TON: Building the Bull Case

And why TONX may be the asymmetric expression of it

A regime change, in three steps

Something fundamental shifted on TON in the last month, and most of the market is still pricing it as just another rally. It is not. In a four-week window, TON went from being a general-purpose, Telegram-adjacent L1 — a chain with a great narrative but always one step removed from execution — into something else entirely: a Telegram-controlled global payments rail with native AI agent infrastructure. That is a different asset.

There are three updates worth understanding, because they only make sense as a sequence:

Three catalysts in four weeks. The market is still digesting the third.

1. Sub-second finality (April 10)

TON activated the Catchain 2.0 consensus upgrade. Block times collapsed from roughly 2.5 seconds to 400 milliseconds, and final settlement now lands in about one second. That is the kind of latency where a payment on-chain feels like sending a message — and crucially, it is faster than a card-network authorization message, all delivered through cryptographic finality. TON is now in the same neighborhood as Solana on speed. The old narrative that TON had a finality flaw is done.

2. Fees cut 6x (April 24)

The next step came two weeks later. Transaction fees dropped roughly 6x, to around 0.00039 TON, or about $0.0005 per transaction. Two details matter more than the number itself: fees are now flat regardless of network load — no volatile gas auctions — and Durov has explicitly said most transactions will eventually move to a fully feeless model, subsidized at the protocol or Telegram-app layer for common payment flows.

Once you remove fee volatility, you remove the single biggest reason a consumer payment app cannot run on a public blockchain. That is the actual unlock here.

3. Telegram replaces the TON Foundation (May 5)

This is the one that changes the asset. Pavel Durov announced that Telegram itself will replace the TON Foundation as the driving force behind TON, and will become the chain’s largest validator. In his words, this is a “direct commitment to the chain’s security and direction.” TON is no longer a Telegram-adjacent project run by a community foundation; it is, effectively, Telegram’s chain.

In a feeless or near-feeless environment, validators normally take the loss on zero-fee transactions. Telegram becoming the largest validator is the answer to that — Telegram itself is willing to subsidize the cost of running a payments network for a billion people. That is the bet.

What TON actually is now

Stitching the three updates together, this is the description that fits:

TON is the settlement layer for Telegram’s billion-user app, with sub-second finality, near-zero fees, AI agent rails through Cocoon, and direct operational control by the company that distributes it.

Every piece of that sentence is now true at the same time, for the first time. Each piece individually has been promised before. The convergence is what is new.

The 1-billion-user distribution channel

The most underrated number in crypto right now is the one Telegram already has on the front of its app. Roughly one billion monthly active users. Profitable in 2024, with over $1 billion in annual revenue and meaningful cash on the balance sheet. No other blockchain has anything close to a built-in distribution channel of this scale.

The stated goal is to bring 1 billion users onchain. Telegram is the only platform on earth where that goal can be stated and not be a fantasy. Onboarding happens inside an app the user already trusts. Wallets are native. Mini apps run inside the chat. Payments live next to messages. The friction layer that has stopped consumer crypto for a decade simply does not exist here.

Cocoon — the AI agent layer

Cocoon — the Confidential Compute Open Network — is the part of this that does not get enough airtime yet. Built on TON, Cocoon is a decentralized GPU marketplace where anyone with a graphics card can earn TON by running AI inference inside trusted execution environments, and developers pay TON to access private, encrypted compute. Telegram is the first major customer and the primary demand engine.

Stack that on top of the rest. You now have a chain that is the payments rail, the social layer, and the compute layer for AI agents — all delivered through one app that people already open every day. Pavel’s vision, stated explicitly, is to make Telegram the place where humans and AI agents interact. The majority of people running personal agents already use Telegram chats as the rail. The pieces fit.

Why this time is different

A small piece of context that matters. Pavel and Nikolai Durov designed TON in 2018 as the Telegram Open Network, before SEC enforcement in 2020 forced Telegram to abandon it. The codebase was then picked up and continued by an open-source community organized as the TON Foundation.

That history is the reason you should take the May 5 announcement seriously. Pavel walked away from TON 1.0 specifically because of US regulatory exposure. He would not be walking back in now, publicly, with Telegram as the validator and the operational driver, unless he had thought carefully about the regulatory environment. The CLARITY Act in the US — still in process but on track — would mark TON as a digital commodity, which is the reading Pavel almost certainly has in mind. He is more aware of this risk than anyone, because it cost him the project once before. He is not making a 2x trade. He is making a multi-year commitment, and the TON blockchain is going to be folded into Telegram’s major goals.

The vision: Telegram as the human–agent layer

Nikola Plecas, head of Telegram payments, has stated the explicit plan: turn Telegram into a global crypto payment network with the TON wallet inside Telegram as the primary user interface. That is not aspirational language. The wallet ships inside the app. The infrastructure is now fast enough and cheap enough to actually carry that traffic.

The Telegram ecosystem already has the building blocks:

• Chats and groups — the best UX in messaging, with deep user trust

• Mini apps — full apps embedded inside Telegram

• Native games — already a meaningful traffic driver

• Wallet — TON-native, already shipped

And there are obvious upgrades still on the table. The first one that comes to mind is livestreaming. Imagine groups going live on Telegram, where you can directly purchase the item being sold or send NFT gifts that the creator can resell on a TON-native marketplace. That single feature replicates the largest revenue stream on TikTok, but settles every payment and every gift on TON. If they ship that, it is a serious change — A platform called Fragment, made over $400m in revenue in the last year, NFT marketplace telegram-native (by NFT it means gits, and emojis, not monkey jpegs).

The second is privacy on payments. Telegram is already the privacy chat platform. Adding privacy-preserving payment rails on TON is the natural extension, and it is something no major competitor can credibly offer.

The Telegram IPO optionality

Telegram had been planning an IPO for 2026, with reported valuation indications above $30 billion before the process was paused. Whenever it does come back online, the IPO is a real catalyst for TON, because it forces the market to price the value of the integrated ecosystem.

There is a structural question worth holding open: when Telegram lists, will TON-equivalent value end up in the equity, or will the market start treating TON as the listed proxy for Telegram’s blockchain layer? Either path has bullish implications for the token. The first re-prices Telegram with a crypto-native economy attached. The second turns TON into the public-market shorthand for Telegram’s chain.

The risks worth naming

Two real risks should be named clearly.

Centralization. Telegram becoming the largest validator and replacing the foundation is a governance centralization. That is the thing it is. Durov has framed it as Telegram acting as a counterbalance that lets other large validators join without breaking decentralization, and there is some logic to that — but a chain where one company is the dominant validator and the dominant front-end is, by any definition, not maximally decentralized. DeFi purists are right to call that out. The bull view is that for a payment network with a billion users, accepting that trade-off may simply be correct.

US regulatory exposure. This is the thing that killed TON 1.0. The CLARITY Act passing on a clean track would resolve this in TON’s favor. If it stalls, or if the SEC posture changes, this whole thesis carries headline risk. The bull’s response is the one we already touched on: Pavel knows this risk better than anyone, and he is betting on it being manageable.

Using TONX to express a leveraged long on TON

With the regime change above as the setup, the next question is the cleanest way to express it. The token itself is the obvious answer. But there is a second option that, on the current setup, looks more interesting: TONX — TON Strategy Company (Nasdaq: TONX), a publicly listed digital asset treasury company whose entire strategy is to accumulate TON and stake it.

The people running it

The power behind this DAT is Manuel “Manny” Stotz, the Executive Chairman. His track record is the kind that matters in this seat: Goldman Sachs, Blackstone, Fortress, Rothschild, THS Partners, founder of Kingsway Capital (managing over $1.5B), and President of the TON Foundation from January to August 2025 before moving directly into this DAT operation. The person who used to run the TON Foundation chose to run a TON treasury vehicle. That is signal.

On May 4 — the same day Telegram announced its takeover of TON — Kevin Wilson took over as CEO. Wilson is a senior fintech executive with over two decades in financial markets, institutional trading, and digital assets, with prior senior roles at Citi and most recently Managing Director at Integral Development Corp leading their crypto and blockchain initiatives. The timing is not a coincidence. The new CEO arriving in the same week as the largest catalyst in TON’s recent history reads as deliberate.

The structure: maximizing TON per share

TONX’s stated goal is to maximize TON held per share. It is a Strategy-style playbook applied to TON instead of Bitcoin, with one structural advantage Bitcoin treasury companies do not have: TON staking generates real on-chain yield. Telegram has cited staking returns near 20% APR, which means the treasury is actually compounding through the network’s own incentive layer rather than just sitting on the balance sheet.

Over 220 million TON are already staked through TONX, making the company a meaningful infrastructure participant in the network — not just a passive holder.

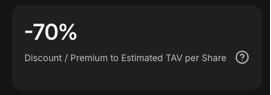

The setup: discount, holdings, and what they look like together

TONX market cap vs market value of TON holdings

Implied discount to TON-adjusted value per share

These two screens summarize the trade. TONX has a market cap around $180M against TON holdings worth roughly $545M — a discount on the order of 70% to crypto NAV. That is a price of roughly $0.30–$0.36 for every $1 of TON inside the company. There is no other vehicle in the listed crypto-treasury space that trades anywhere near this kind of discount.

Why the discount exists

To be honest, the discount is not just a market inefficiency. There are real reasons for it: the company is still working through legacy operating losses from its previous form (Verb Technology), there has been heavy dilution from the 2025 PIPE that funded the treasury, and the prior management team did not have a strong record on transparency around treasury management. Some of that discount is the market pricing those structural concerns — fairly.

But the equation has changed. Stotz is in the chairman seat. Wilson is now CEO. The TON network itself has just been transformed in a way that materially raises the value of every TON in the treasury. The same discount that may have been appropriate three months ago is much harder to justify against the current setup.

The May 12 catalyst

TONX reports Q1 2026 earnings on May 12 — next week. This is the first earnings call under the new CEO, and the first one after the entire TON regime shift. The Q1 numbers themselves will reflect a quarter that ended March 31, before any of the recent catalysts — but every single forward-looking statement on that call will sit under a completely different network than the one that existed at the end of Q1.

Two things are likely to be communicated:

• The discount itself, as the message to investors. They will market the gap between price and TON NAV.

• Capital allocation choices. Above NAV they can issue stock to buy more TON. Below NAV — where they sit today — the most accretive move is to use TON to buy back their own shares. Either path increases TON-per-share, which is the whole point of the vehicle.

On top of that, staking revenue is now a real recurring number on the income statement. At ~20% APR on a treasury this size, the run-rate yield is meaningful. The Q1 print will already show a cleaner staking-revenue line, but the bigger surprise is more likely to land in Q2, when the full effect of the network upgrade and Telegram’s takeover flows through.

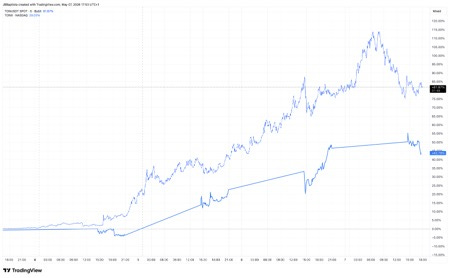

The dislocation chart

TON spot vs TONX since May 4. TON +82%, TONX +44%. The beta has not arrived.

This is the picture that makes the trade. Since the May 4 announcement, TON spot has run roughly 82%. TONX has done about 44%. A leveraged-long vehicle on TON, holding $545M of the asset, has captured roughly half of the underlying move. That is the gap.

Two readings of that gap. Either the market is genuinely sleeping on TONX — and the May 12 earnings call is the wake-up event that closes the discount — or the discount is appropriately pricing structural problems that the new management team has not yet proven they can solve. The honest answer is probably some of both. But with the discount this wide, you are being paid a lot to find out which one wins.

The asymmetry

Pull all the threads together and the setup is hard to ignore. TON has structurally re-rated as an asset. Telegram is now the operator, the validator, and the distribution engine. Cocoon adds an AI compute leg. Fees are gone. Finality is a second. The CLARITY Act, if it lands, removes the last regulatory overhang. And the Telegram IPO sits as a separate, larger catalyst behind all of it.

On the expression side, TONX gives you the same exposure with leverage built into the discount: roughly $0.36 of price for $1 of TON, plus a ~20% staking yield on the underlying, plus a competent management team that has now arrived in the same week as the largest catalyst this network has ever had, plus an earnings call next Tuesday that almost forces management to address the discount directly.

If the bull case on TON is right, TONX should at minimum compress the gap to NAV. If TON itself continues to re-rate, TONX gets both moves — the underlying and the discount close — at the same time. That is the asymmetry.

This is research, not investment advice. Crypto-treasury vehicles carry meaningful structural risks — dilution, governance, regulatory, and the volatility of the underlying asset. Position size accordingly.