Where is the crisis?

22 Mar 26'

[Brief in audio format]

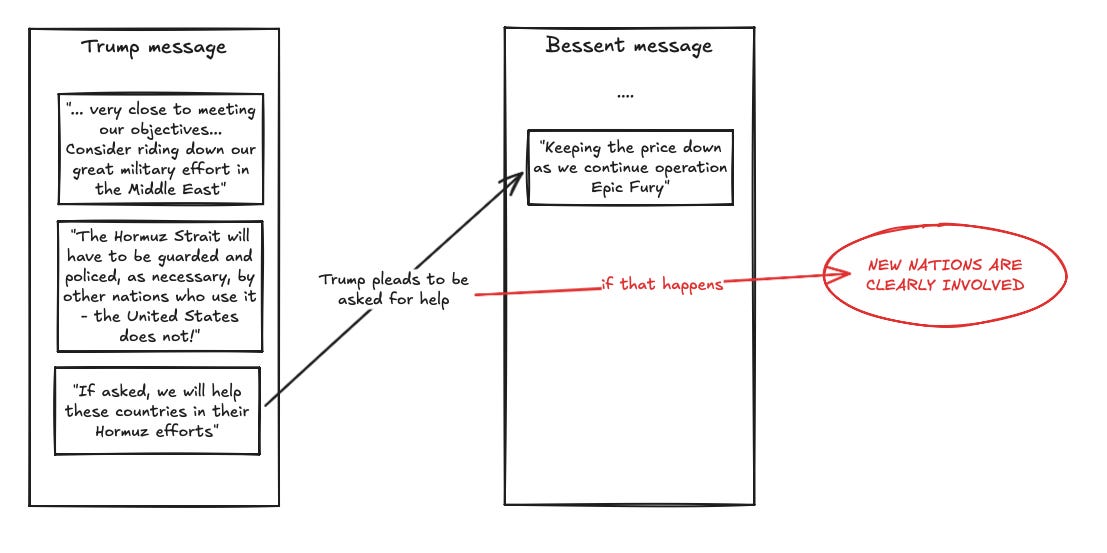

It stems from uncertainty about the current state of the Iran war. Recently, Trump announced a probable “de-escalation” after all US objectives were achieved, noting that defending the Strait of Hormuz is not America’s purpose or mandate—other nations must protect it. However, Treasury Secretary Bessent mentioned that, among other things, the administration will keep oil prices down as they continue Operation Epic Fury.

Analyzing these two types of communication, one gets the sense that the US isn’t getting the help it wants in the Strait, so they are strategically “removing” their protection to force others to ask for it. This essentially corners other nations, particularly Gulf nations and NATO, into getting involved. Gulf nations and Europe are desperate to open the Strait—it is a true emergency—but protecting it means military involvement, and involvement means escalation.

Because of this, the next moves by these nations are highly uncertain. If the US pulls out, will Iran open the Strait and allow vessels to continue floating? Will the US even allow that? Gulf nations didn’t want this war—Israel wanted it, and they got it. Now, Gulf nations are being struck and finding their own economies harmed with no direct cause.

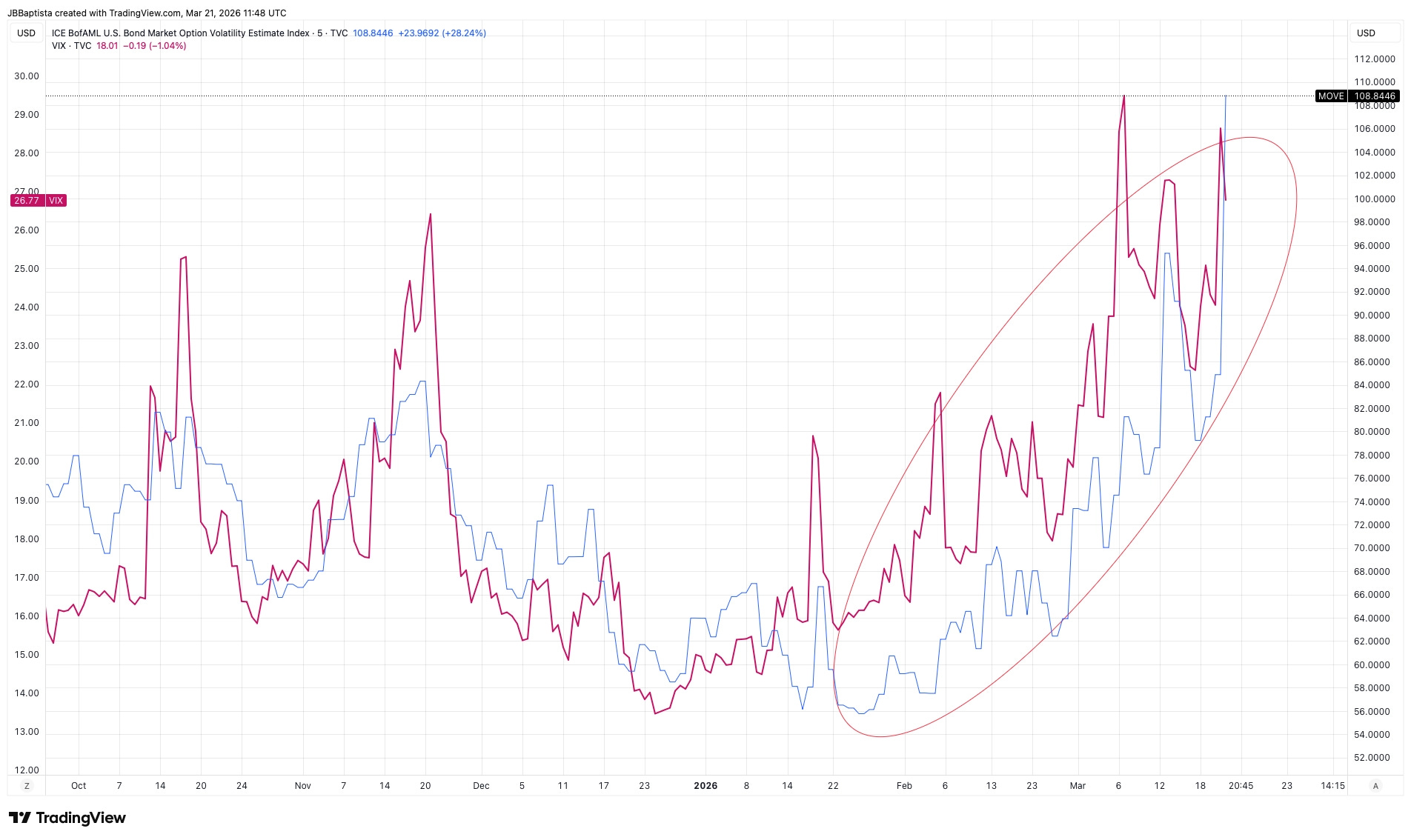

Unsurprisingly, the bond market is reflecting this chaos; the MOVE index is agreeing. Seeing this correlation after the recent Fed meeting, we have to discount some potential background noise. But the trend of rising volatility has not only been clear on the MOVE index since the war started, but it is also being mirrored in the VIX.

Despite this rising volatility, the anticipated move to risk-off assets hasn’t fully materialized; a rotation to hedge assets, particularly gold, hasn’t started. It remains unclear if this is a localized geopolitical crisis or if it represents a widespread contagion that will lead investors to dump risk-on assets. So far, strangely, gold has been down just like any other risk-on asset.

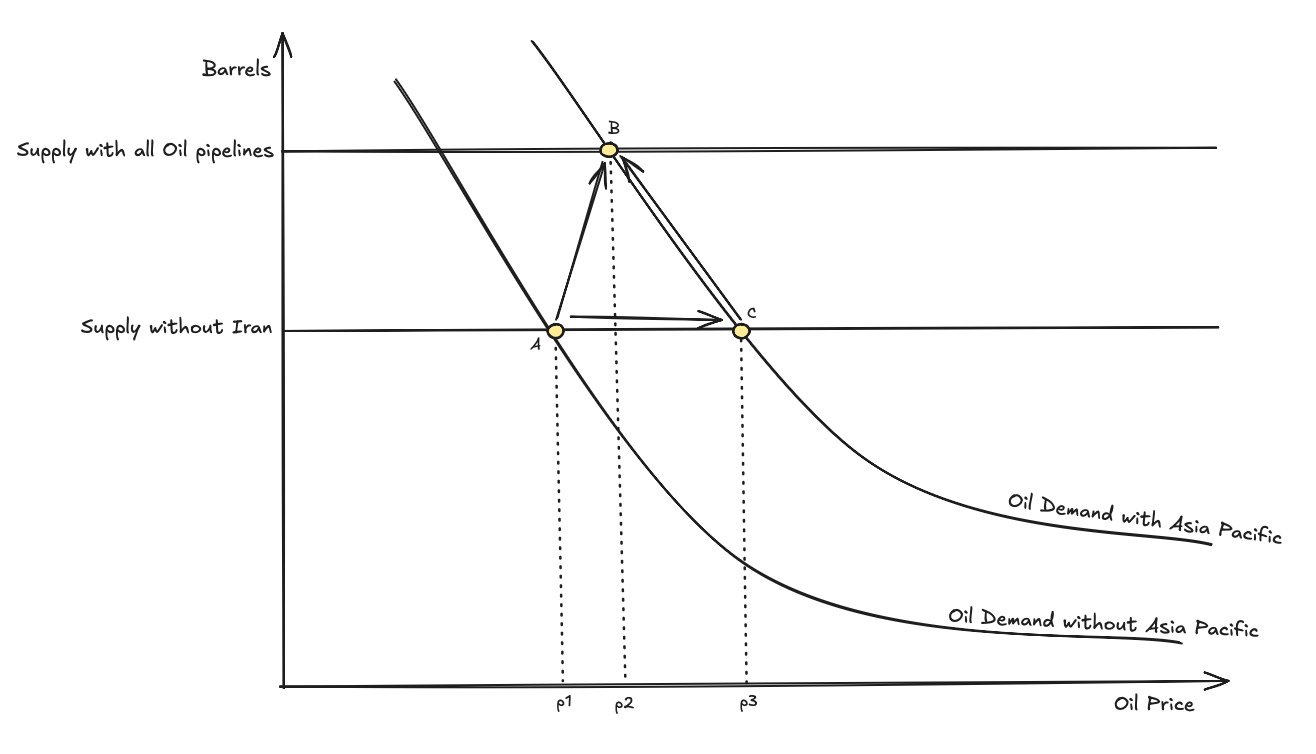

The real driver behind these market anomalies is China. In a world where the Asia-Pacific region is buying discounted, high-quality Iranian oil at a key inflection point of the changing world order, I don’t believe the US will back off. The US won’t allow Iranian deals to be done outside their system, nor will they allow all that oil supply to be absorbed by the same competitor nations. The US needs a strong Europe—Europe is not a threat. China is. This is especially true when oil is being sold at huge discounts to America’s direct competitor.

Building on this dynamic, there are two major caveats to consider regarding US strategy. First, Bessent recently mentioned in a tweet that the US aims to “bring around 440m additional barrels of oil to the global markets, undercutting Iran’s ability to leverage its disruptions in the Strait of Hormuz.” He specifically highlighted a short-term goal to bring 140m barrels of Iranian oil, currently stranded at sea, onto the open financial system. This clearly shows the strategic direction of their oil goals.

Conventional wisdom suggests that expensive oil is good for America, given they are a net exporter. However, there are three reasons why this is currently false: 1. The US aims to aggressively expand AI development, bring massive manufacturing onshore, and create a new tech boom. That requires a massive supply of cheap energy, which may not be supported by their own supply alone. 2. China—their major competitor—is buying oil at unfair, discounted prices and growing like crazy. 3. Russia is a massive net-exporter of oil, and higher prices mean higher revenue for them.

Consequently, the US is ready to take a hit on its own oil revenue if it means vampirizing the revenue of its adversaries. At this stage, controlling the growth of competitors is much more important for the US empire than growing its own direct profits. By bringing stranded Iranian oil supply onto the open market, they can directly dump the price of oil substantially and track China’s growth based on their consumption.

The second caveat is that the Iran war isn’t over, and Trump is already raising alarms about a probable “friendly takeover” of Cuba.

The geopolitical world is starving for information, making tracking the MOVE index vital to understanding shifting risk. However, it is not entirely clear how directly correlated the price of Bitcoin (BTC) is to the MOVE index right now. What we can note is that drastic spikes in the MOVE—specifically those sending it above 120 and toward 150—create high pressure on risk-on assets and tend to dump BTC. Usually, a V-shape recovery happens as soon as BTC transitions from trading as a risk-on asset to a risk-off hedge.

Historically, MOVE has traded in an 80–150 range for long periods. During these times, BTC has moved both directionally down and up, meaning you can’t simply draw a straight line saying ‘MOVE up equals BTC down.’ But we can confidently say that a rapid spike to 150 could create a short-term, aggressive downward move for BTC that recovers rapidly. Positioning ourselves for this potential ‘black swan’ dip is key to unlocking massive opportunities.

Interestingly, despite these potential short-term drops, BTC has been trading incredibly well during wartime. In scenarios where gold and equities are down, Bitcoin is up. In a world where conflicts with China signal a changing global order—and a changing asset order—Bitcoin is proving to be a genuinely effective hedge.

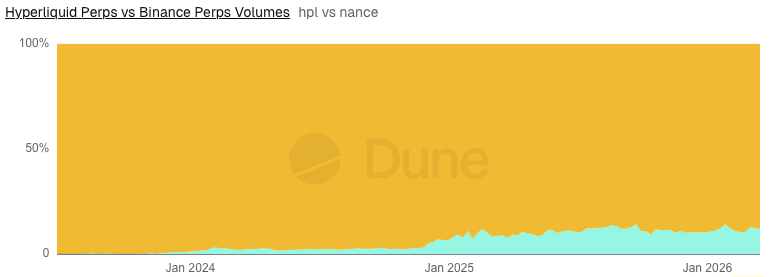

Bitcoin isn’t the only crypto asset proving its fundamental value right now; Hyperliquid (HYPE) is doing the same. Hyperliquid has arguably become the most promising project in the space. To borrow from Philip A. Fisher’s stock categorization, there are companies that are ‘fortunate and able’ and those that are ‘fortunate because they are able.’ The Hyperliquid team has proven they fall into the latter category. They consistently demonstrate the ability to ship new products, hire sophisticated talent, and onboard the high-quality users required for any product they launch. Their earnings directly reflect this. Starting as a crypto-only perp trading machine, they are expanding into all sorts of asset classes, slowly but surely eating into the market share of both centralized crypto competitors and traditional exchanges.

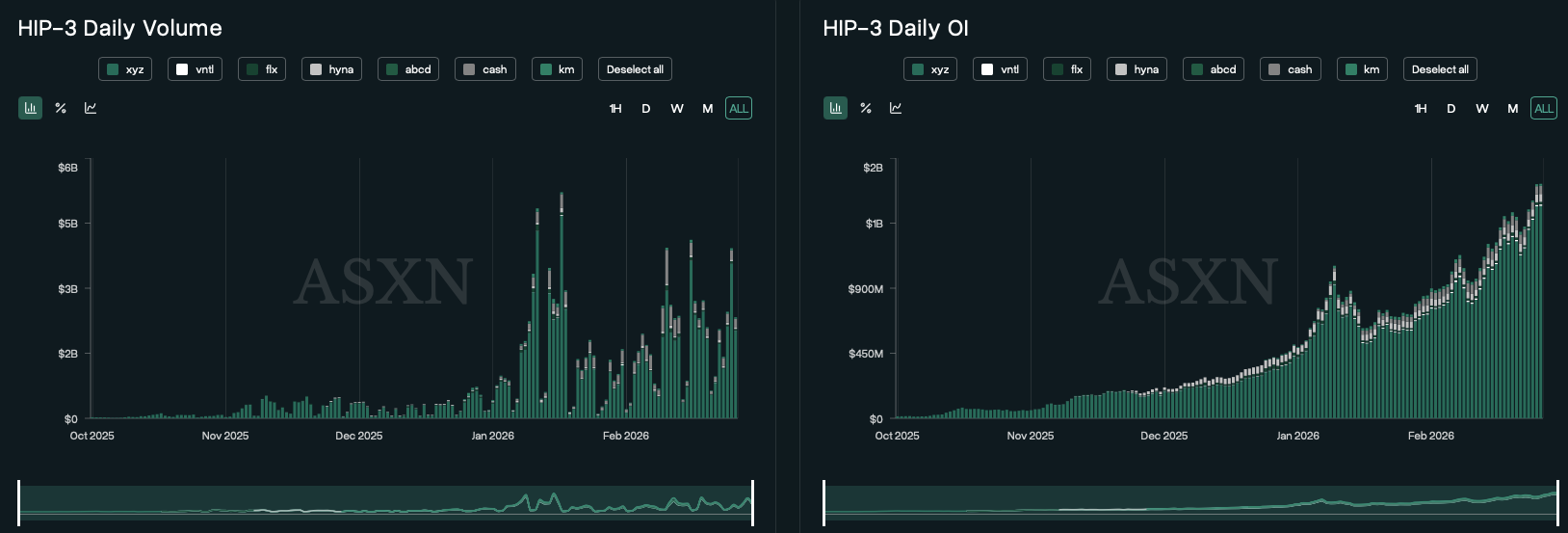

A prime example of this growth is their HIP-3 markets, which currently present one of the most bullish charts ever invented. I remember analyzing how HIP-3 was created back on October 13th, wondering how it could successfully move tokenized versions of traditional assets on-chain, and asking: who would use this venue over others? On that day, hype on the news pushed the token from $38 to $42, before quickly dumping to almost $20.

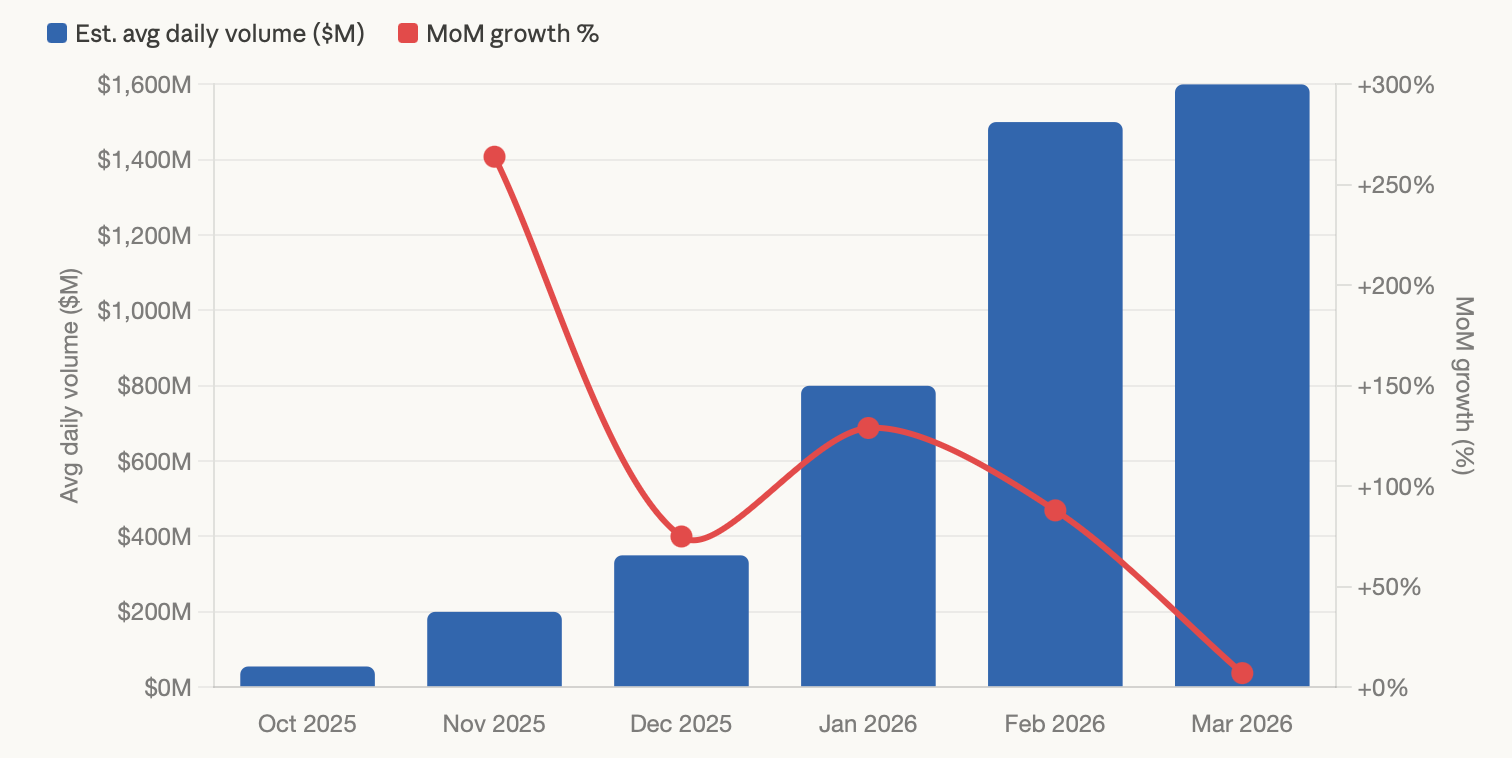

Fast forward to today, and HYPE is trading around that same October 13th price level. However, the fundamentals have exploded: just on the HIP-3 markets alone, it now boasts $1.6B in total open interest and $1.5B to $4B in daily weekday volume, all achieved in roughly five months.

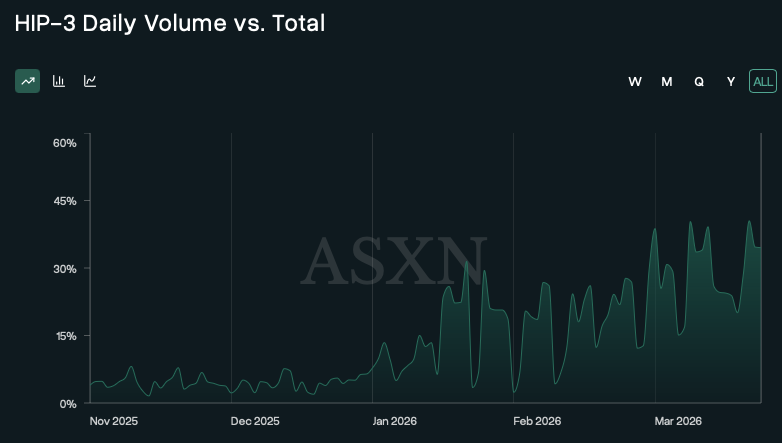

These HIP-3 markets are rapidly capturing crypto market share, now representing roughly 35% of the total and growing consistently.

Financially, the protocol is generating between $1.5M and $2M a day in revenue, using the majority of that to buy back the token. This equates to $500M to $750M in annual buybacks. For a project with a $9B market cap, it’s trading at a highly attractive 12 to 16 times sales with a buyback yield of 5% to 8%.

Ultimately, HYPE is not just a value accrual mechanism for the exchange; it is functionally designed to provision new markets for the protocol. Using HYPE as a utility token allows participants to create, vote on, and participate in new products within the ecosystem. This unique approach substantially increases the incentive for institutions using the venue to hold the token to enforce their wants and needs. Validating this institutional interest, S&P Dow Jones, in partnership with TradeXYZ, recently launched their first S&P 500 perpetual contract exclusively on Hyperliquid. This cements the real-world use case for the platform and highlights exactly where the smart money is heading in this shifting macroeconomic landscape.

This is intended to be a thought exercise, and not financial advice. Reach out in open conversations, DM me or comment anytime.

I’m aiming to provide clarity about the world day-by-day, and I hope you get smarter and more financial intelligent every day. Each day we increase our chances of winning.

Thanks, Joao