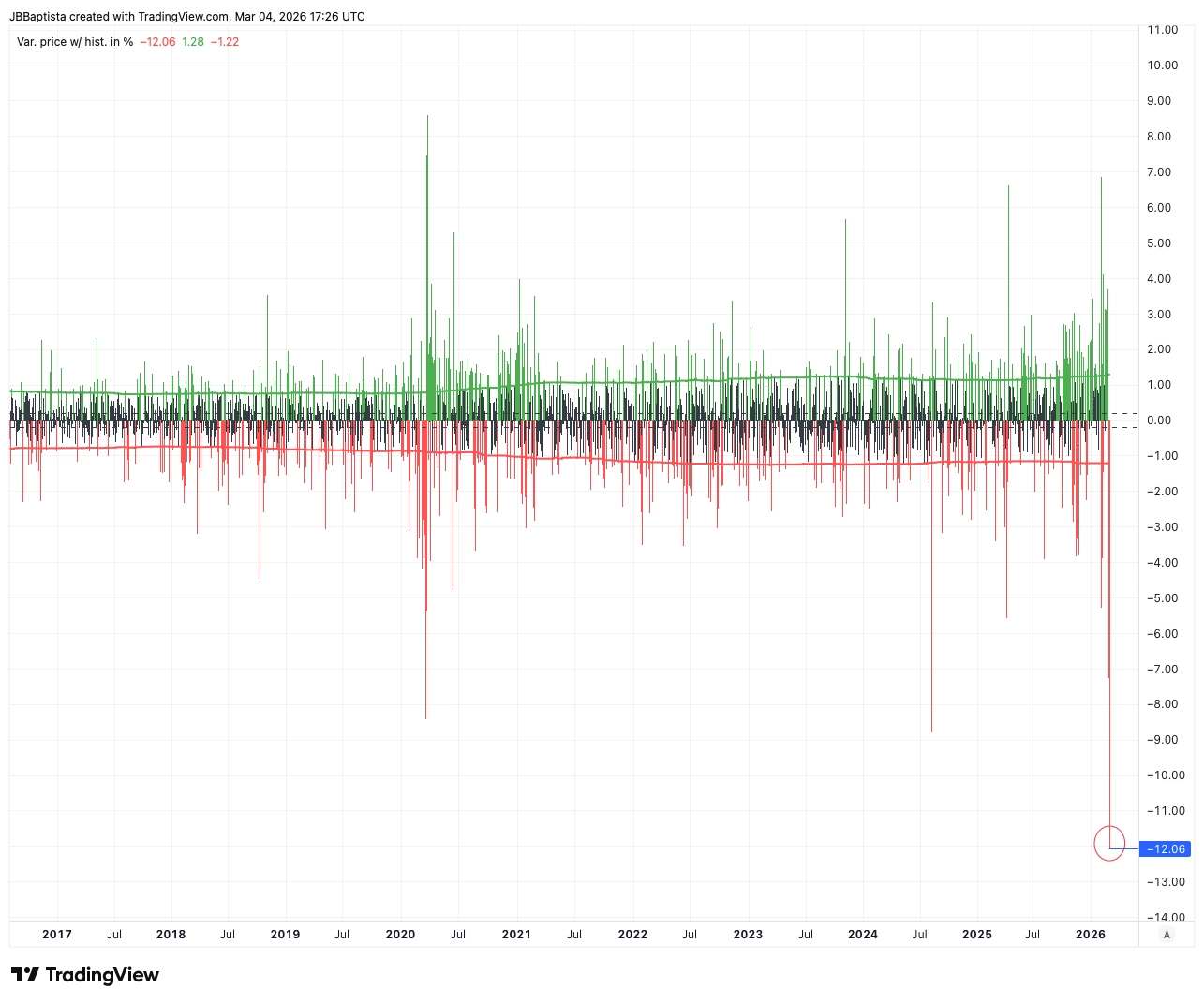

Today marks the worst day in the history of the KOSPI. With the index down -12.06% in a single day, we have entered uncharted territory. The only comparable precedent was September 12, 2001, when the KOSPI sank -12.02% in the immediate aftermath of the 9/11 attacks. On that day, Korean markets reacted aggressively as the first major exchange to open following the tragedy in the U.S. By eclipsing that record today, March 4, 2026, officially becomes the darkest day in the history of the Korean market.

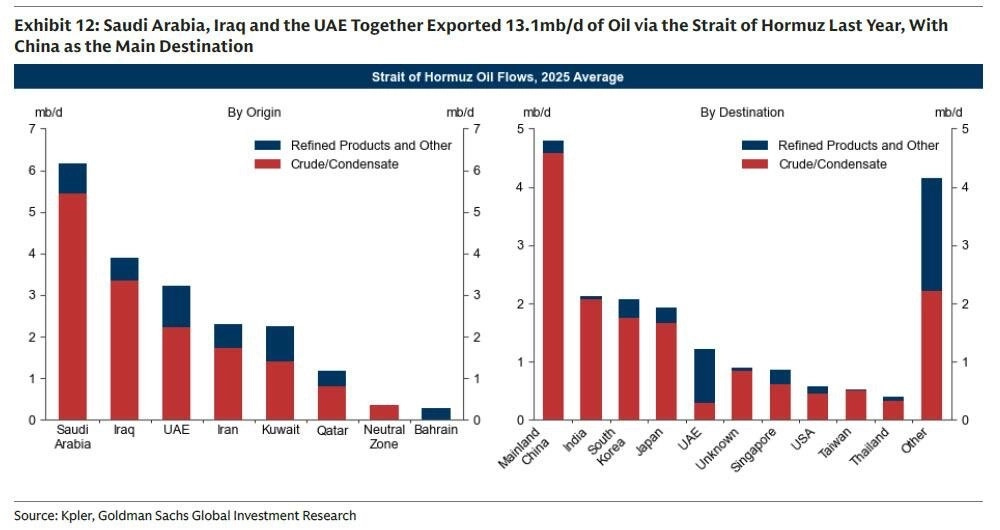

This collapse is driven by a singular, overwhelming headline: oil supply constraints FEAR. Korea’s dependency on crude passing through the Strait of Hormuz is absolute, with more than 70% of all imports relying on that narrow passage. With Iran now exerting control and threatening the Strait, the market has reacted with pure aggression to the headlines.

However, this volatility is not solely a consequence of geopolitical tension; it is also a byproduct of the market’s internal microstructure. As I highlighted in previous letters, the Korean market was already on an euphoric, over-extended path. This created a “predictable black swan” (as I like to call it) scenario where even a minor disruption could cause a total bust. The energy crisis and the closure of the Strait acted as the catalyst to dump the market and liquidate retail leverage. This “flush” has decimated the index and AI stocks alike under the threat of a prolonged crude shortage.

We must remember the euphoria of February to understand the scale of this reversal. The KOSPI was in the midst of aggressive bull momentum, boasting a 1-year performance of +118% and a YTD return of +30%, with equity flows at historical all-time highs.

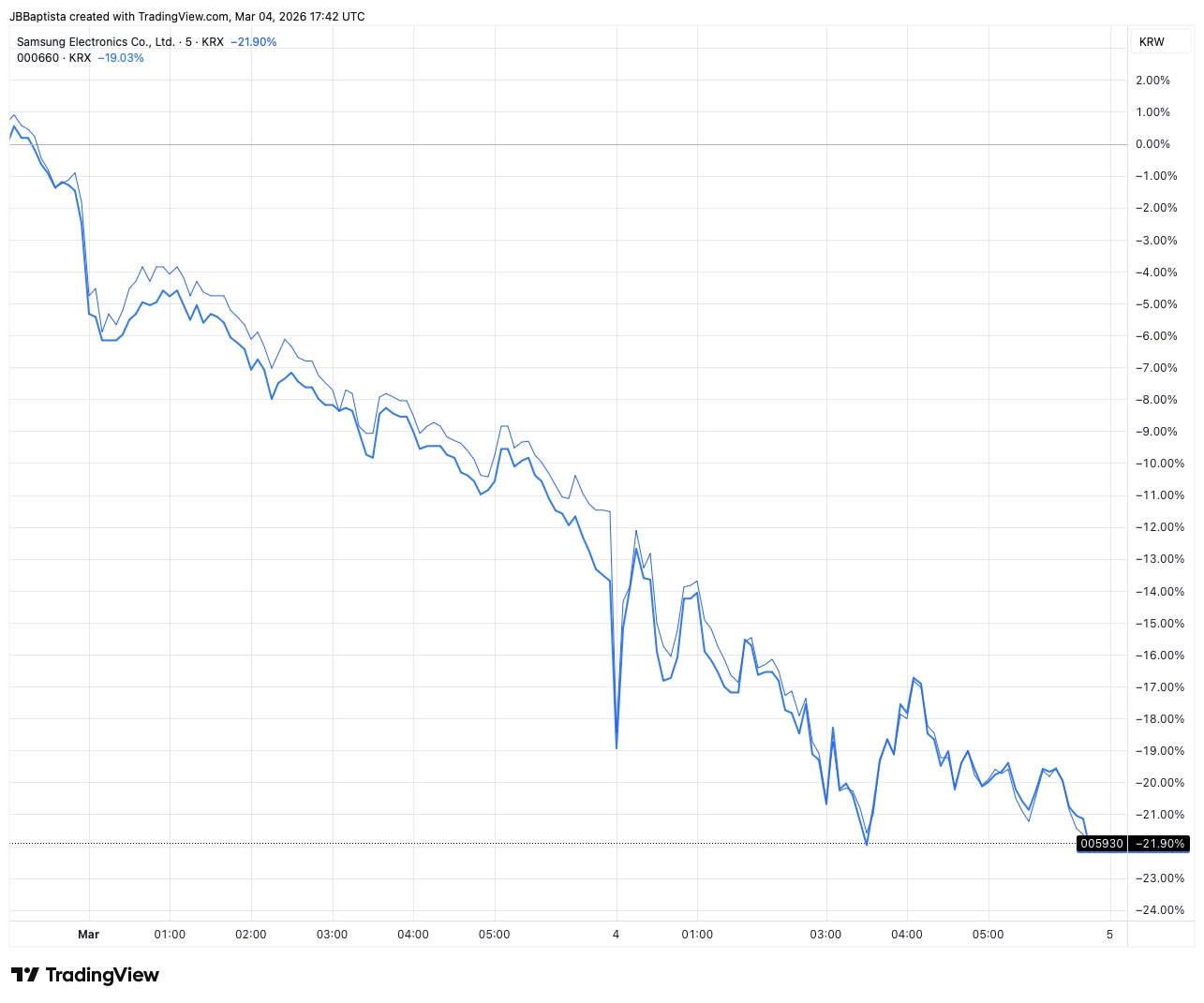

The majority of these flows were concentrated in two frontier AI companies: Samsung and SK Hynix. Since the conflict began, both have plummeted more than -21% in high correlation —confirming systemic risk.

Understanding this “house of cards” explains why the market is down, but it also suggests why we might see a V-shaped recovery. I suspect a rebound will trigger as soon as the Trump administration stabilizes the Strait of Hormuz conflict. Resolving the insurance issues for crude carriers and ensuring safe passage through the Gulf is now a matter of global urgency. Secretary Bessent has already signaled that the issue will be addressed over the weekend, and Trump has alerted the markets that ships will move.

This pressure is not coming from the West alone. The Chinese economy depends heavily on crude crossing the Strait. While I previously thought this could escalate U.S.-China tensions, I now believe that if China continues to let the Strait remain blocked, it will sink Asian economies while the West stabilizes and the U.S. dollar strengthens. China will likely be the first to pressure Iran to surrender, facilitating a deal with the U.S. to secure its own oil quotas. This convergence of interests—including Middle Eastern nations dependent on the security of their own land—will rapidly erode Iranian leverage.

While markets are currently reacting with massive short-term fear, the physical reality is more stable for three reasons:

The estimated travel time for a crude carrier from production to Korea is 30–45 days. 4-days shock causes no real economic problem.

Korea maintains one of the most robust strategic energy reserves in the world, with supply secured for several months. Not infinite but at least 7 months secure.

An immediate weakened KRW reaction relief right after, no currency depreciation momentum.

Nevertheless, there is a reason Squid Game resonates so deeply here; it reflects a realistic truth about the Korean appetite for speculation. Domestic traders love to push markets to the absolute limit. Those who remember the “Kimchi Premium” know that when Korean traders enter a market, they push speculation to its breaking point. For that reason, rather than buying the dip immediately, I am watching closely. After a 2025 rally bottom-to-peak of +175%, even a -12% daily correction can trigger a deeper liquidation cascade. I can easily see another -15% to -20% drawdown as retail investors wake up to another “flush” and exit to secure remaining profits.

My strategy is to set limit orders below $4,500. I am timing this based on the expectation that if the U.S. cannot immediately control the Strait, the fear will intensify—but the moment the Strait reopens, the V-shape reaction begins. The catalysts to follow are: 1) The reopening of the Strait (an immediate buy signal) and 2) Mean reversion at the point of maximum liquidation fear.

Korea is not the only market suffering under this geopolitical weight; the UAE is also down. There, the concern is that land-based tensions will damage the “wealth-haven” status and tourism that their economy relies on. While I am still researching the full repercussions, the UAE ETF has reached one of its highest single-day volumes—usually a sign of a mean reversion as liquidity is absorbed. I expect the UAE to be prudent, increasing defense to prevent escalation on their soil to protect their economic stability. But still uncertainty on the long-term consequences to their economy and stability —if Iran regime changes, it can be the epic moment for all middle east. Iran is the most problematic country in middle east. US controlling it, will give theoretical peace to the region.

Ultimately, the message from the administration, via Pete Hegseth, is clear: we are only four days into this conflict, but progress is being made. Pete and Trump highlighted the infinite supply of bombs available. This leads us to the biggest potential catalyst for Bitcoin. As Arthur Hayes mentioned in his last report, Middle Eastern wars have historically triggered the same reaction: massive stimulus to hedge economic weakness. The longer the U.S. engages in the costly activity of Iranian “nation-building,” the higher the likelihood the Fed increases the money supply to support the effort.

This “infinite glitch”—the ability to print money to finance the war machine—is the core of our thesis to go long Bitcoin. History bears this out:

1990 Gulf War: The FOMC eased policy to counter economic weakening.

2001 War on Terror: The Fed accelerated rate cuts to restore confidence, with Alan Greenspan delivering a 50-basis point cut.

2009 Afghanistan: Despite rates being at zero, QE was deployed to provide infinite liquidity.

I maintain my thesis. The war machine requires the printing press, and the printing press requires a hard-money hedge.

This is intended to be a thought exercise, and not financial advice. Reach out in open conversations, DM me or comment anytime.

I’m aiming to provide clarity about the world day-by-day, and I hope you get smarter and more financial intelligent every day. Each day we increase our chances of winning.

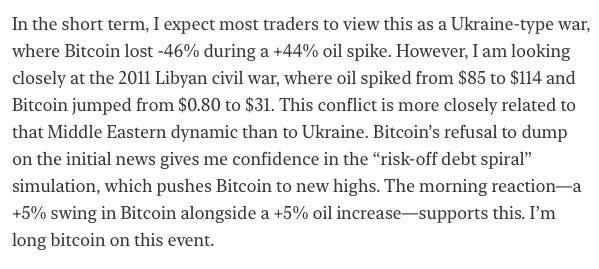

Thanks, Joao